EPAM Systems, Inc.'s management explains the business in its own materials. The slides below do the most of that work, pulled from the documents preserved in Sources. Each source link opens the complete presentation at that slide in a new tab.

EPAM's current company-overview deck: the fastest tour of what it does, its scale and segments, the AI strategy, and FY26 guidance. · Open the full document →

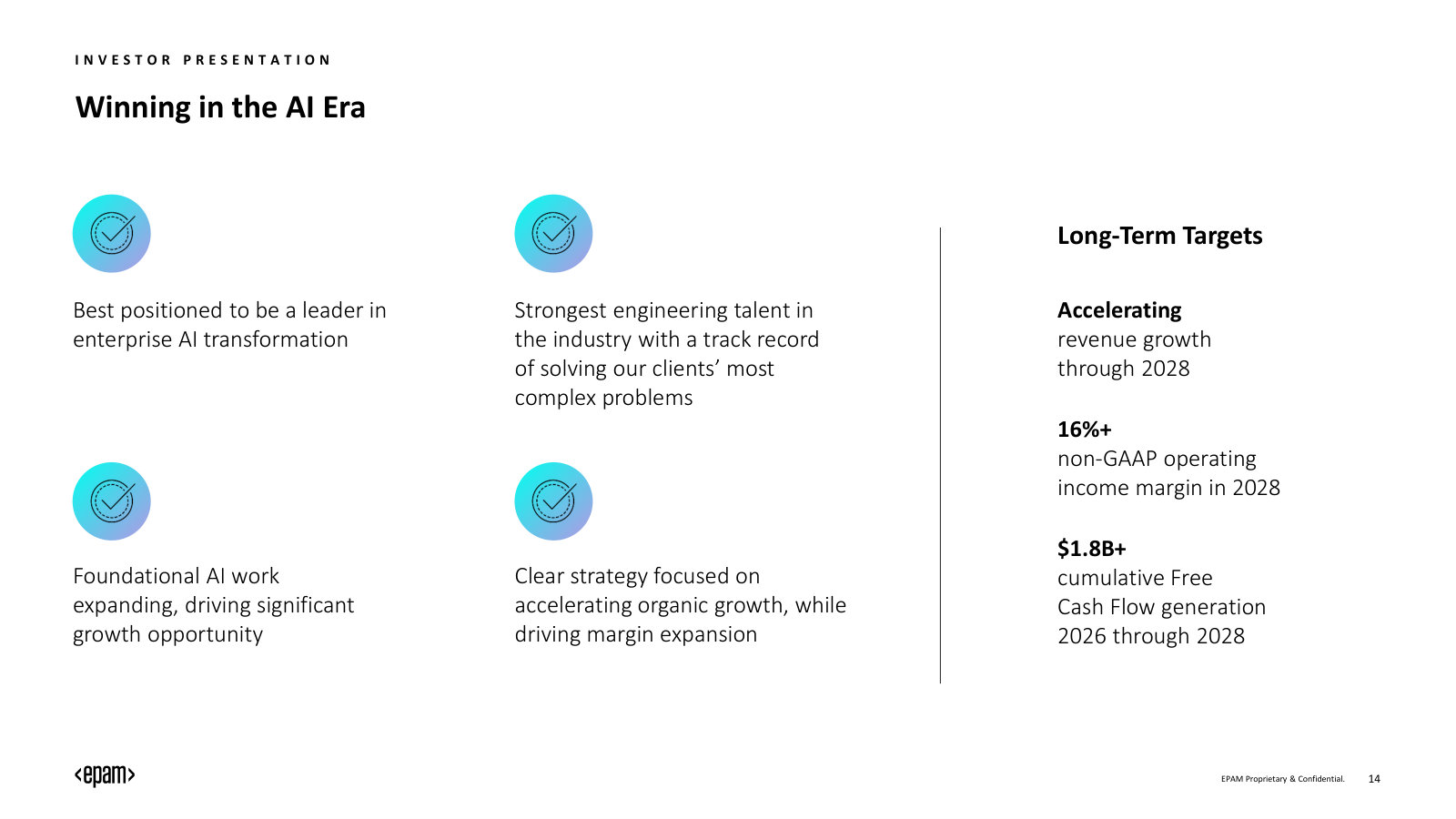

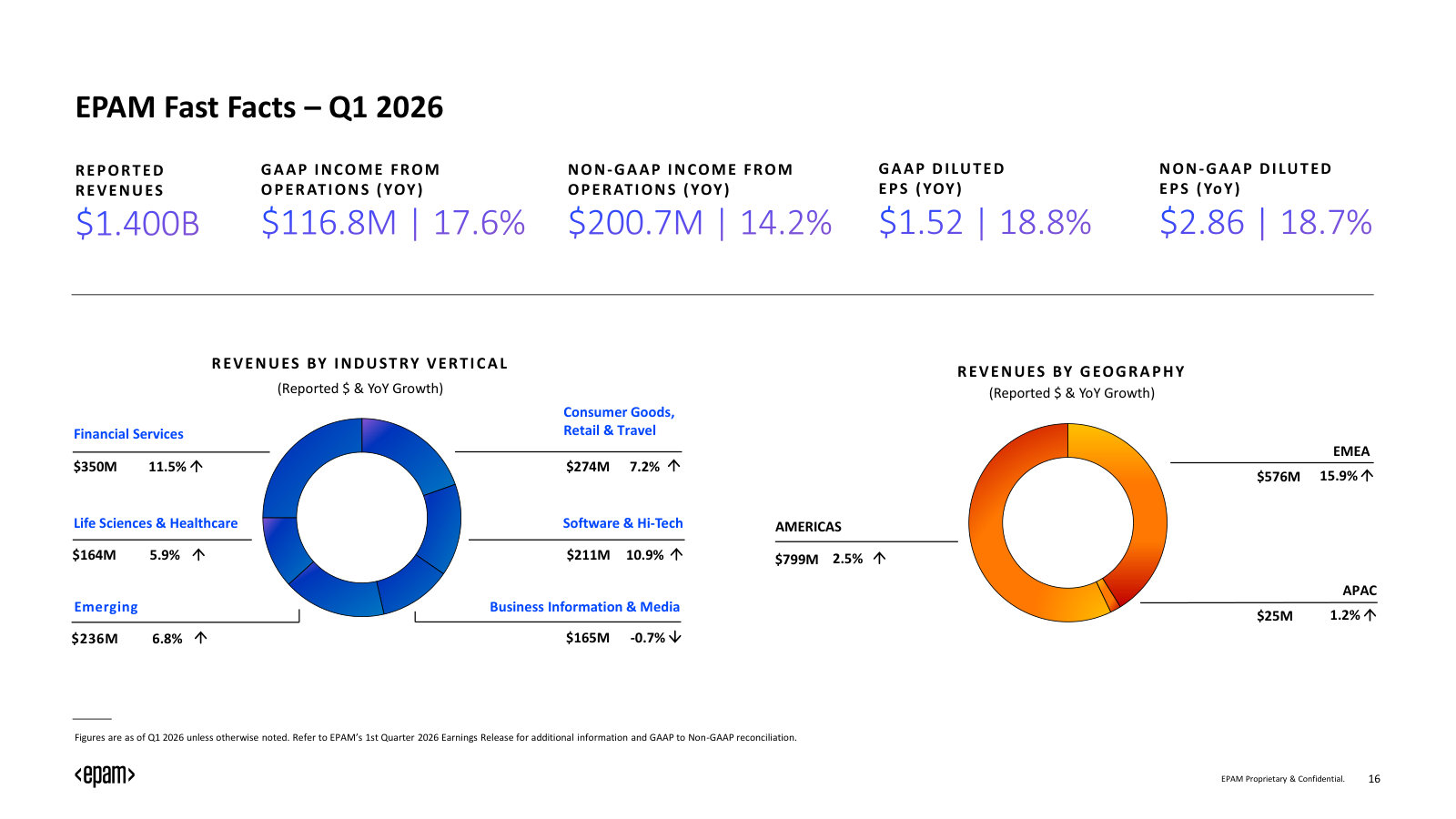

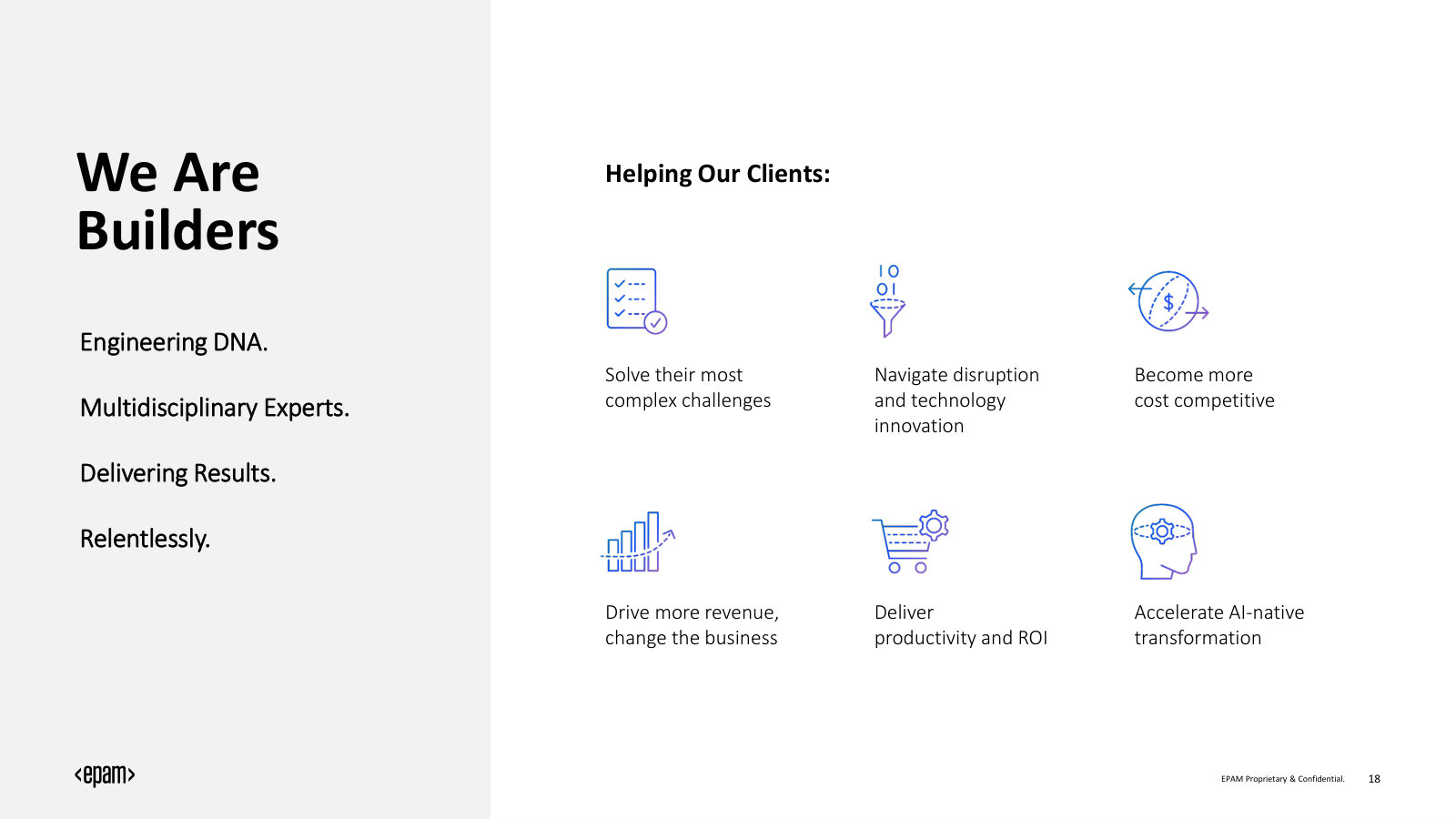

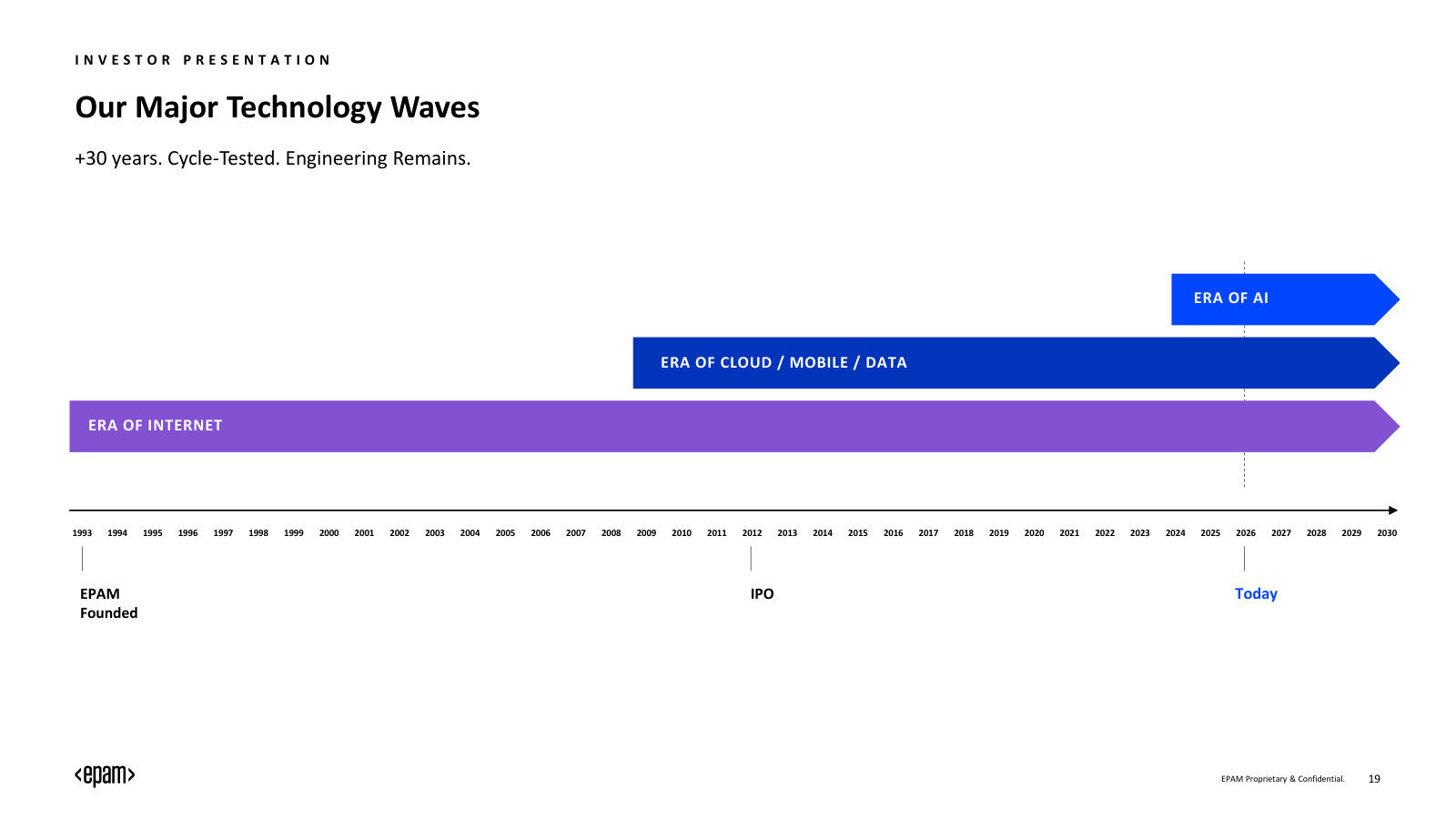

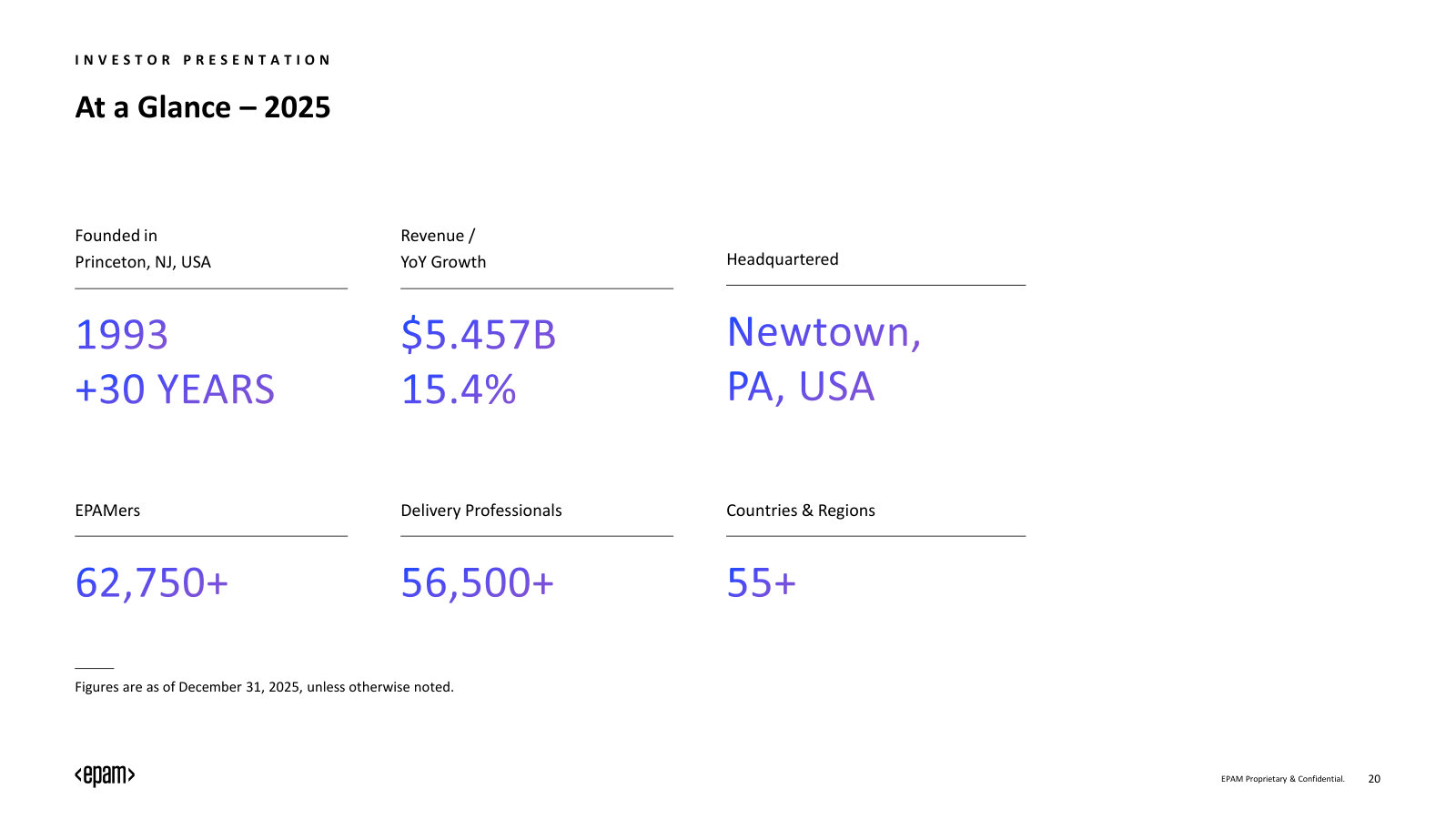

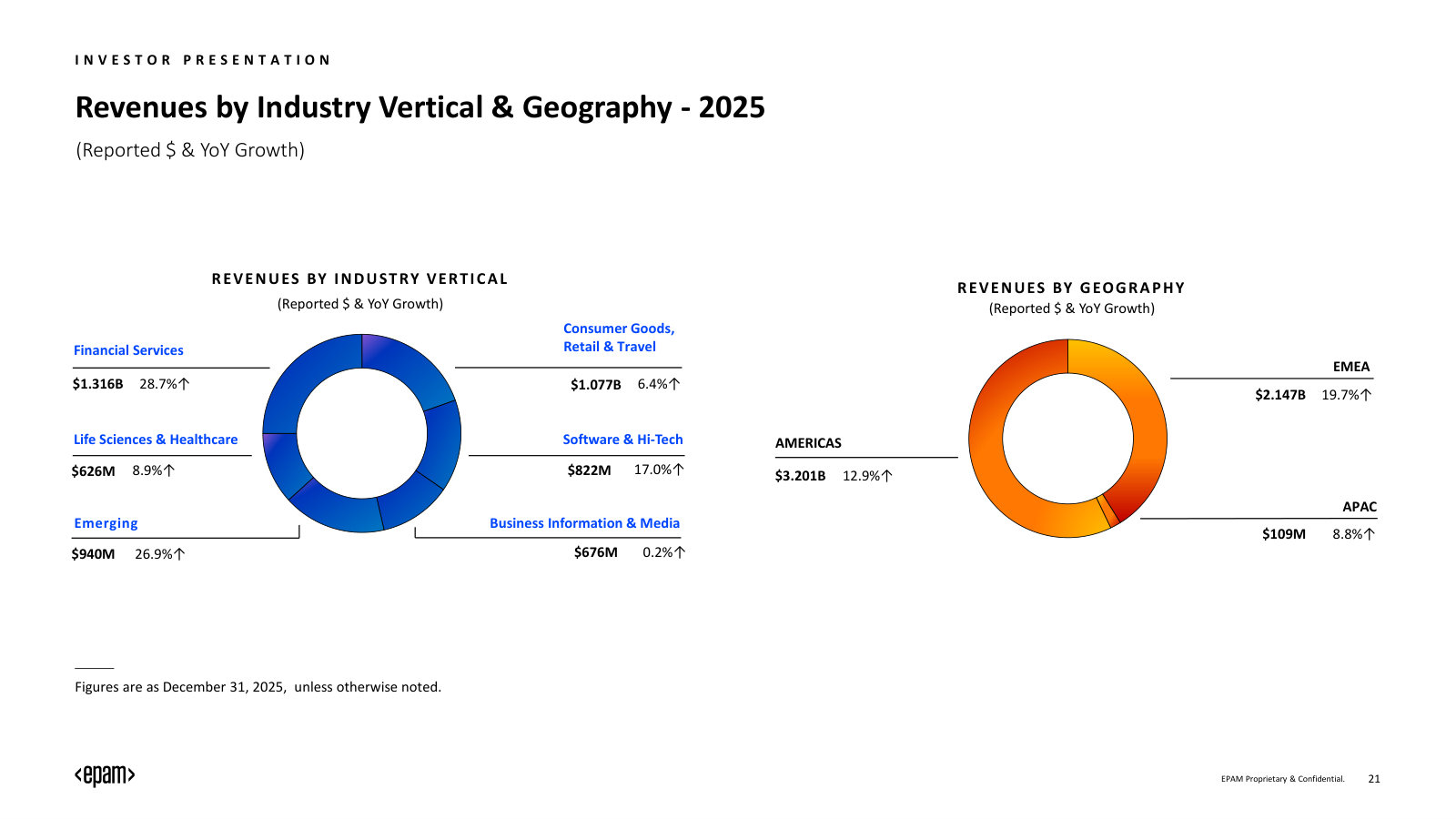

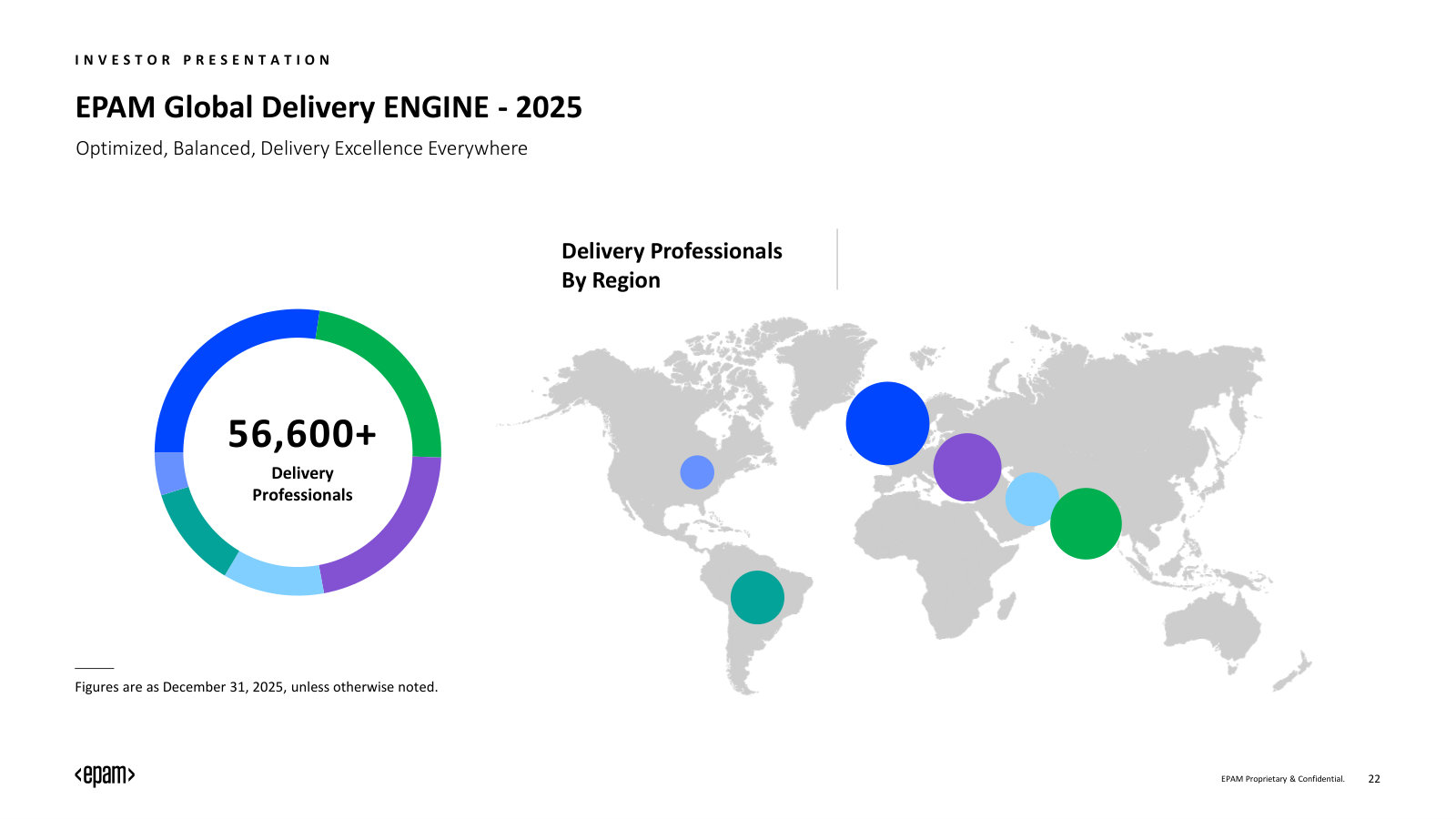

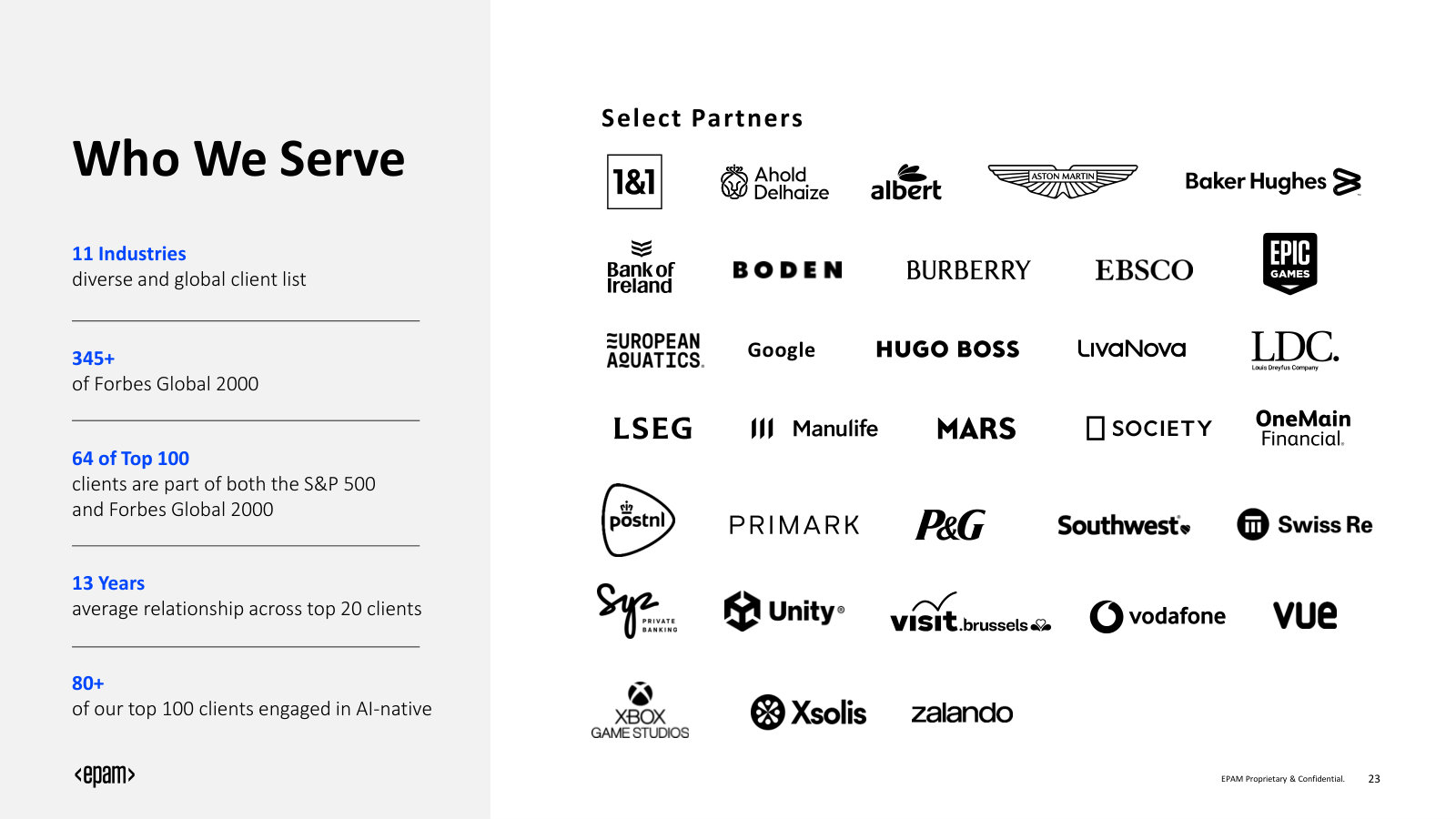

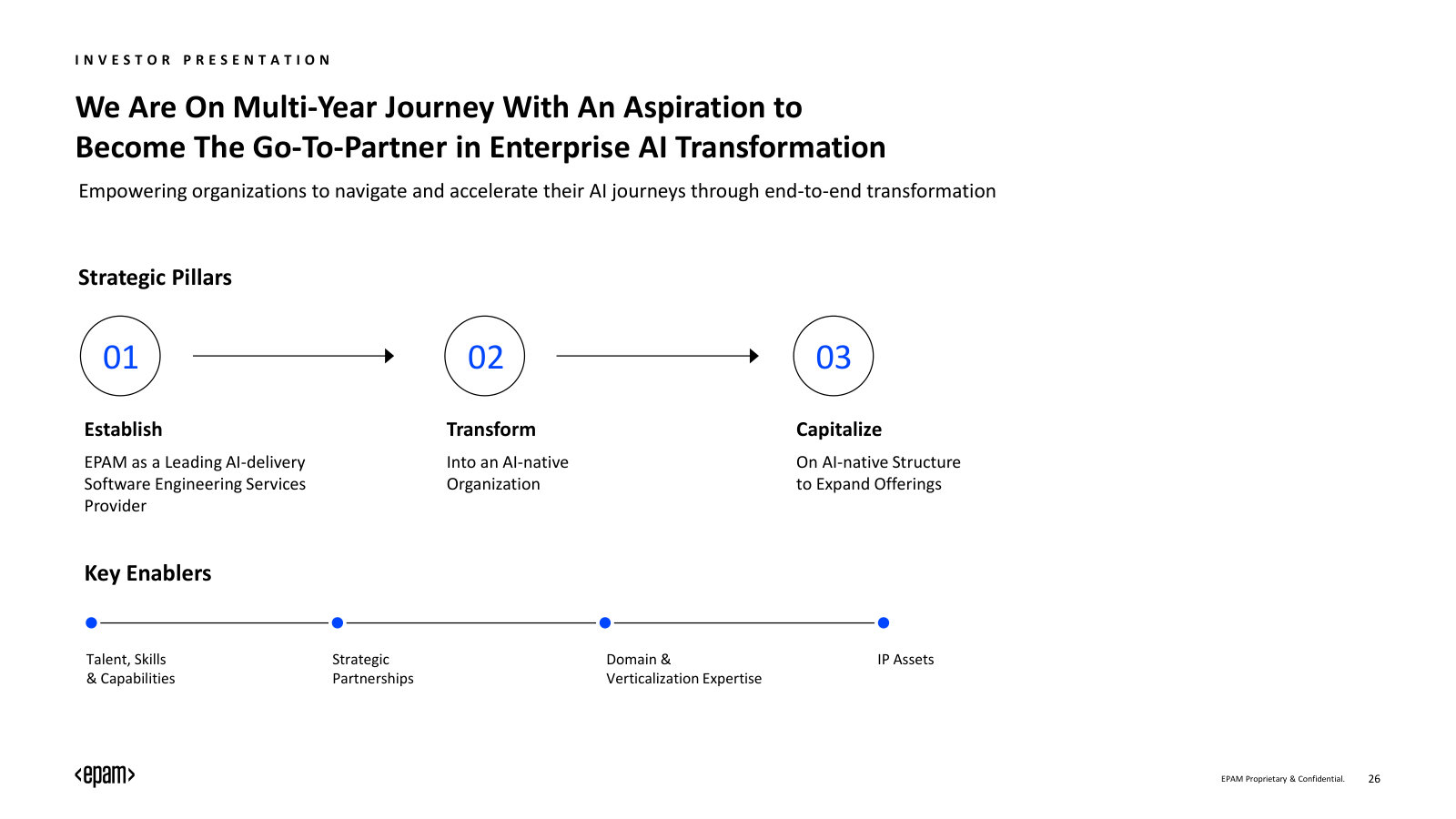

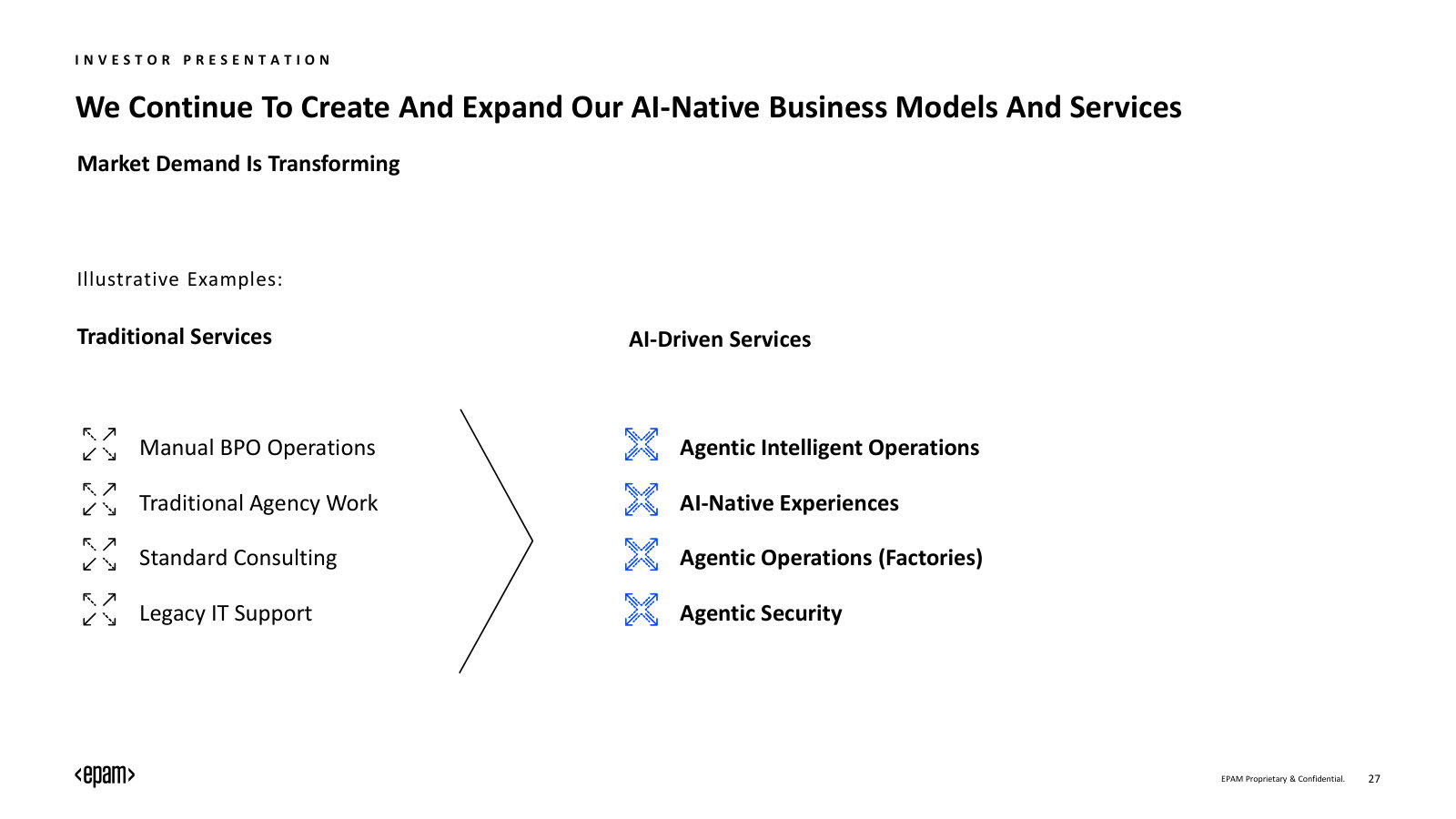

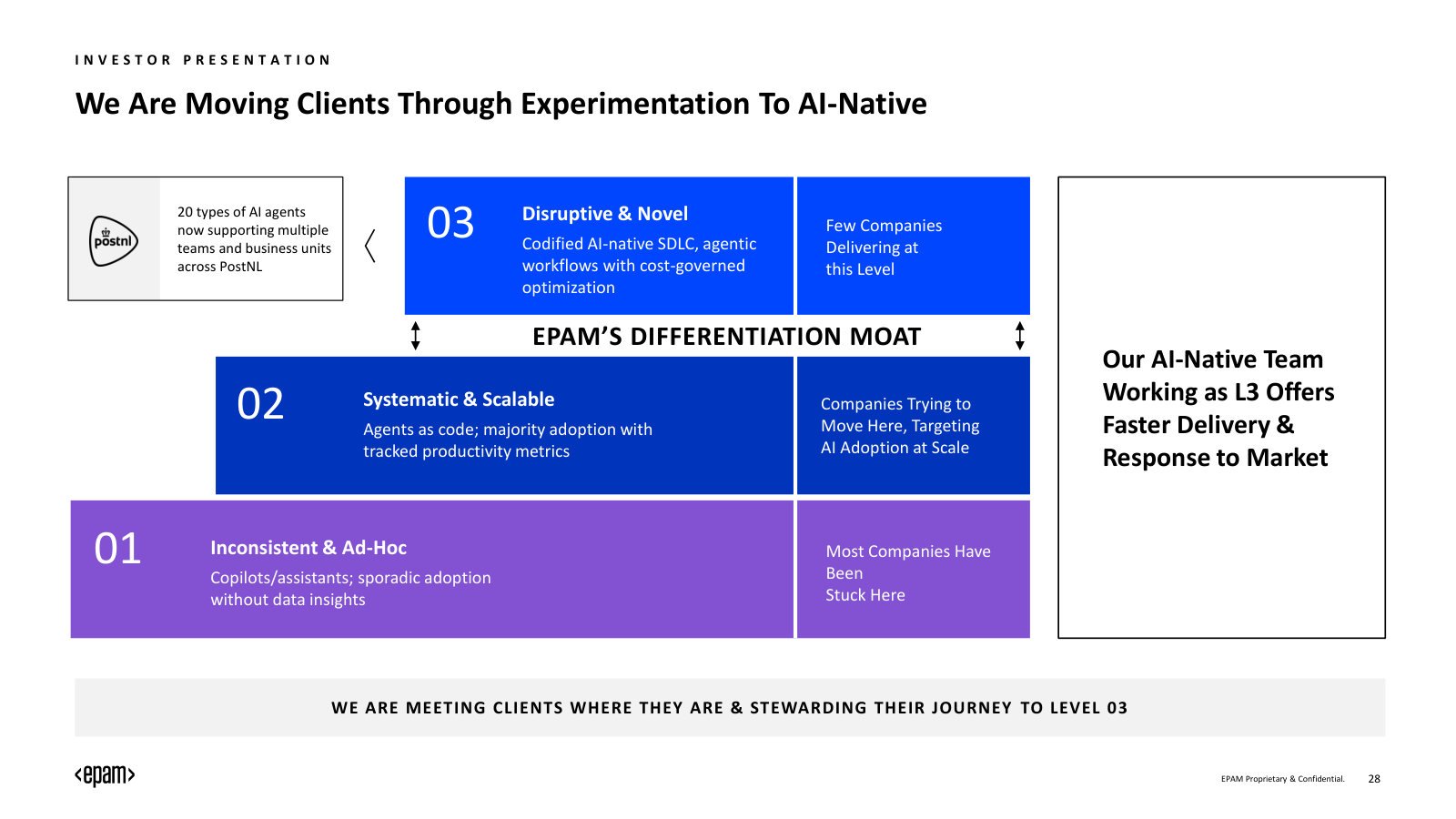

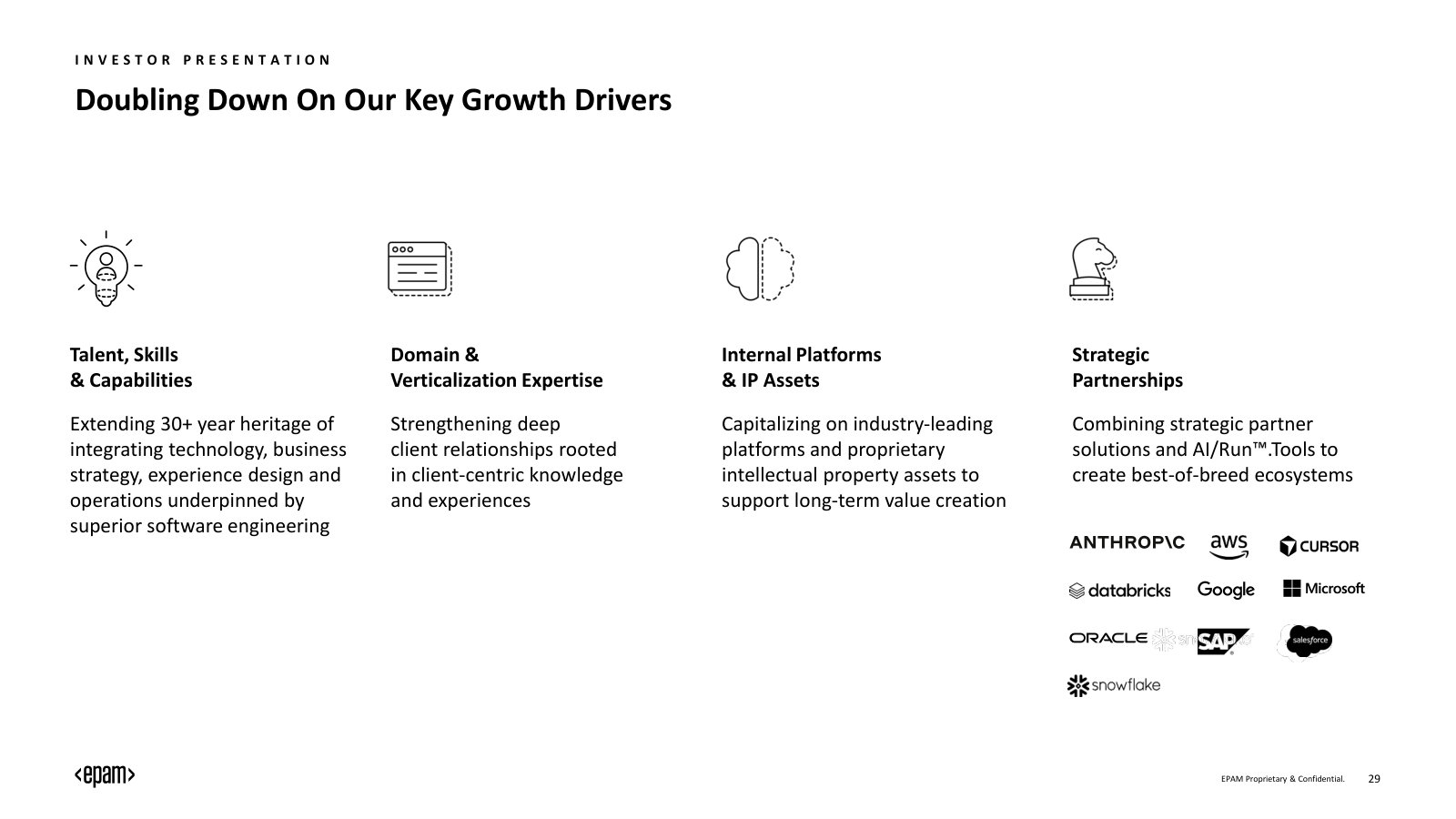

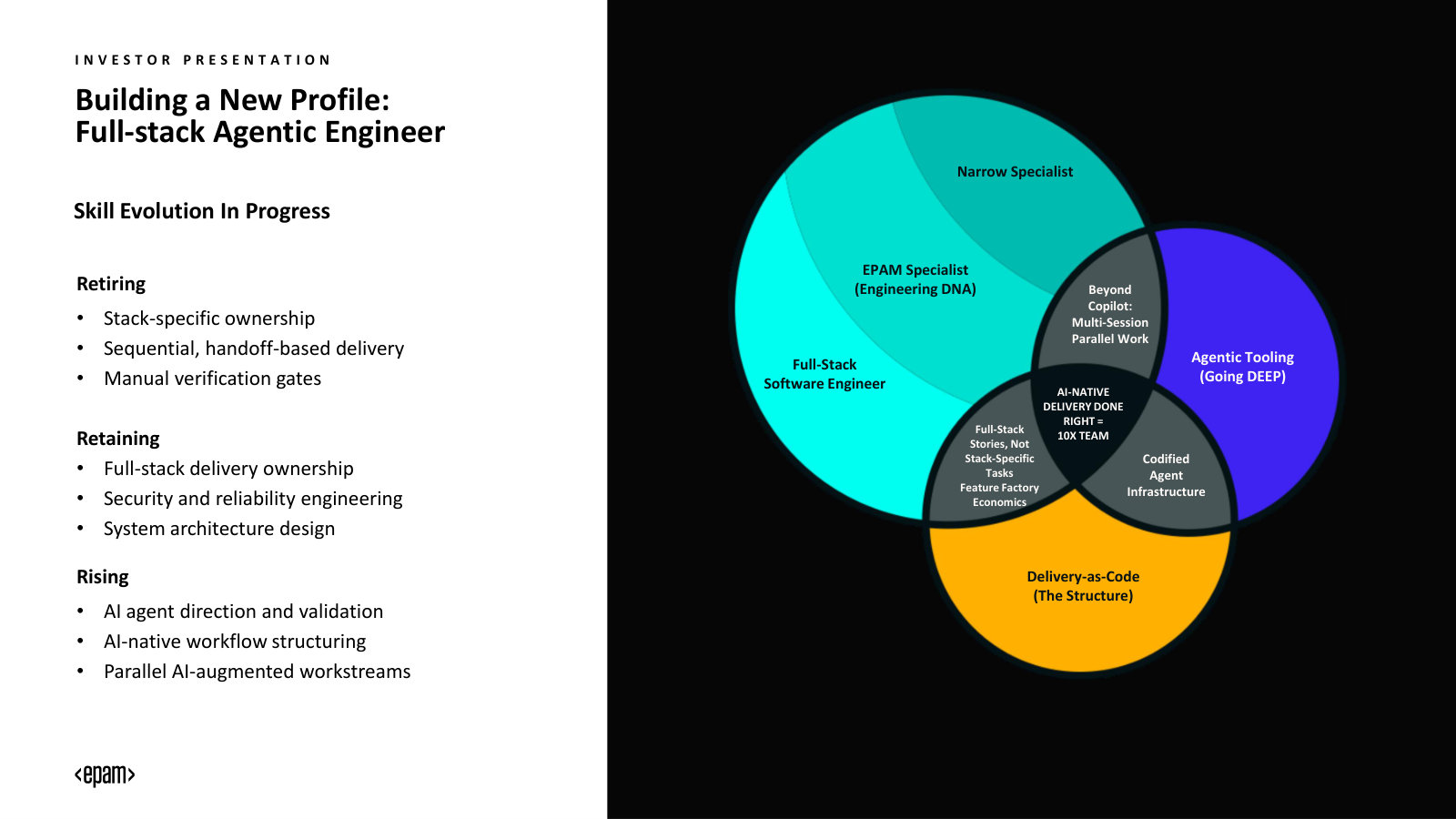

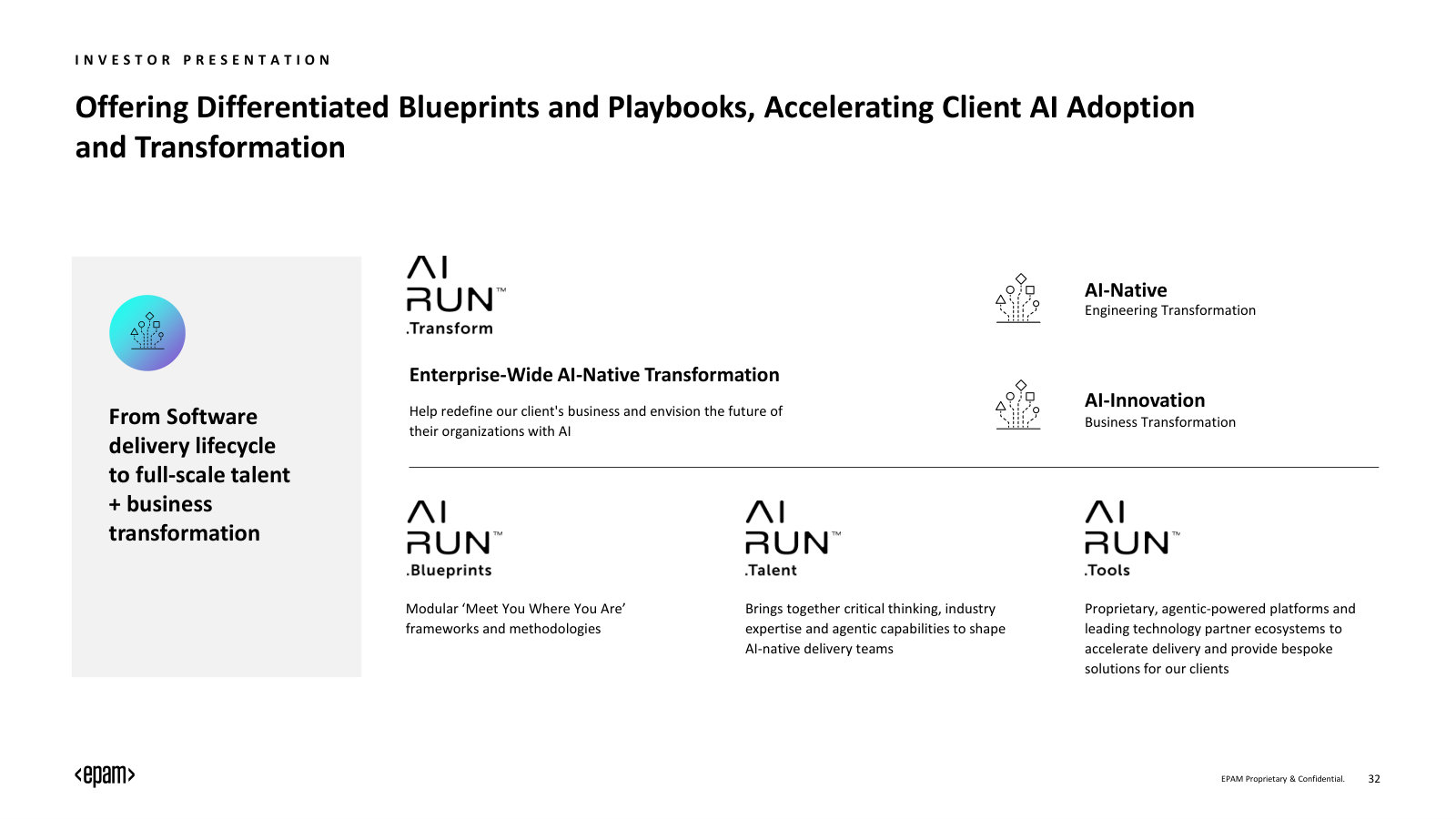

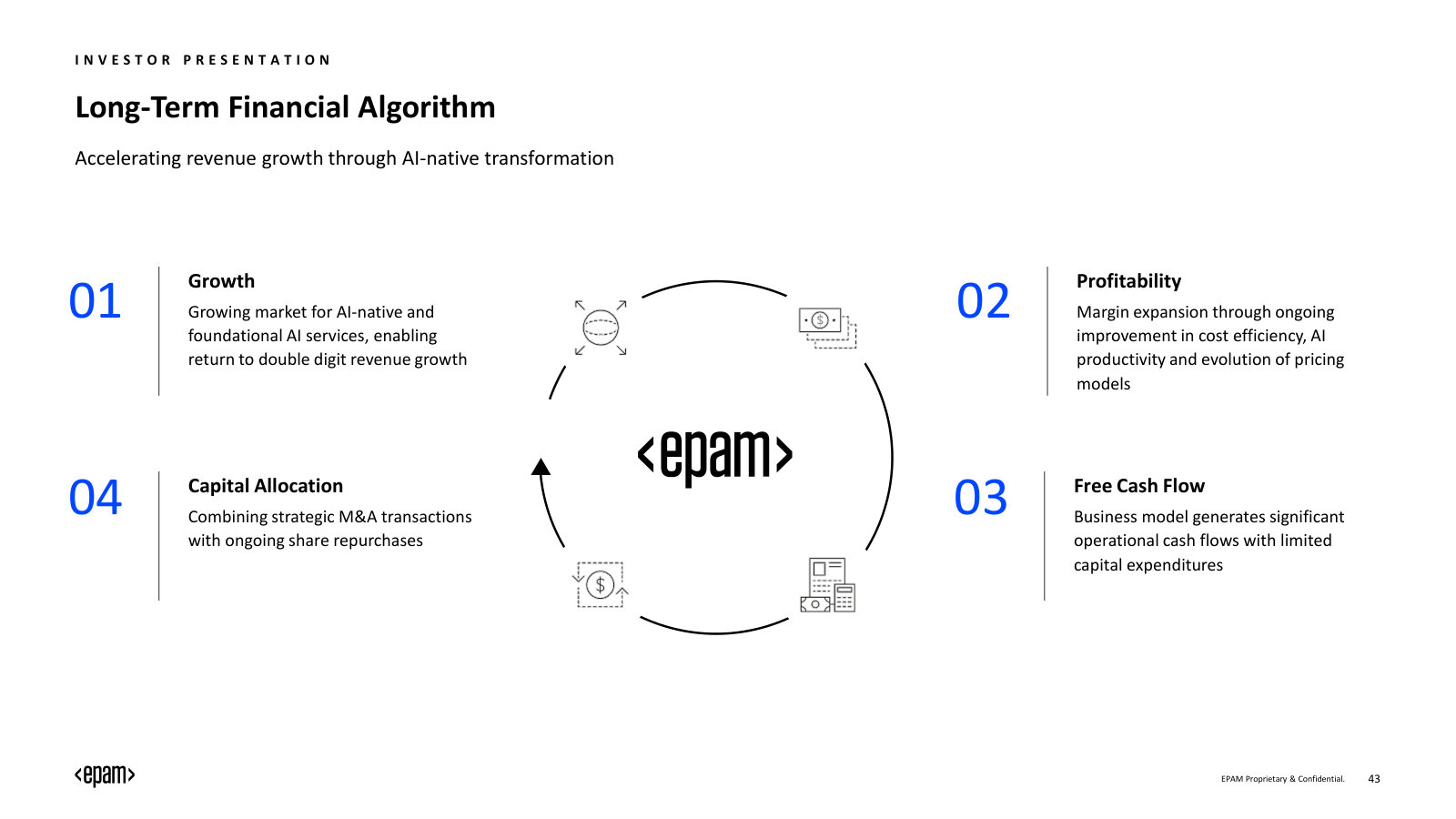

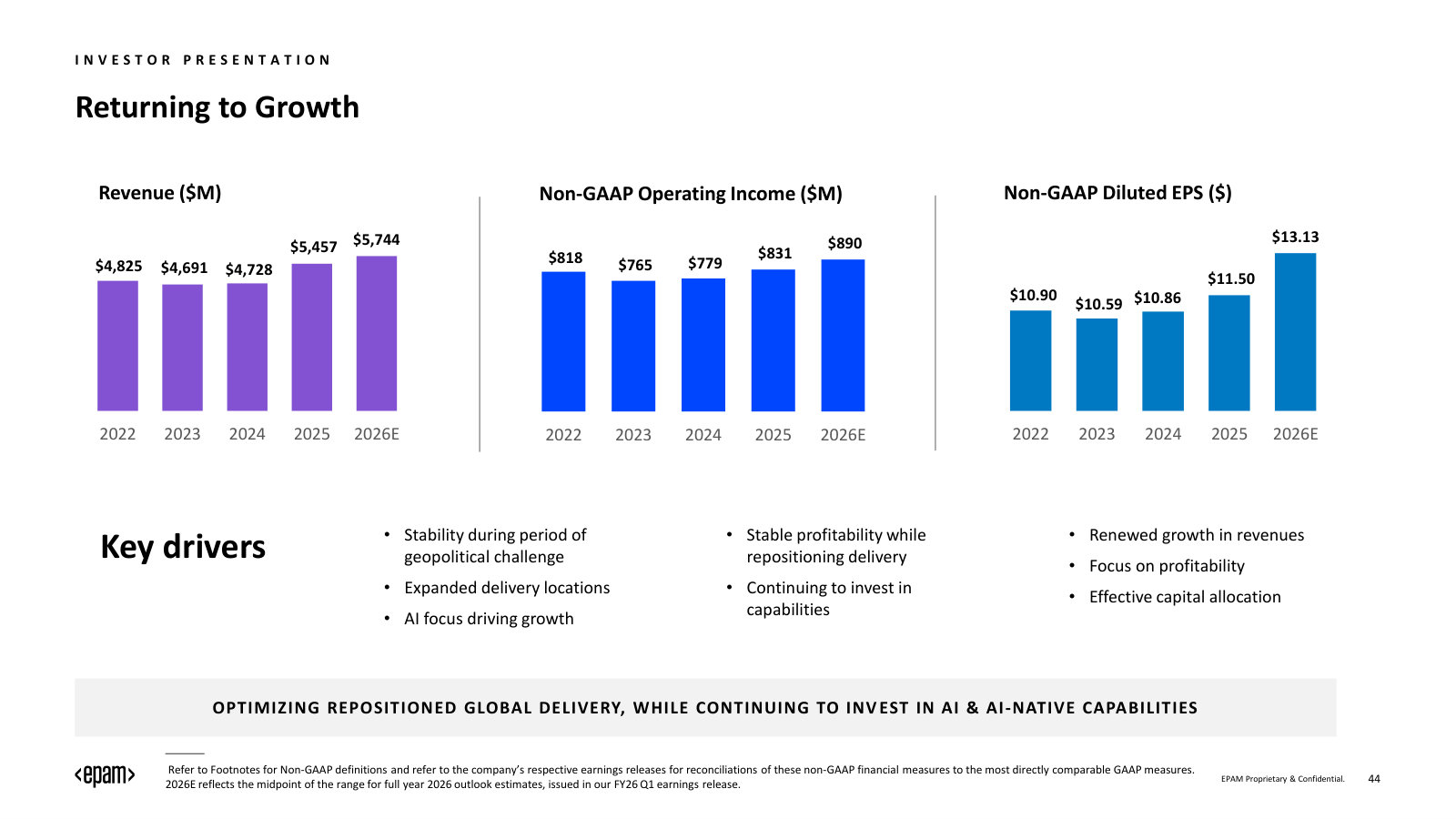

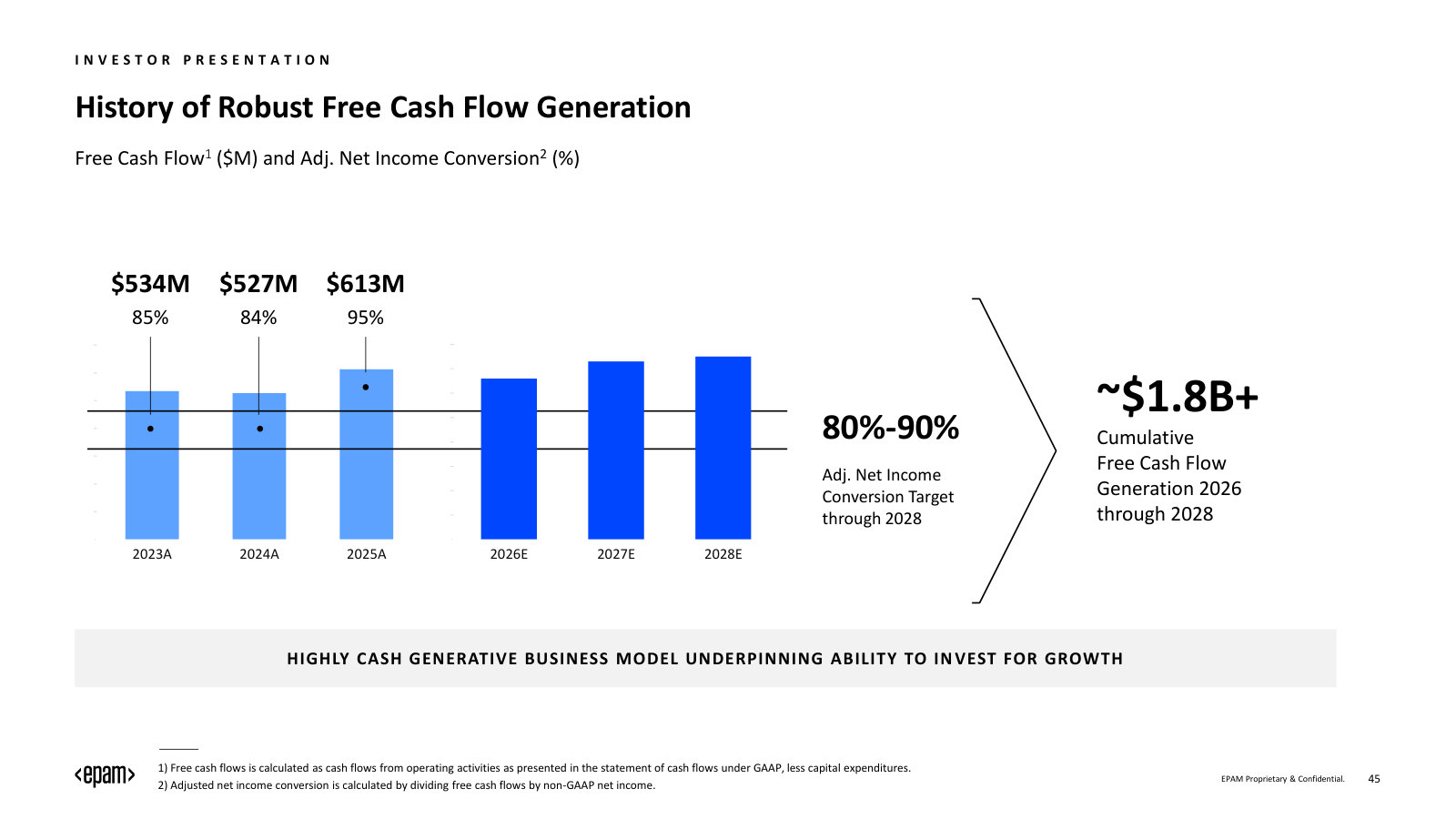

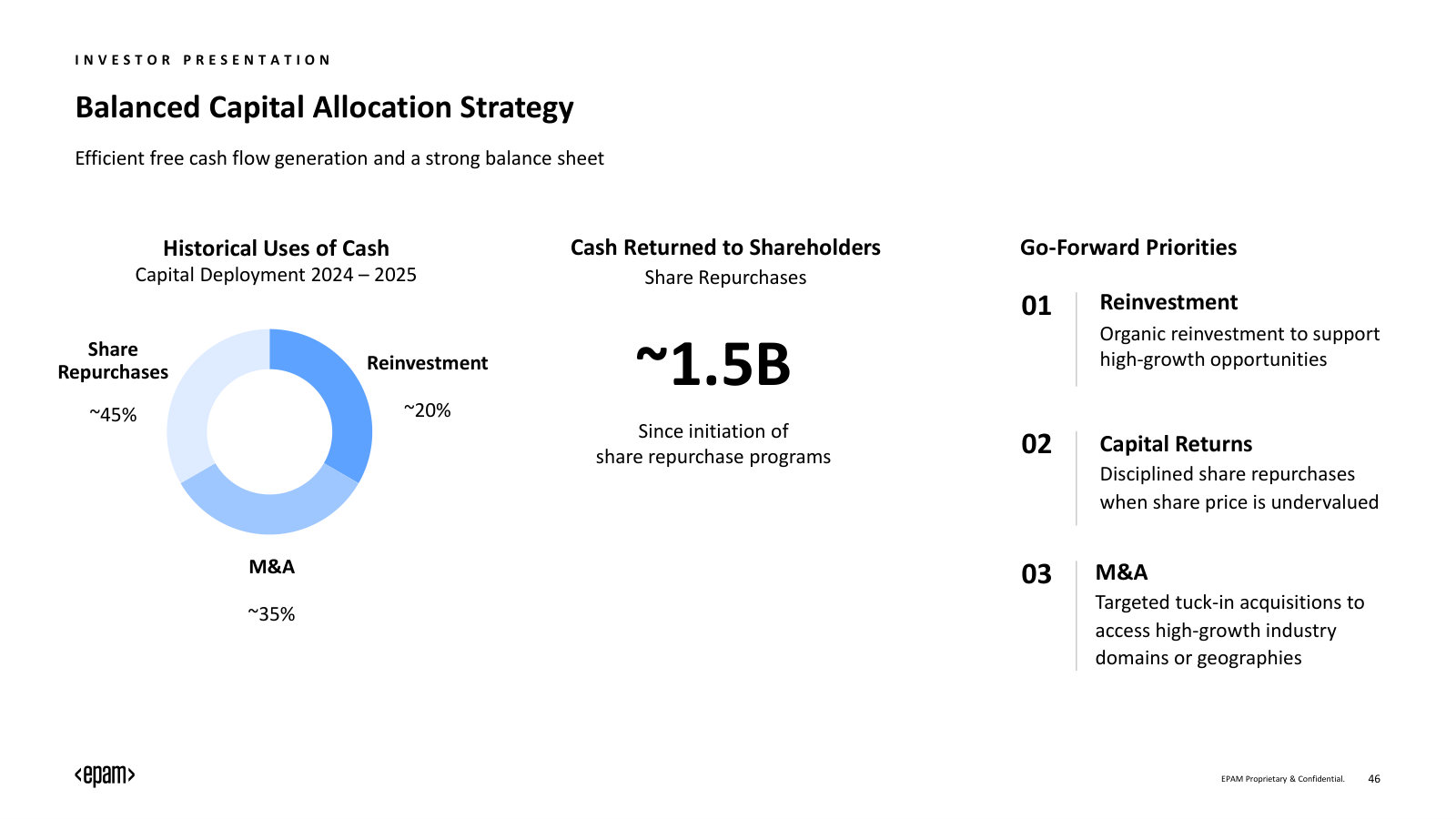

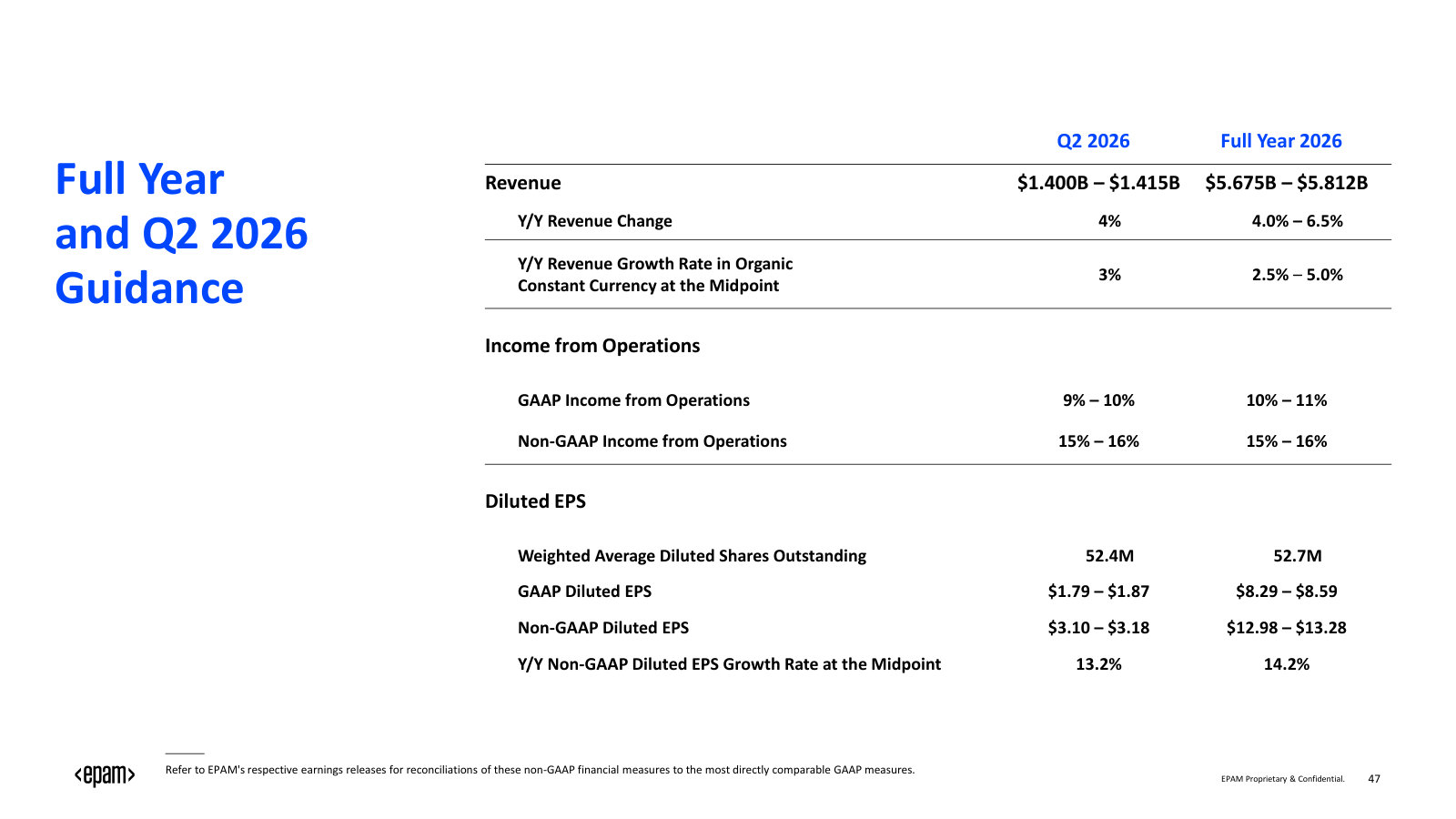

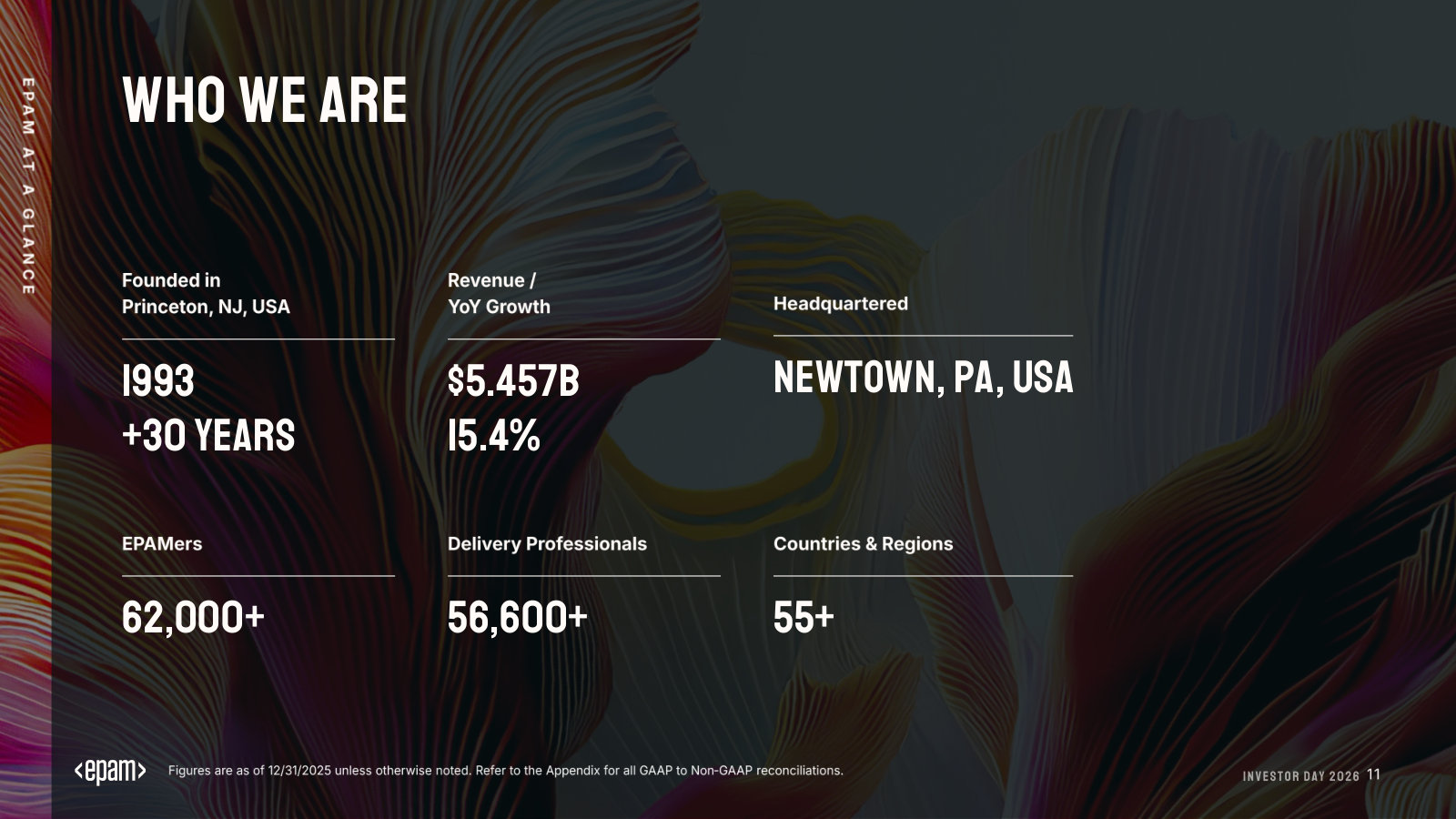

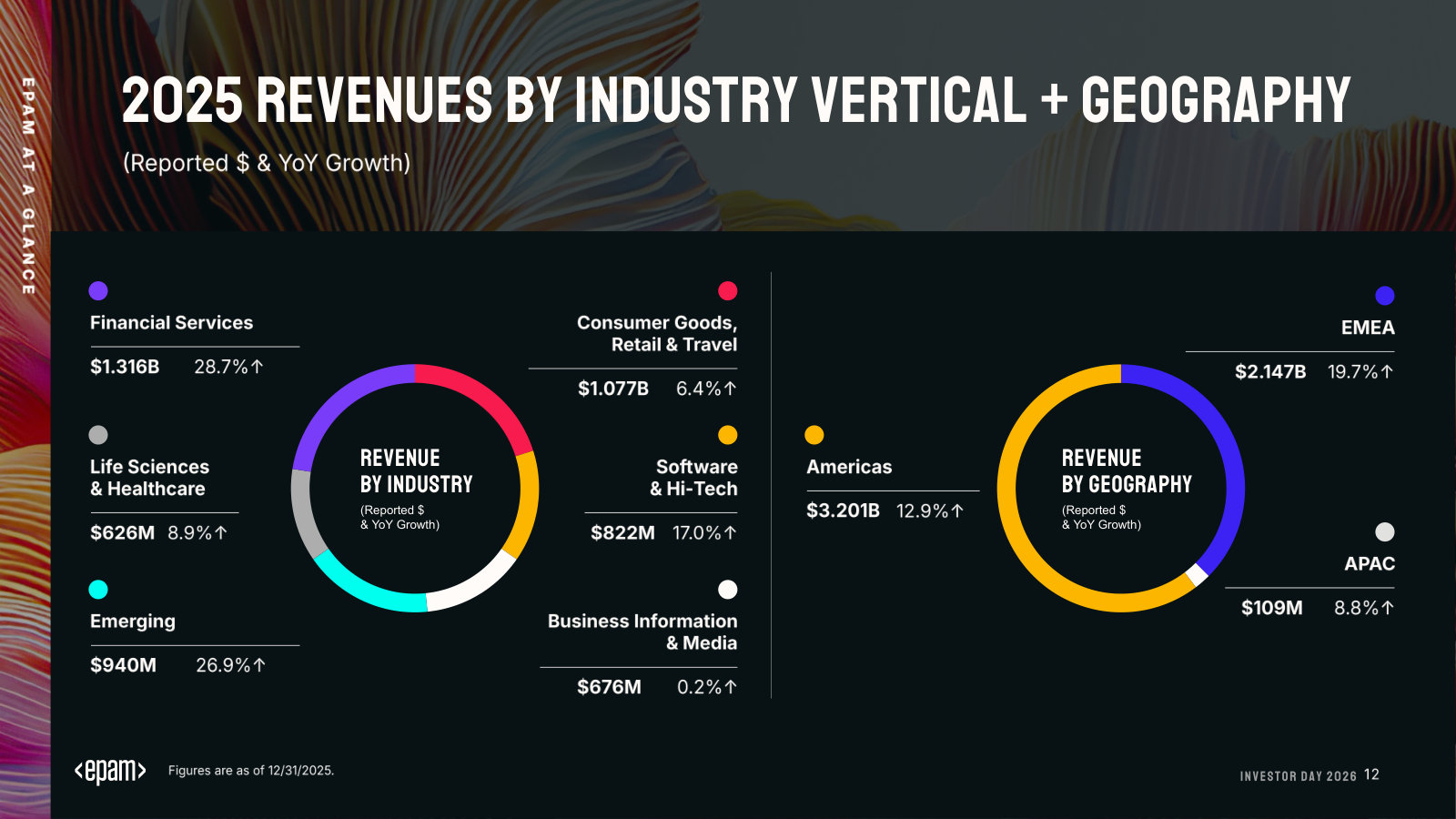

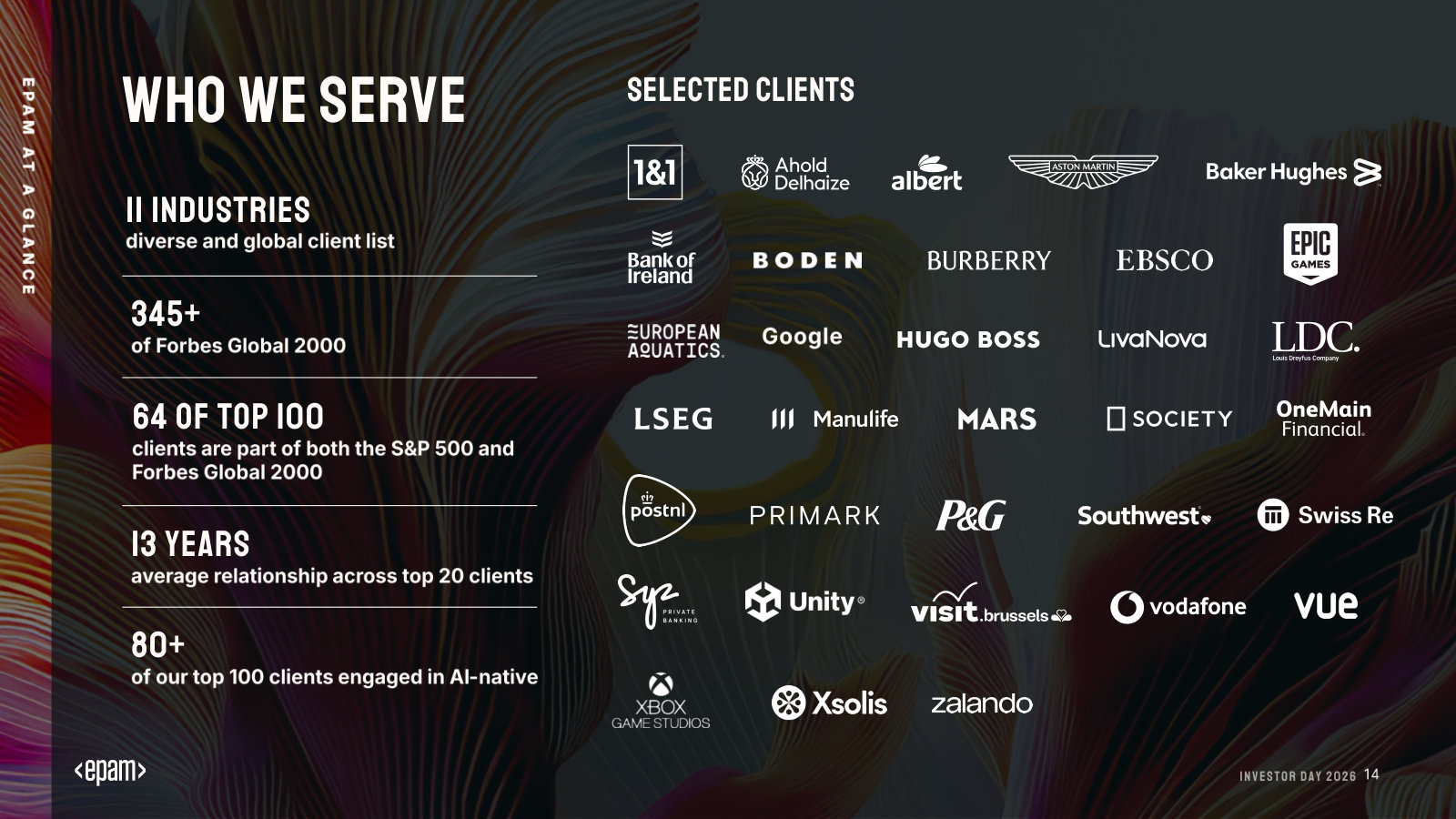

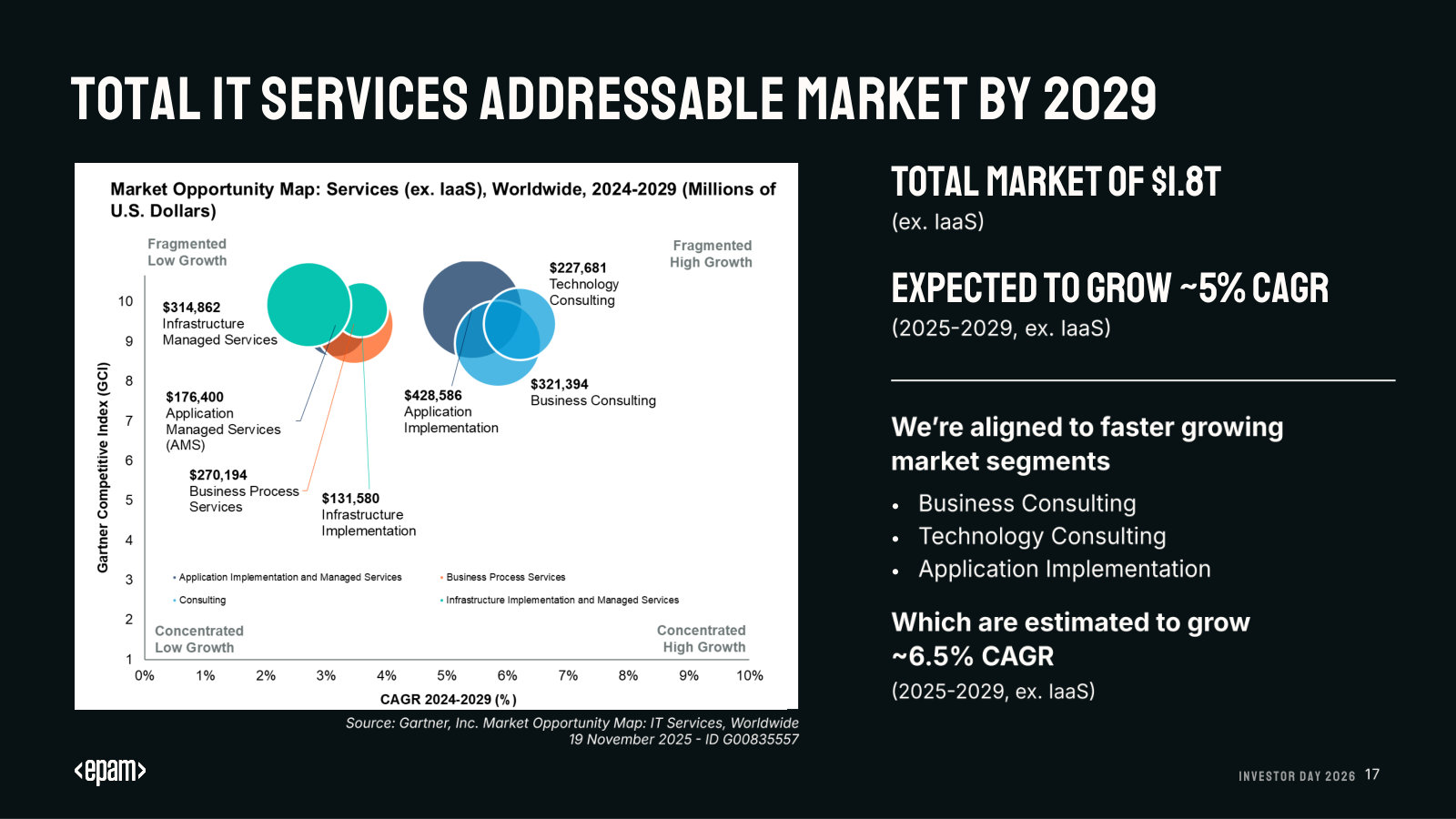

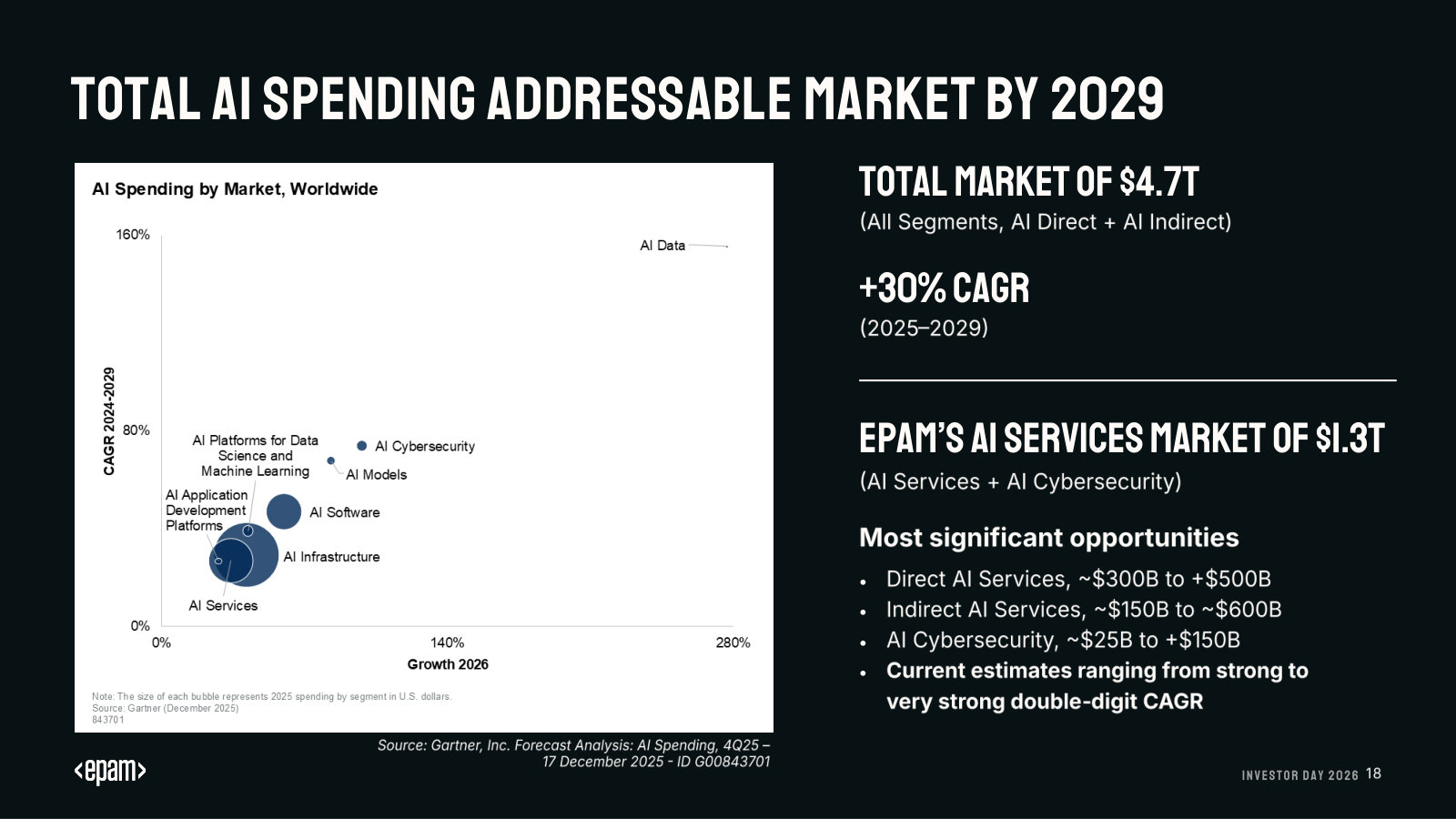

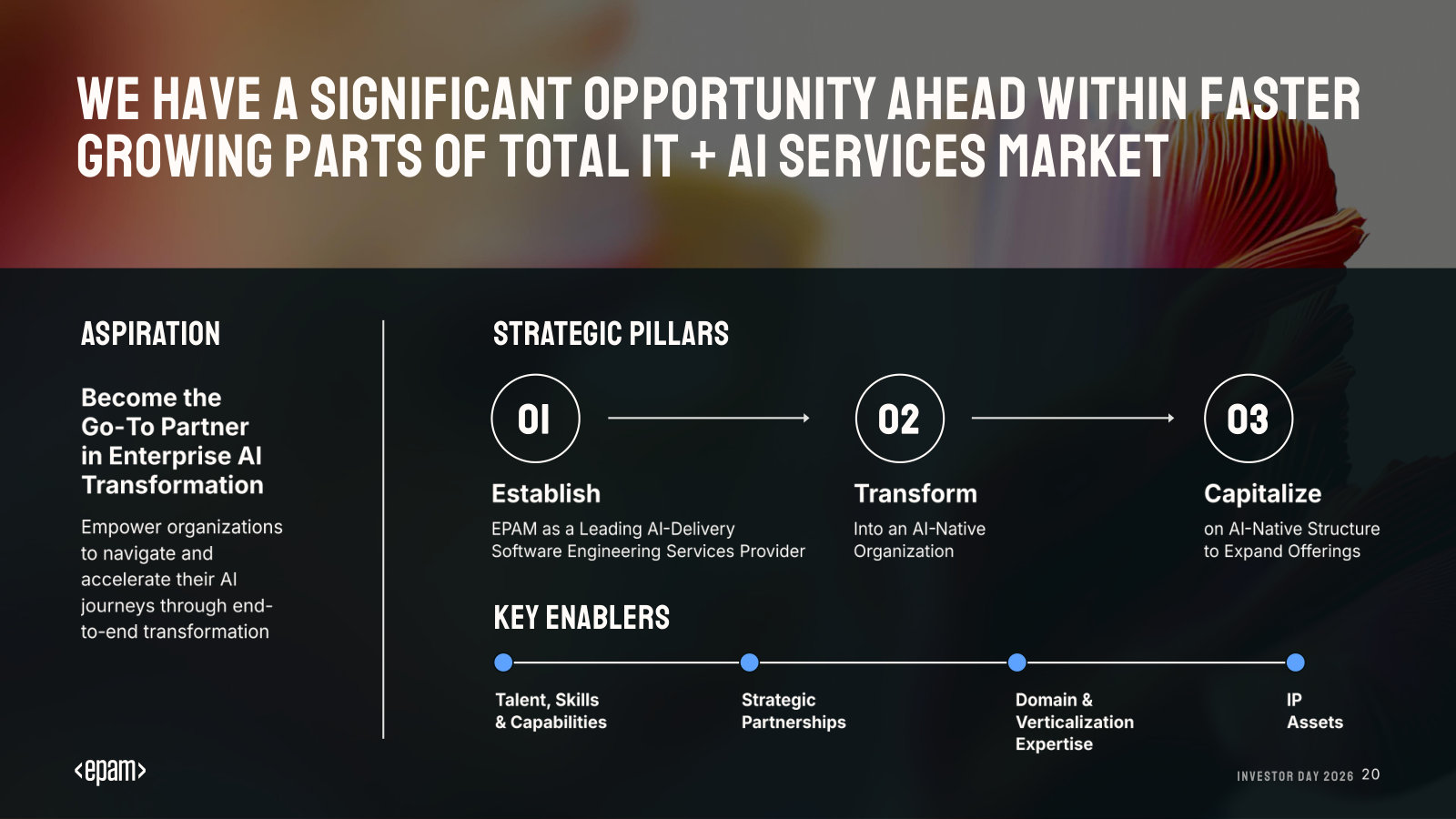

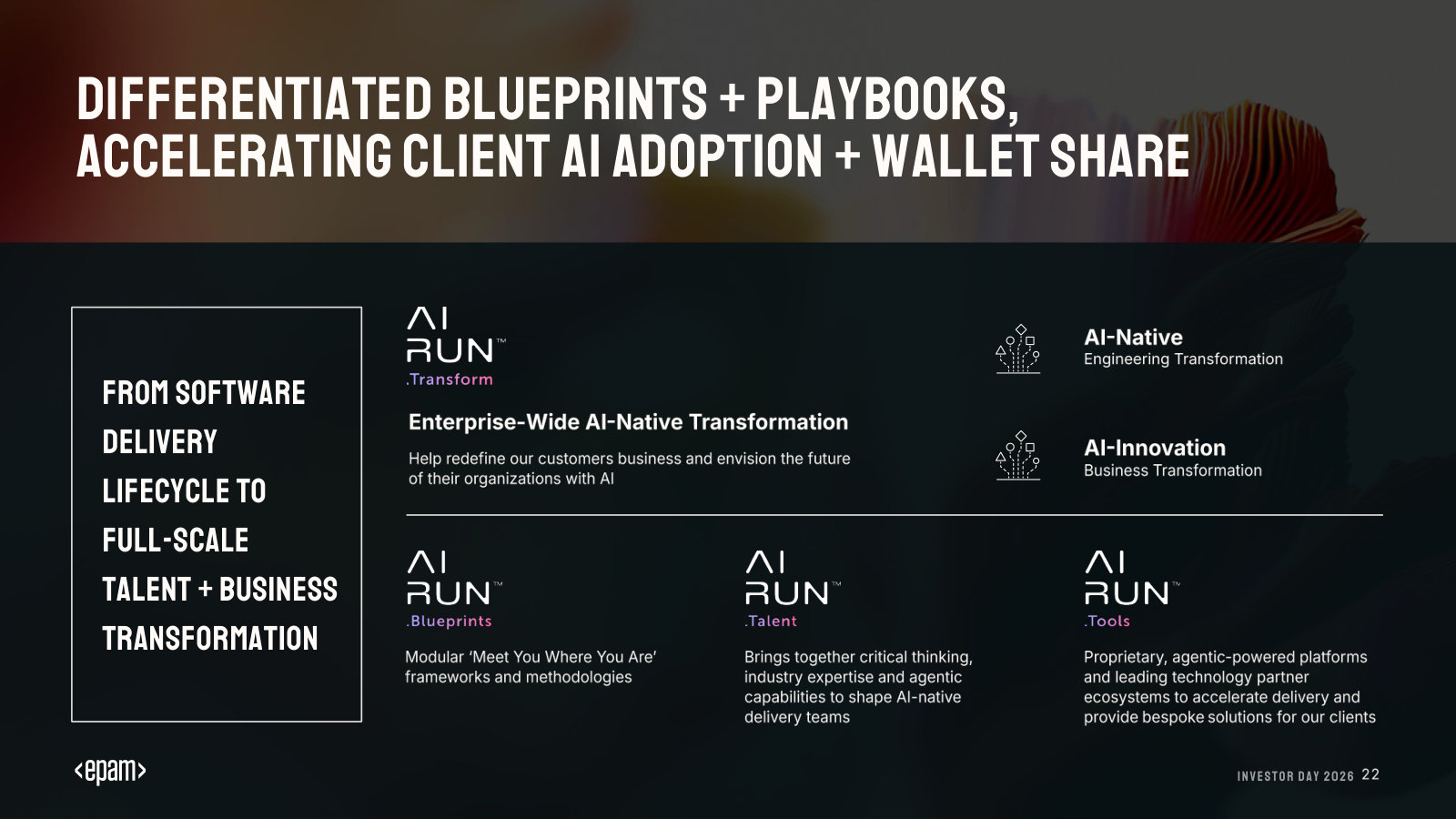

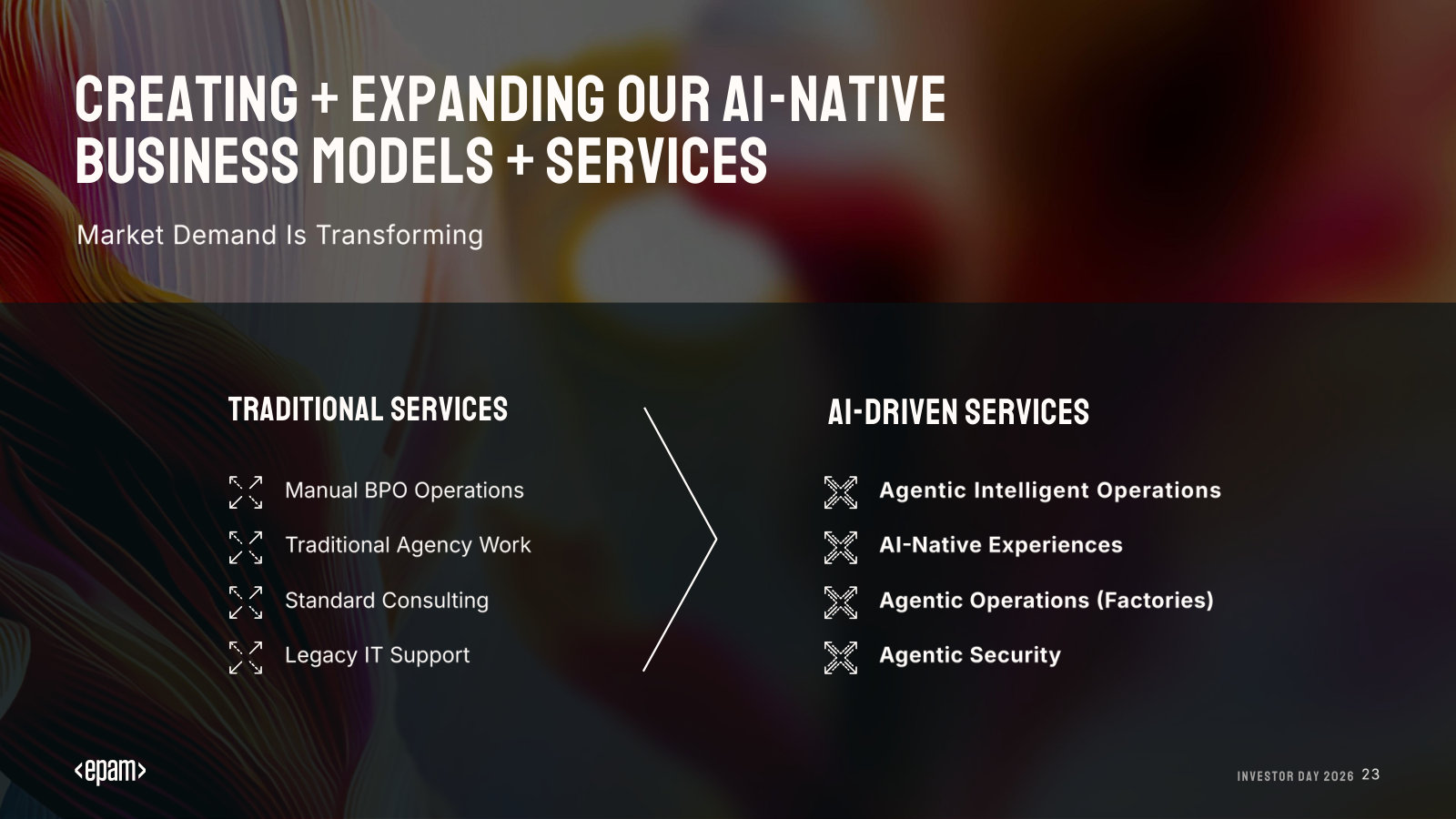

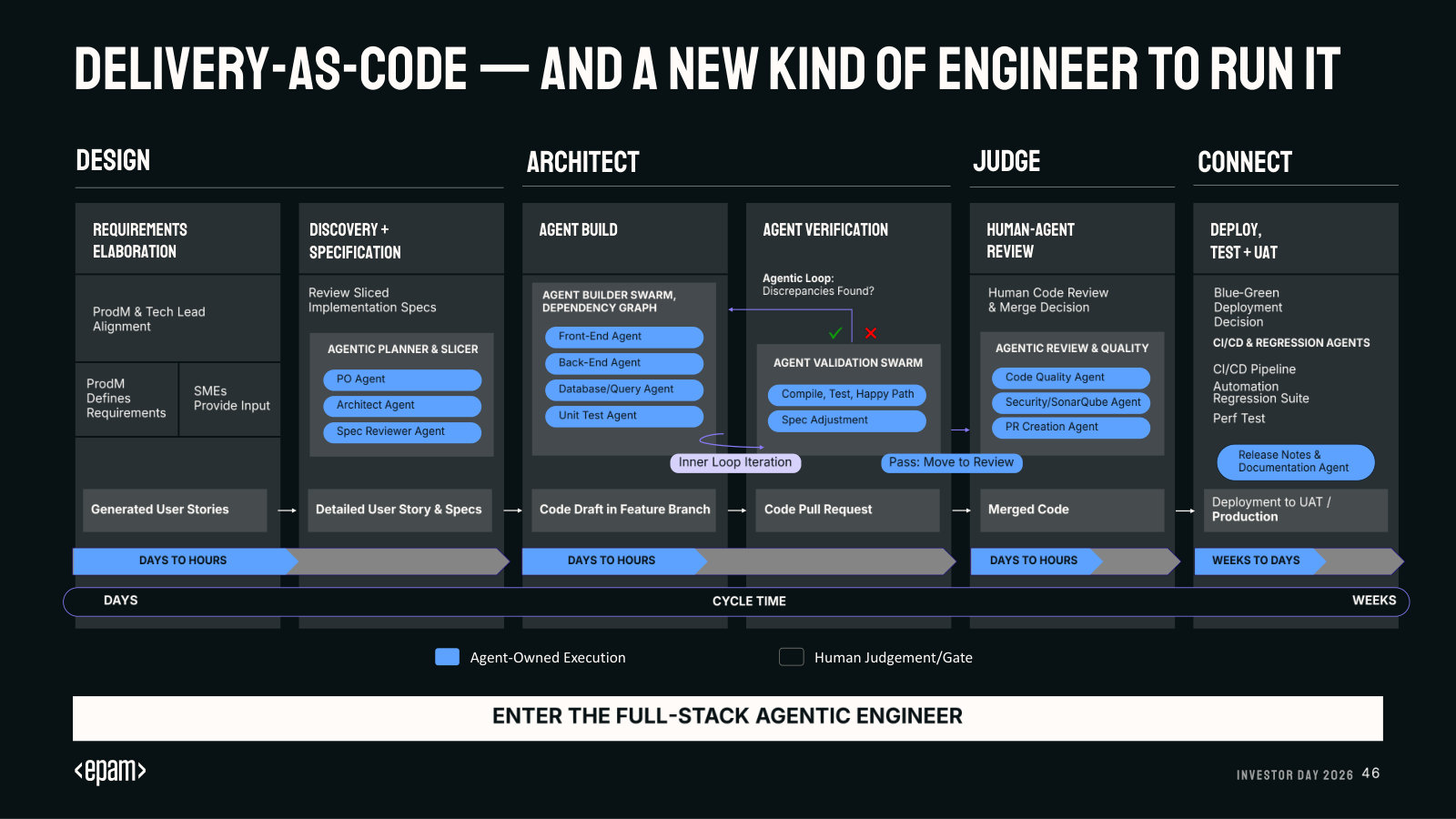

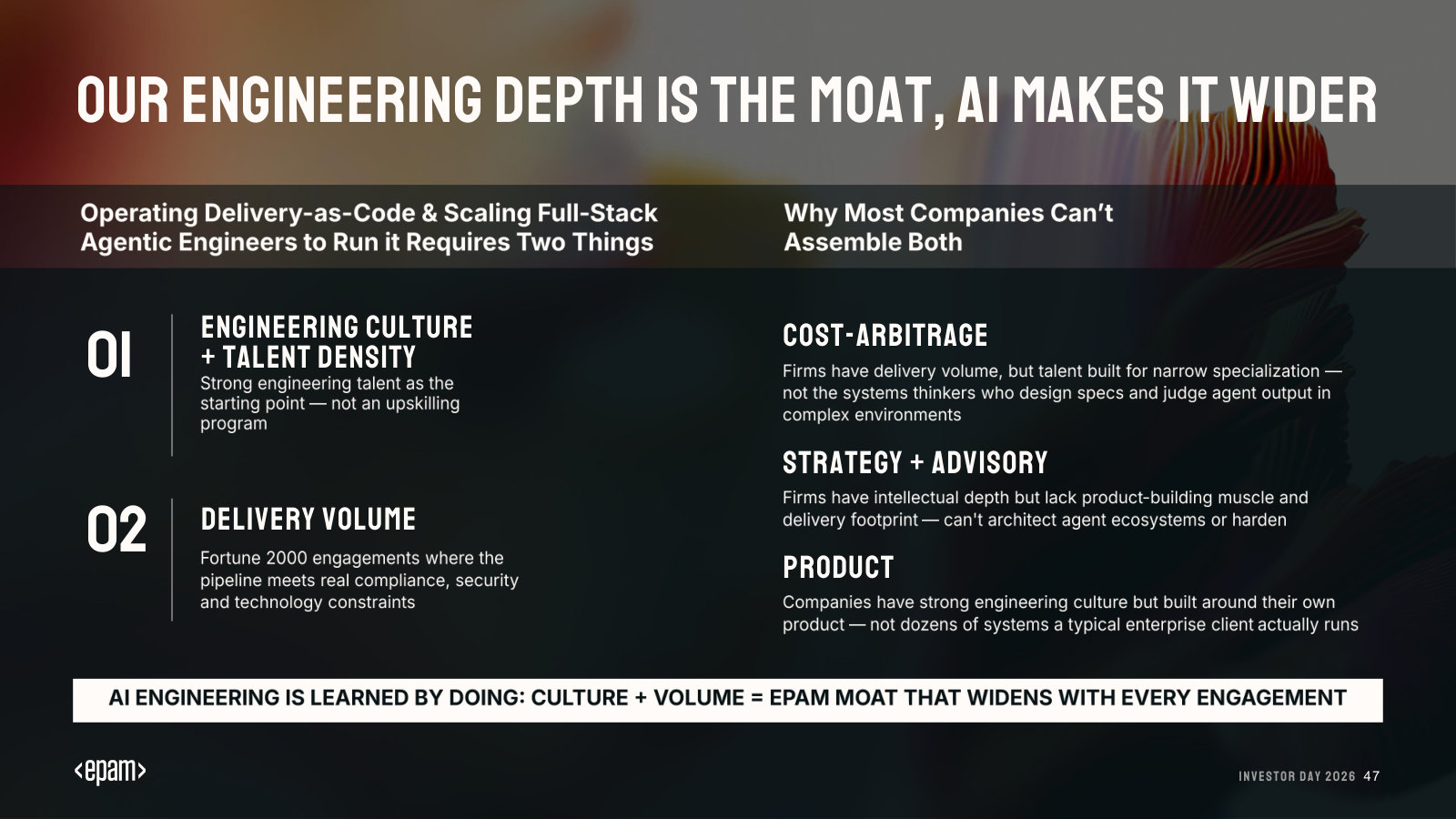

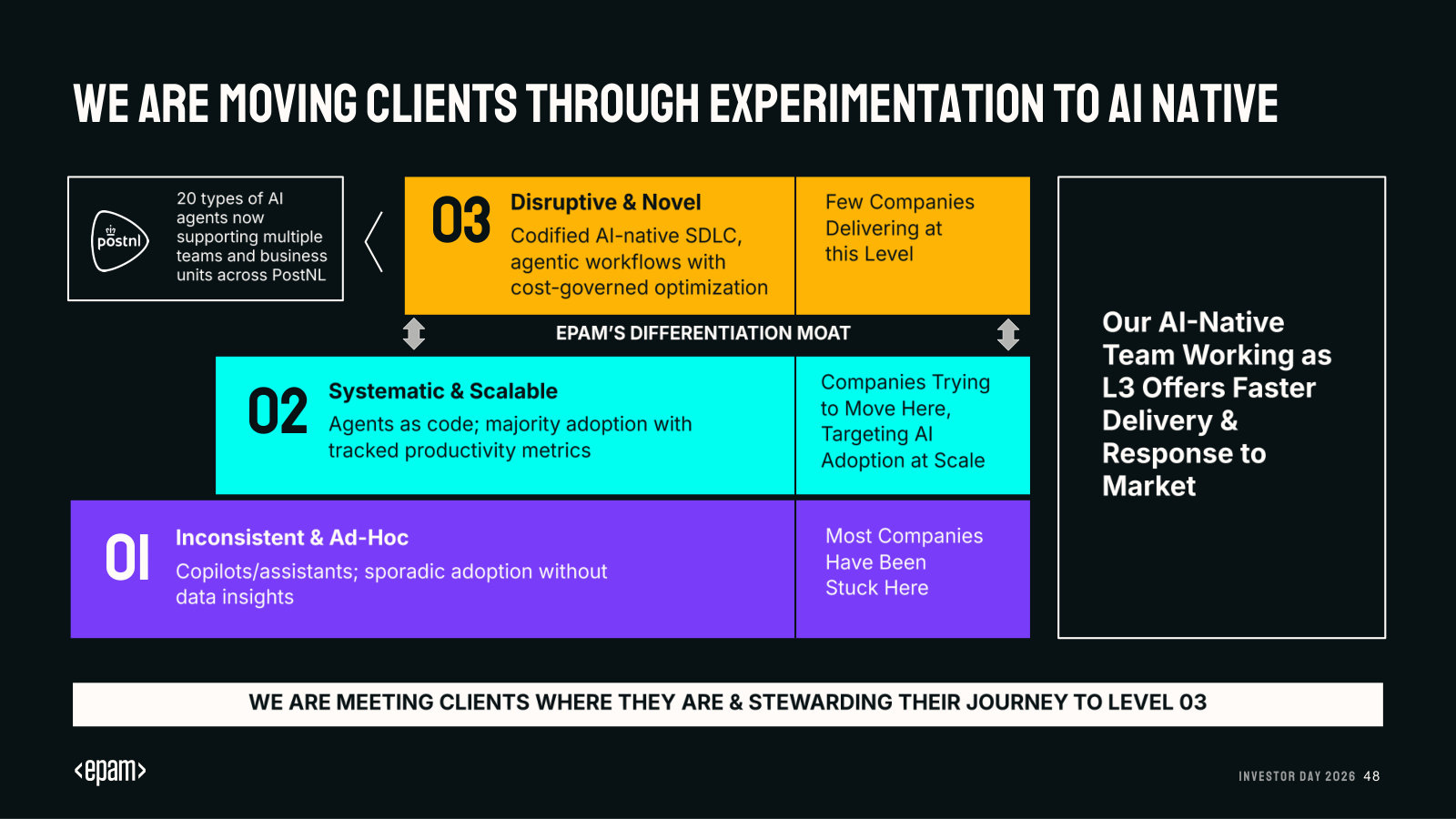

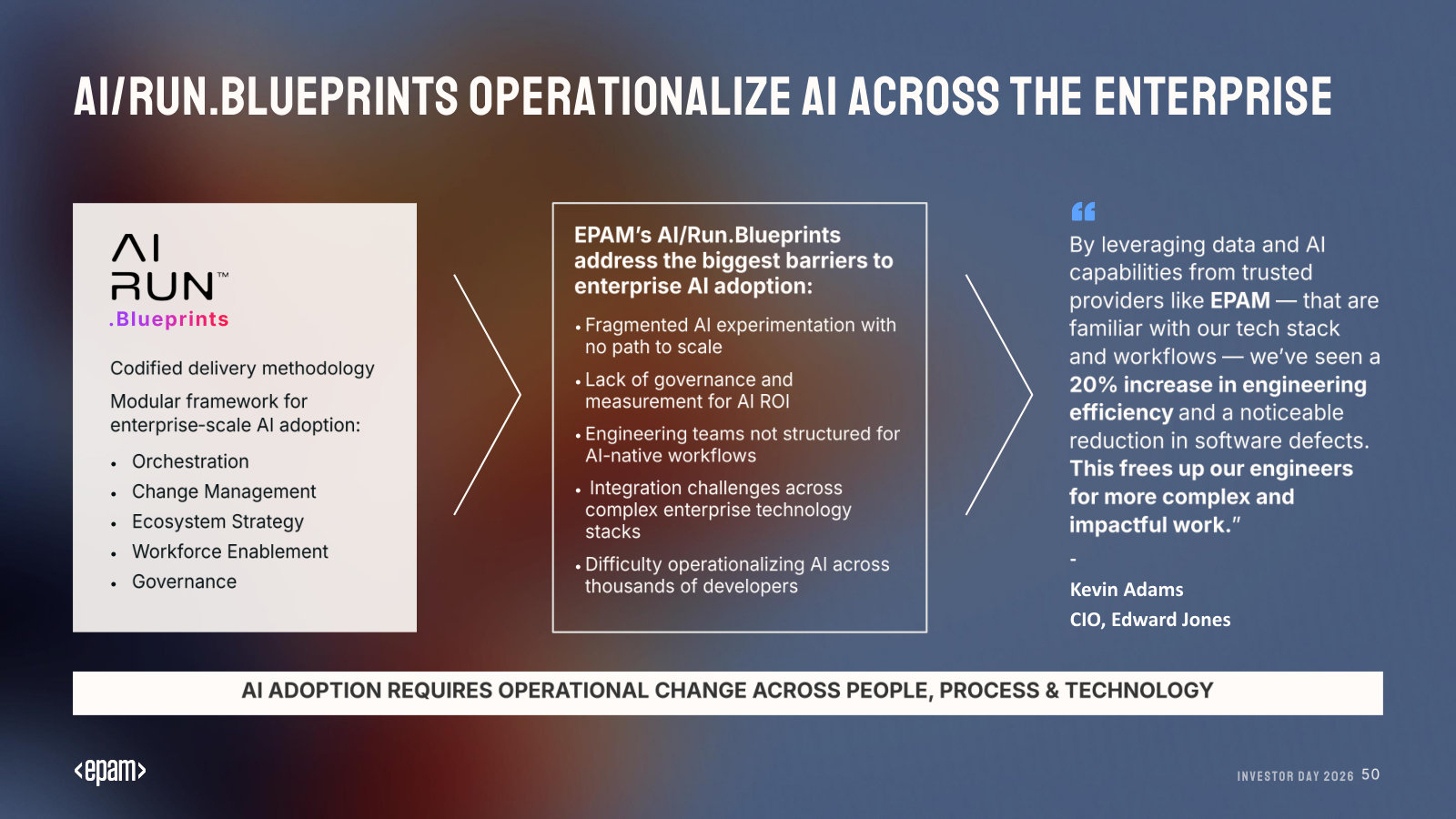

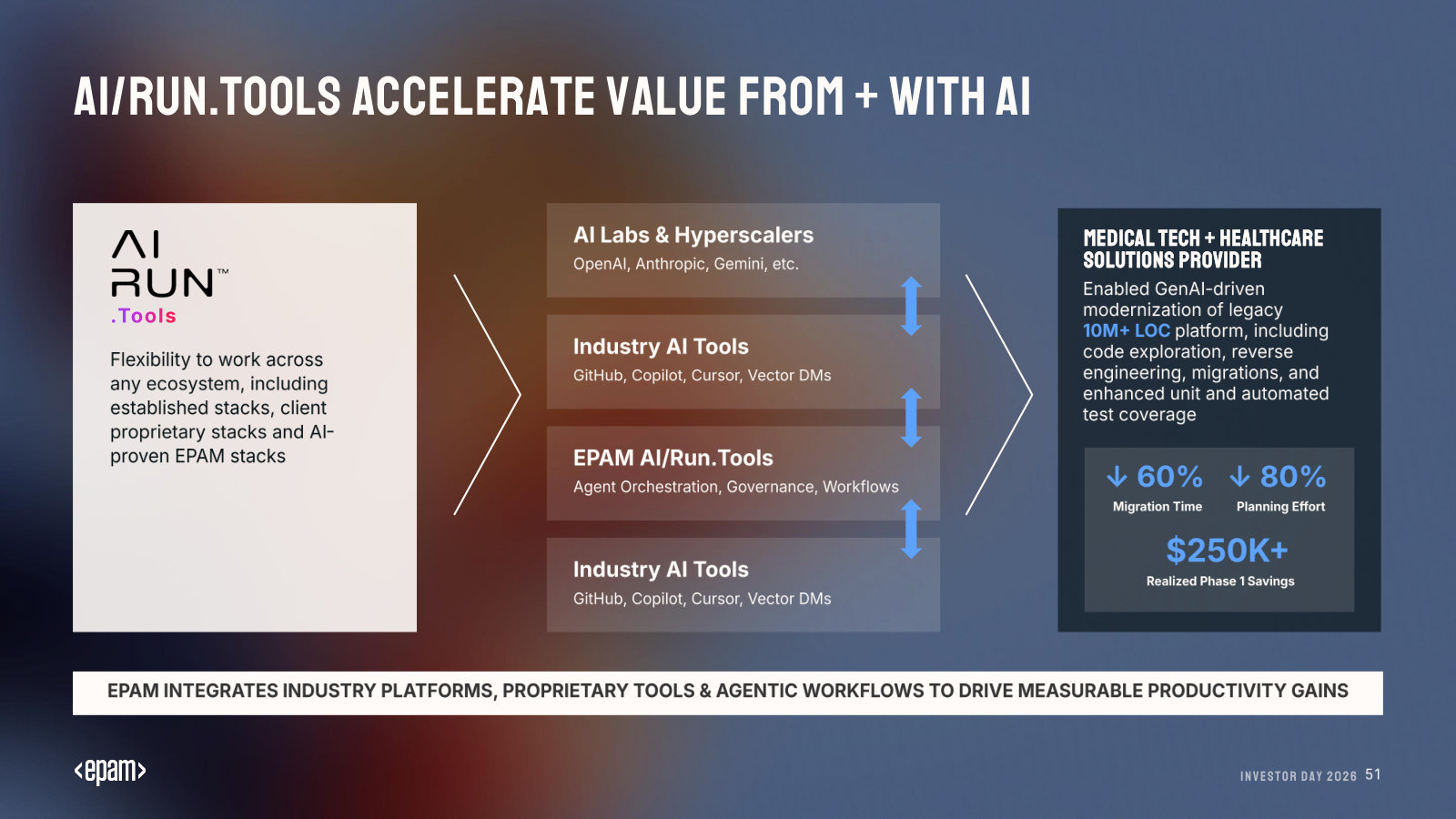

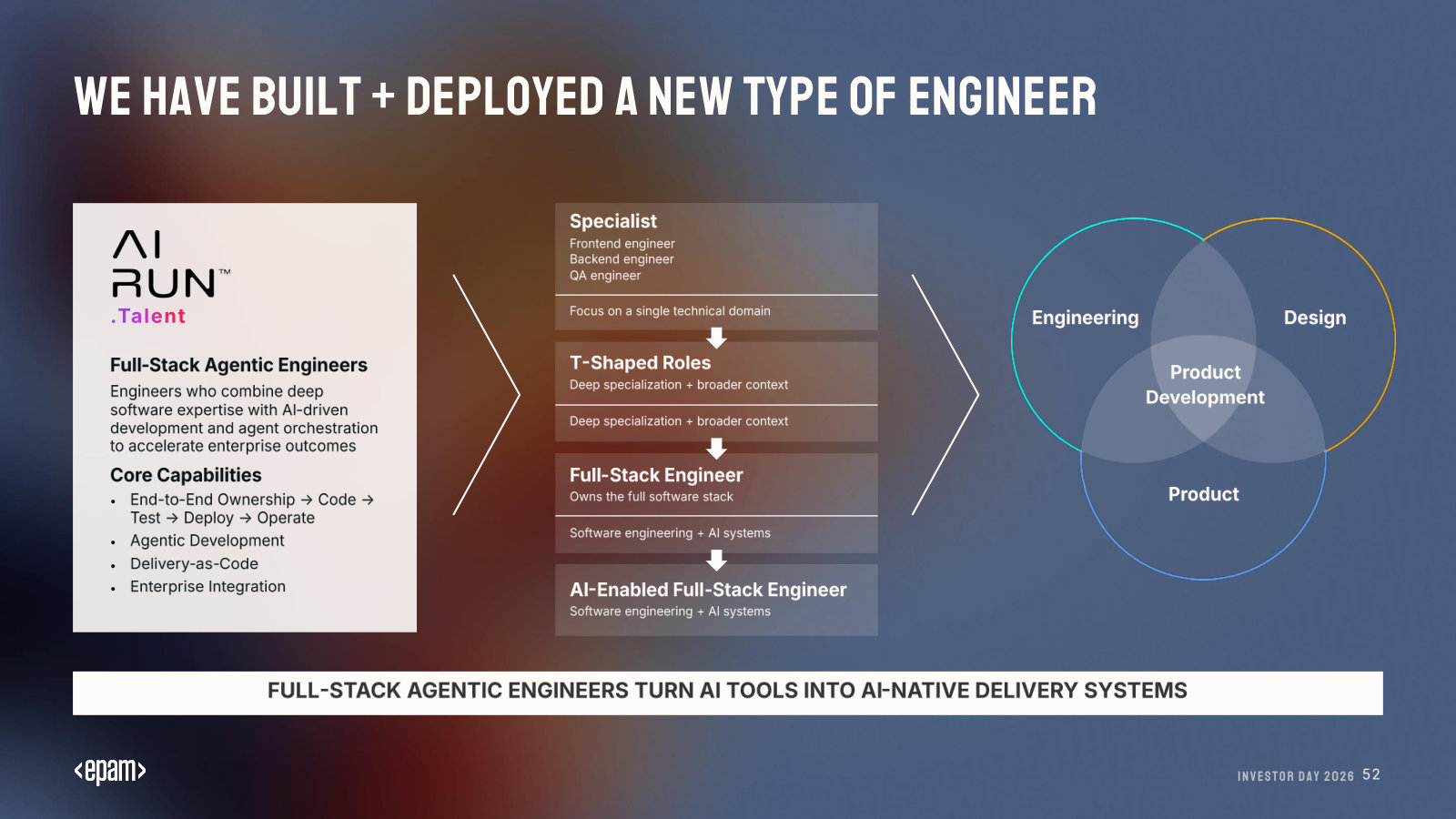

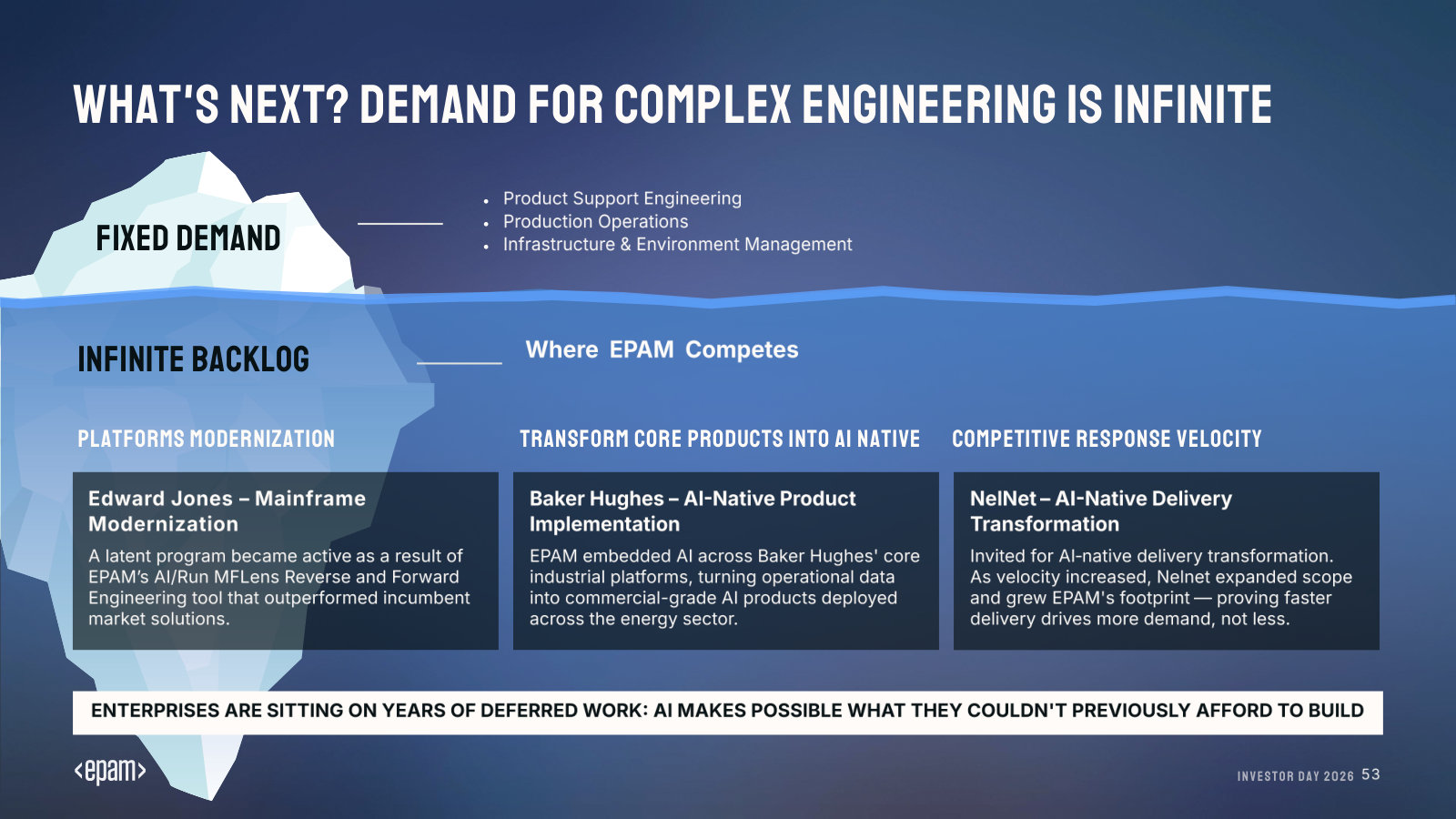

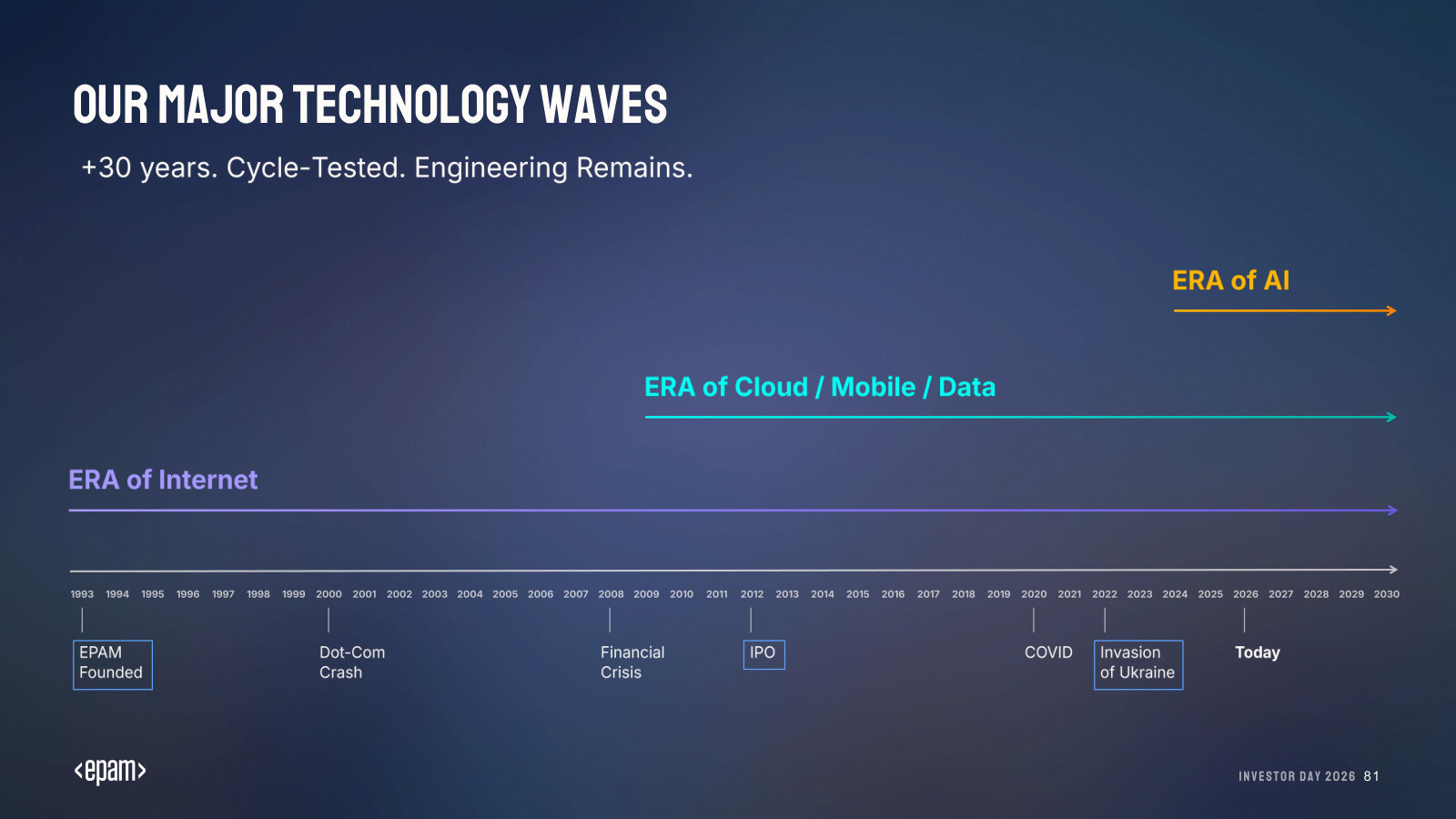

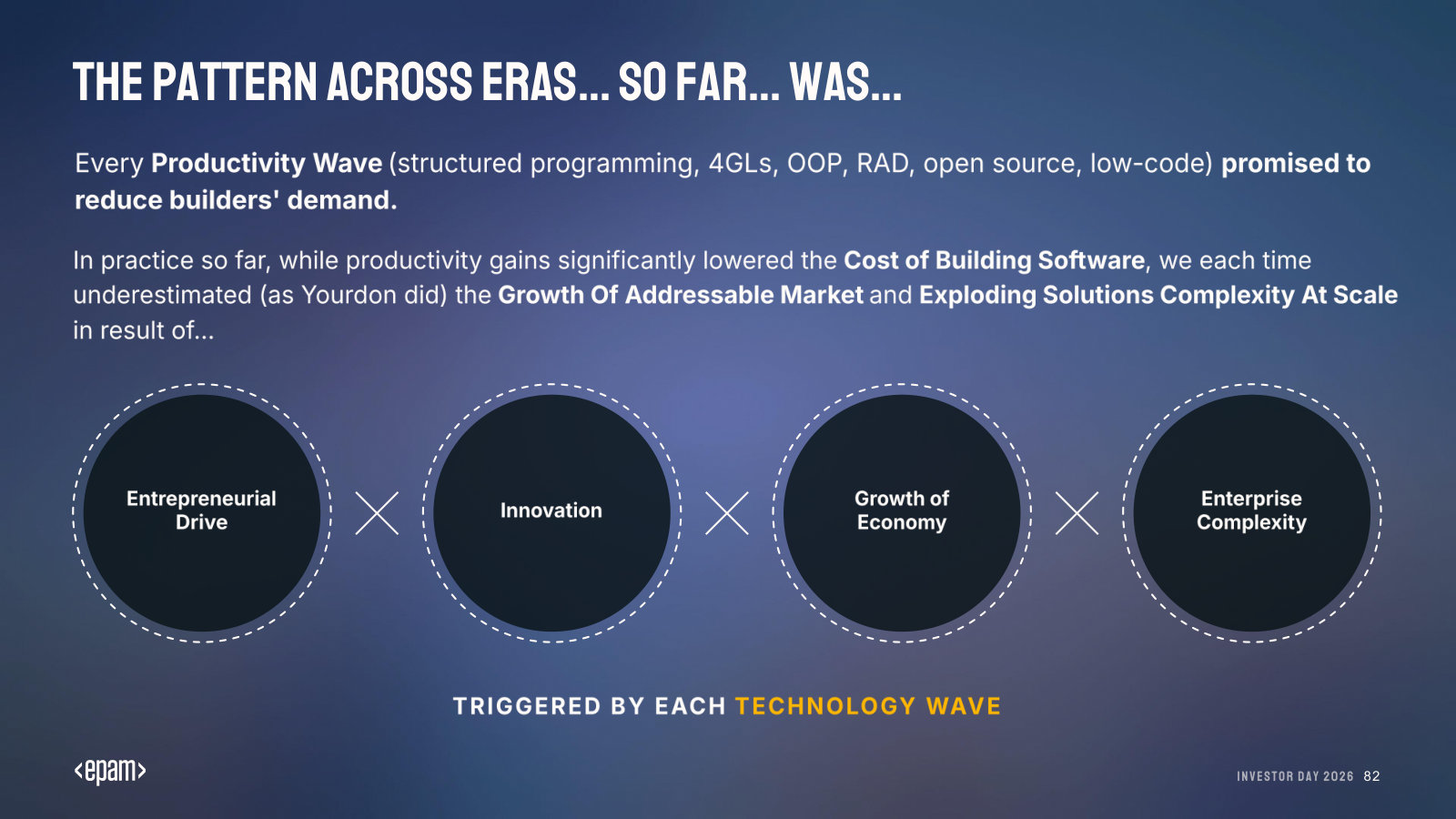

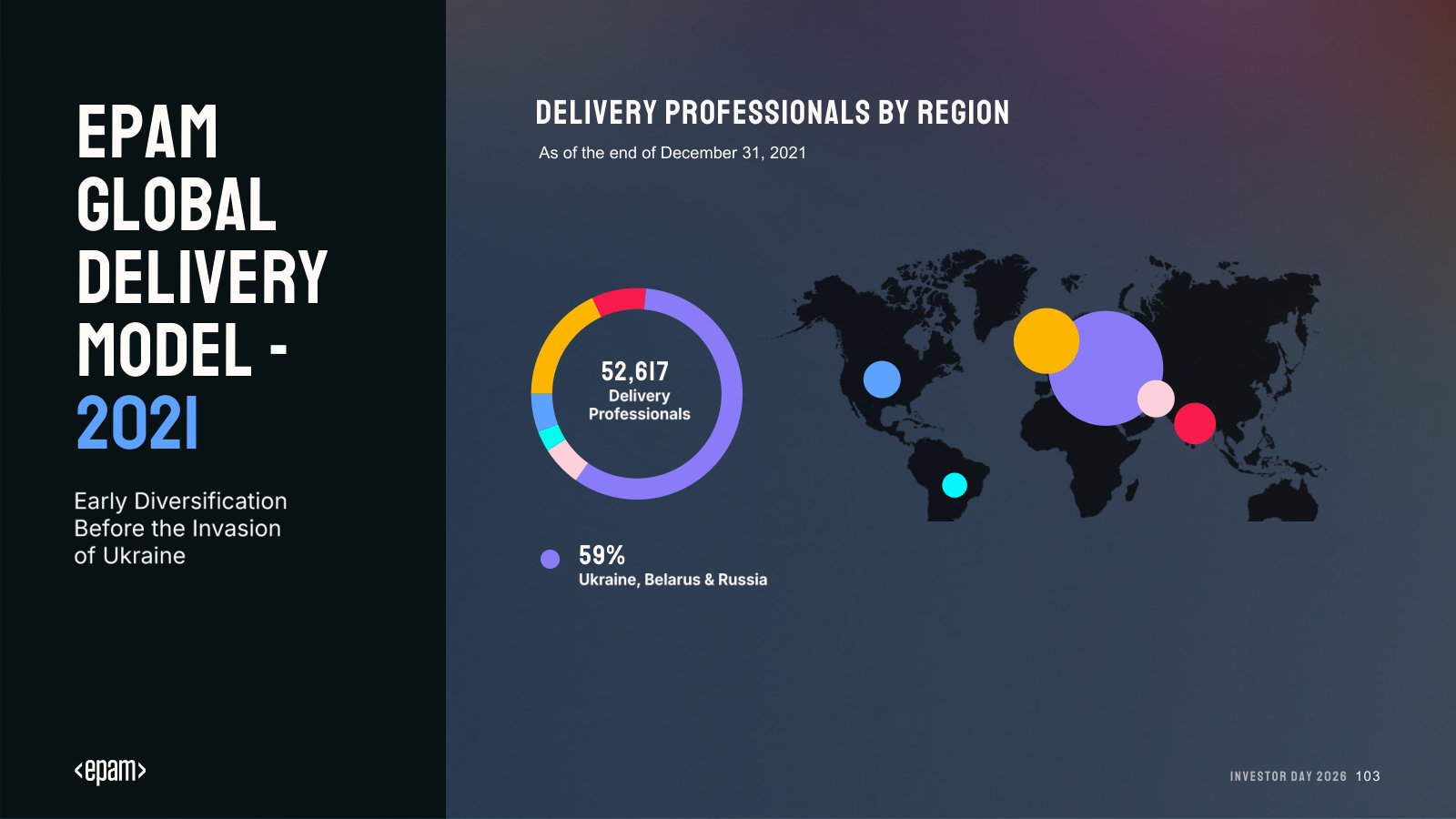

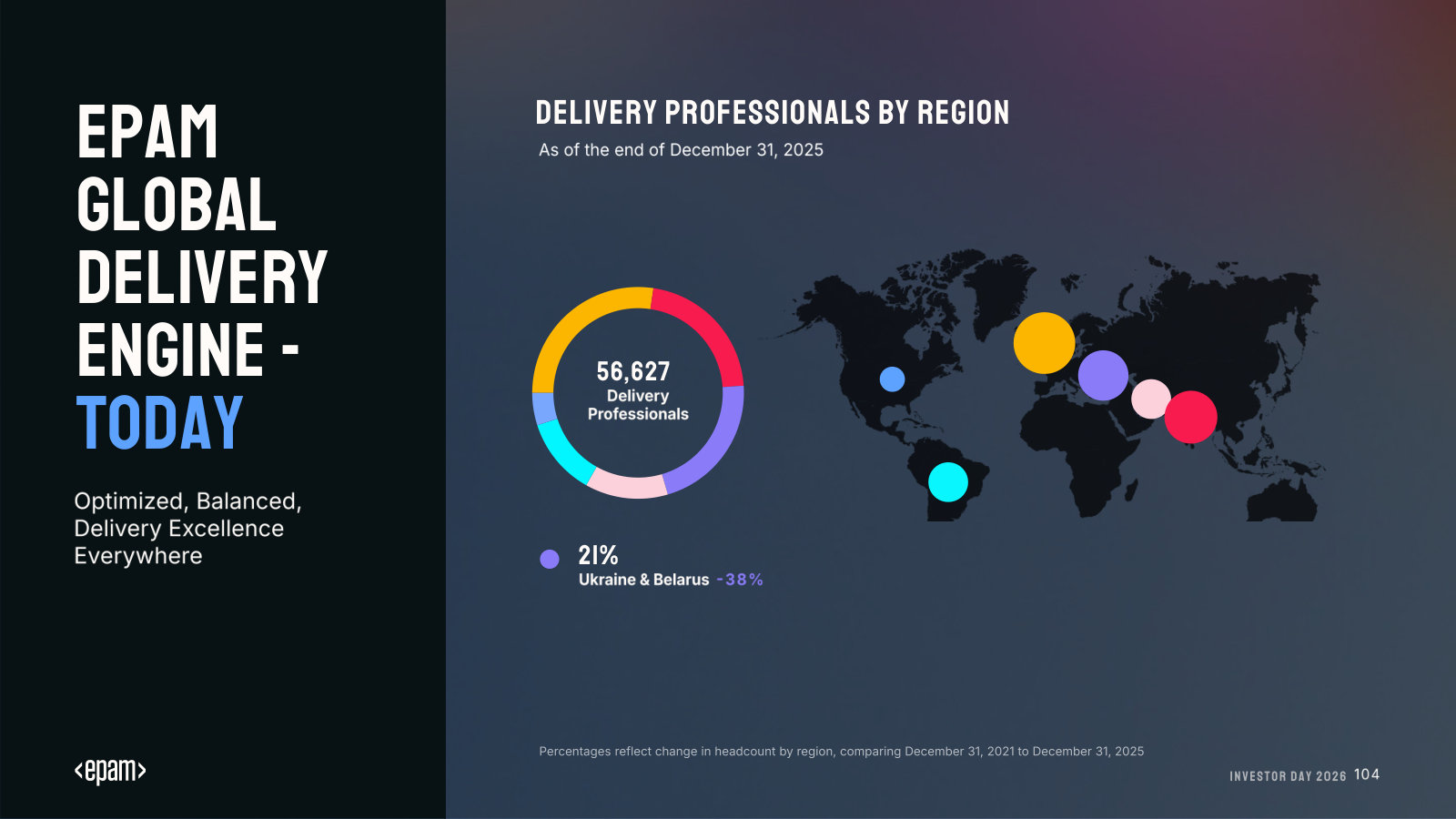

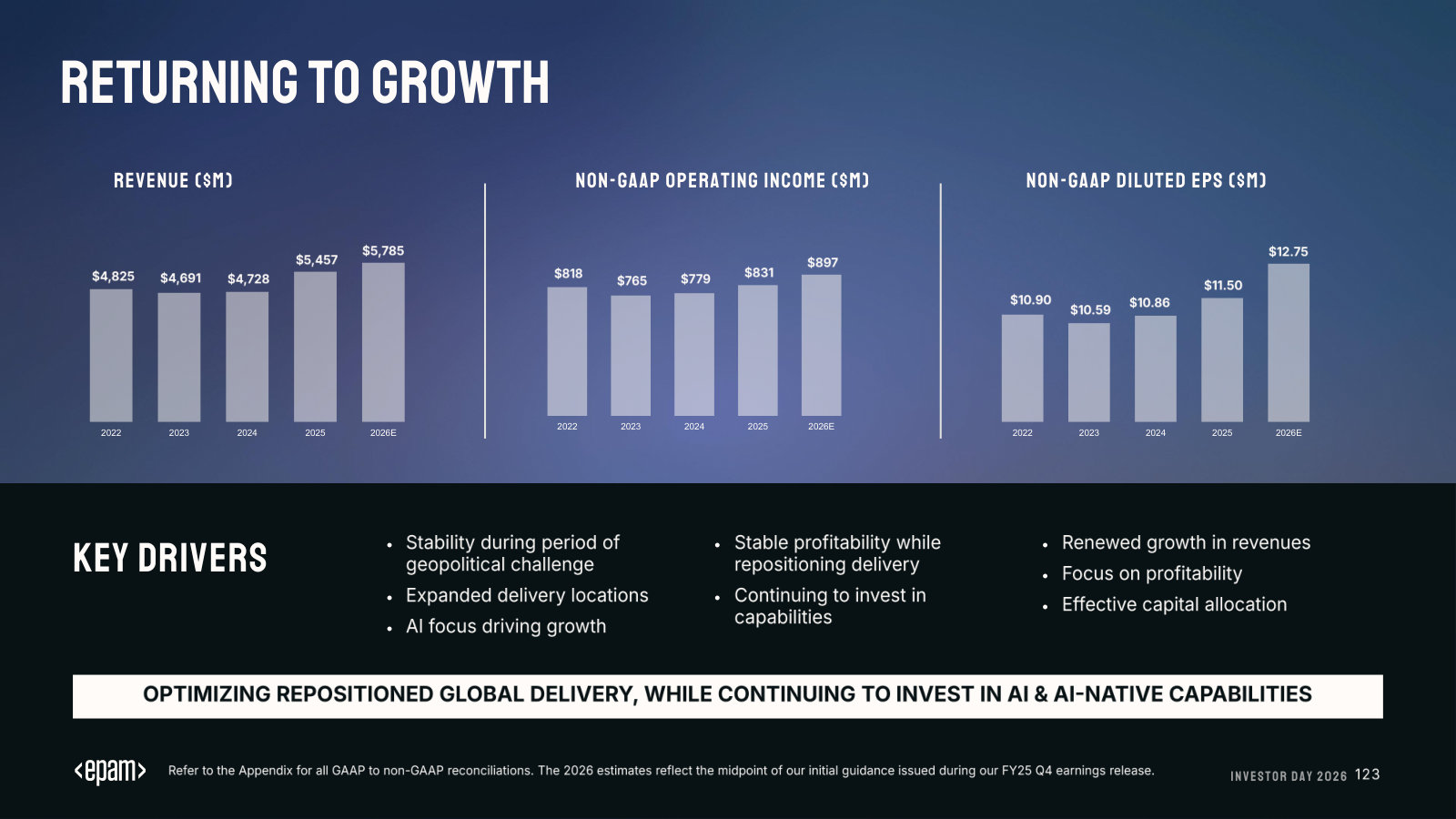

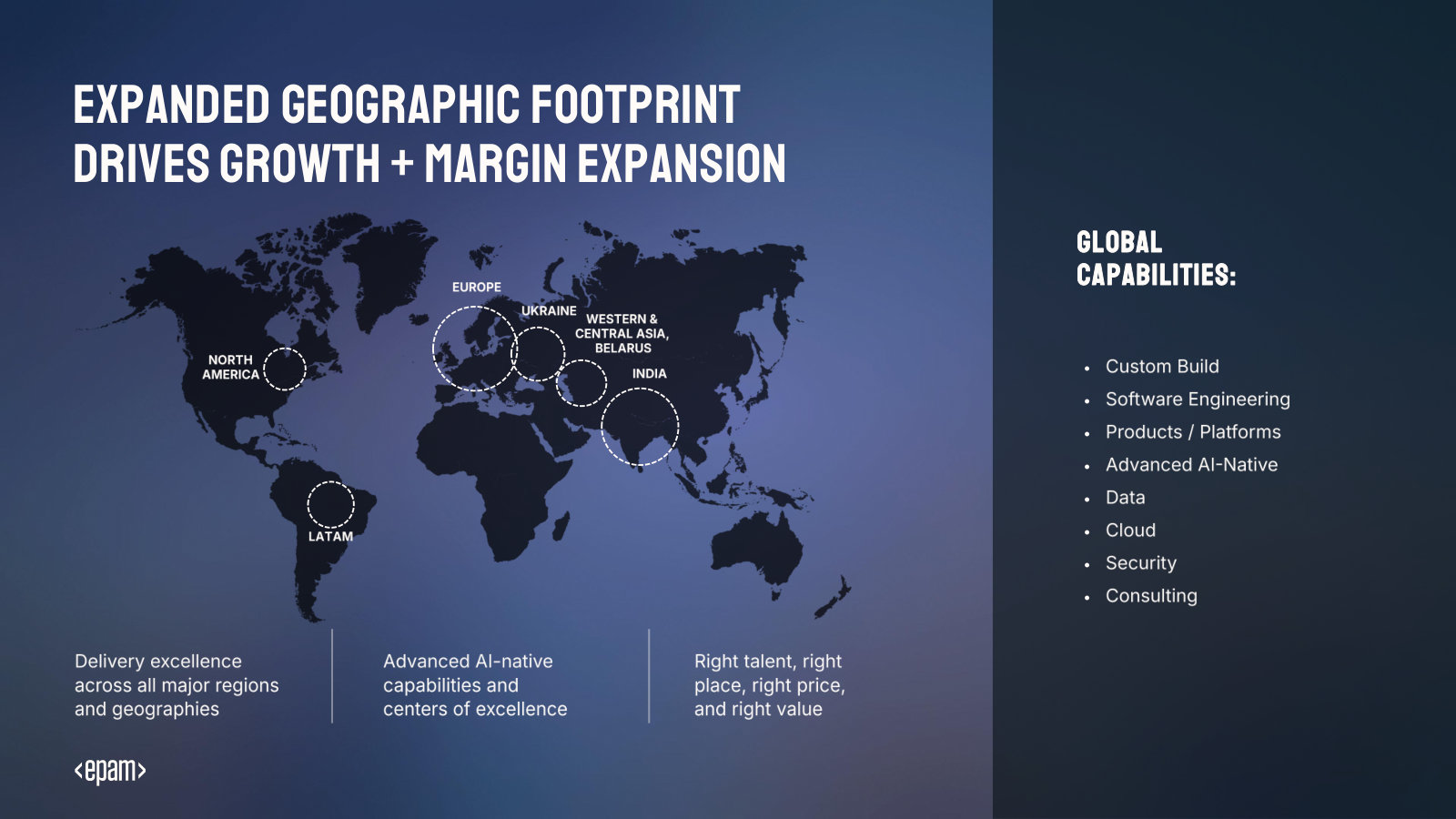

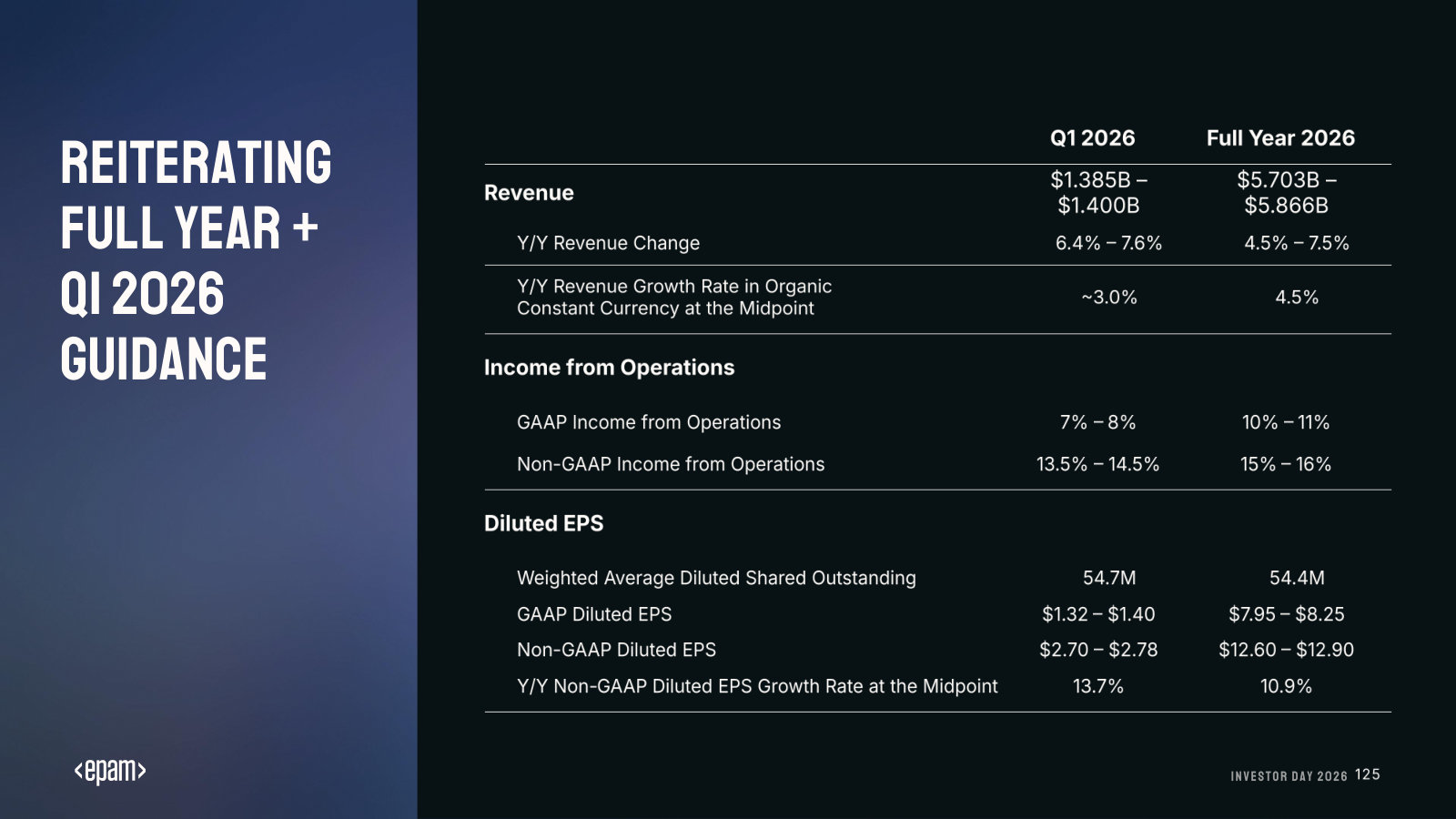

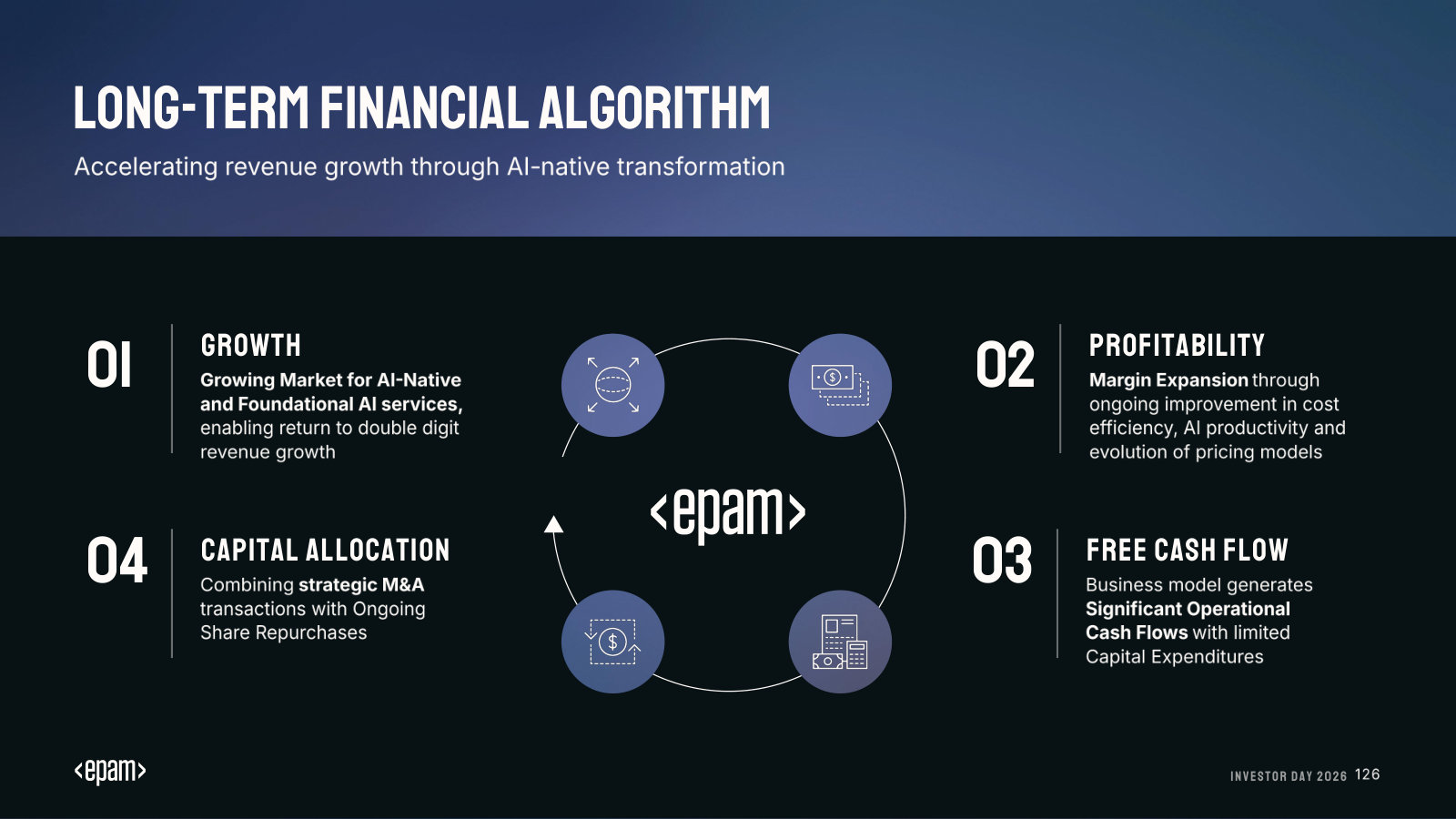

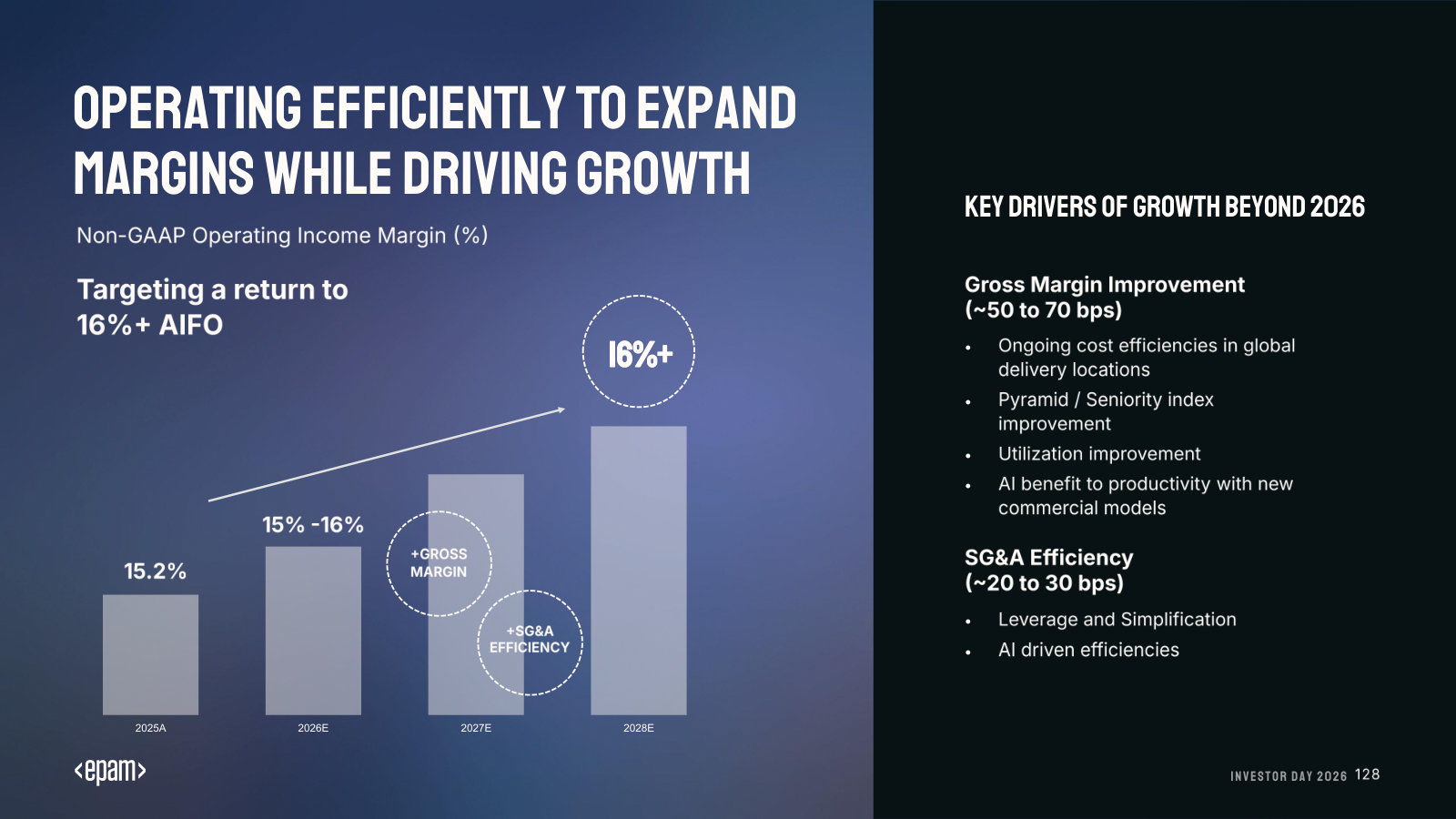

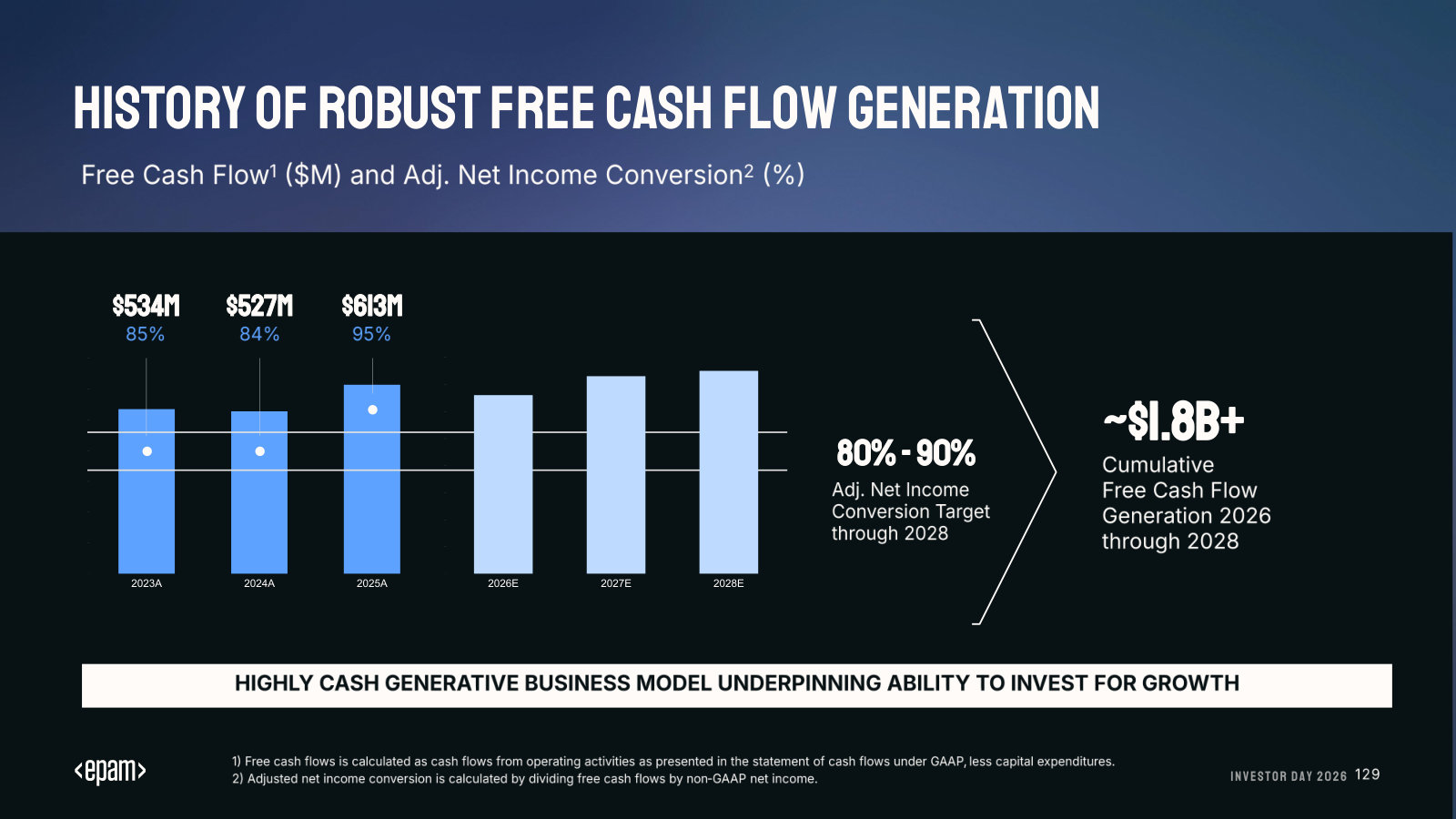

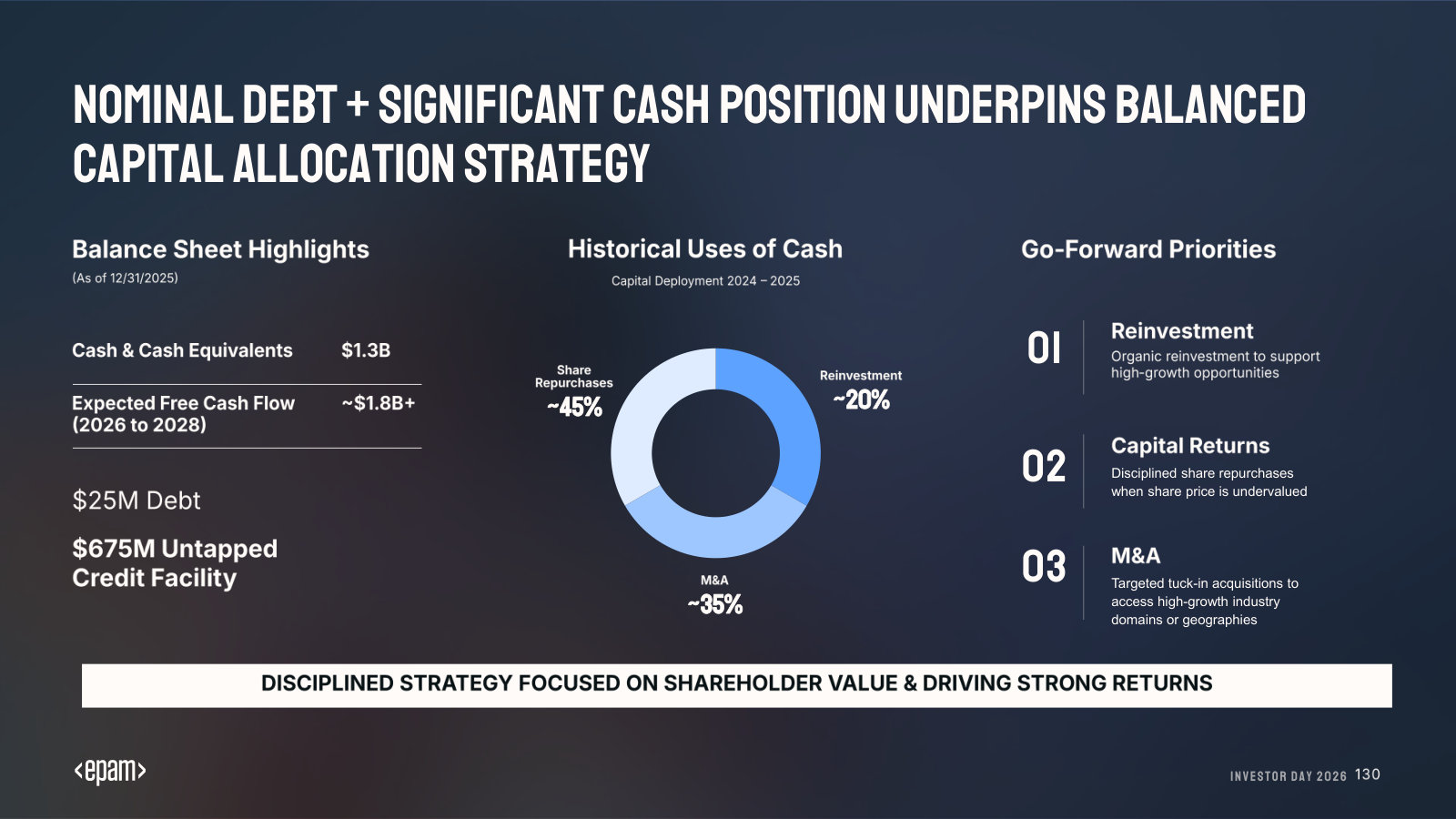

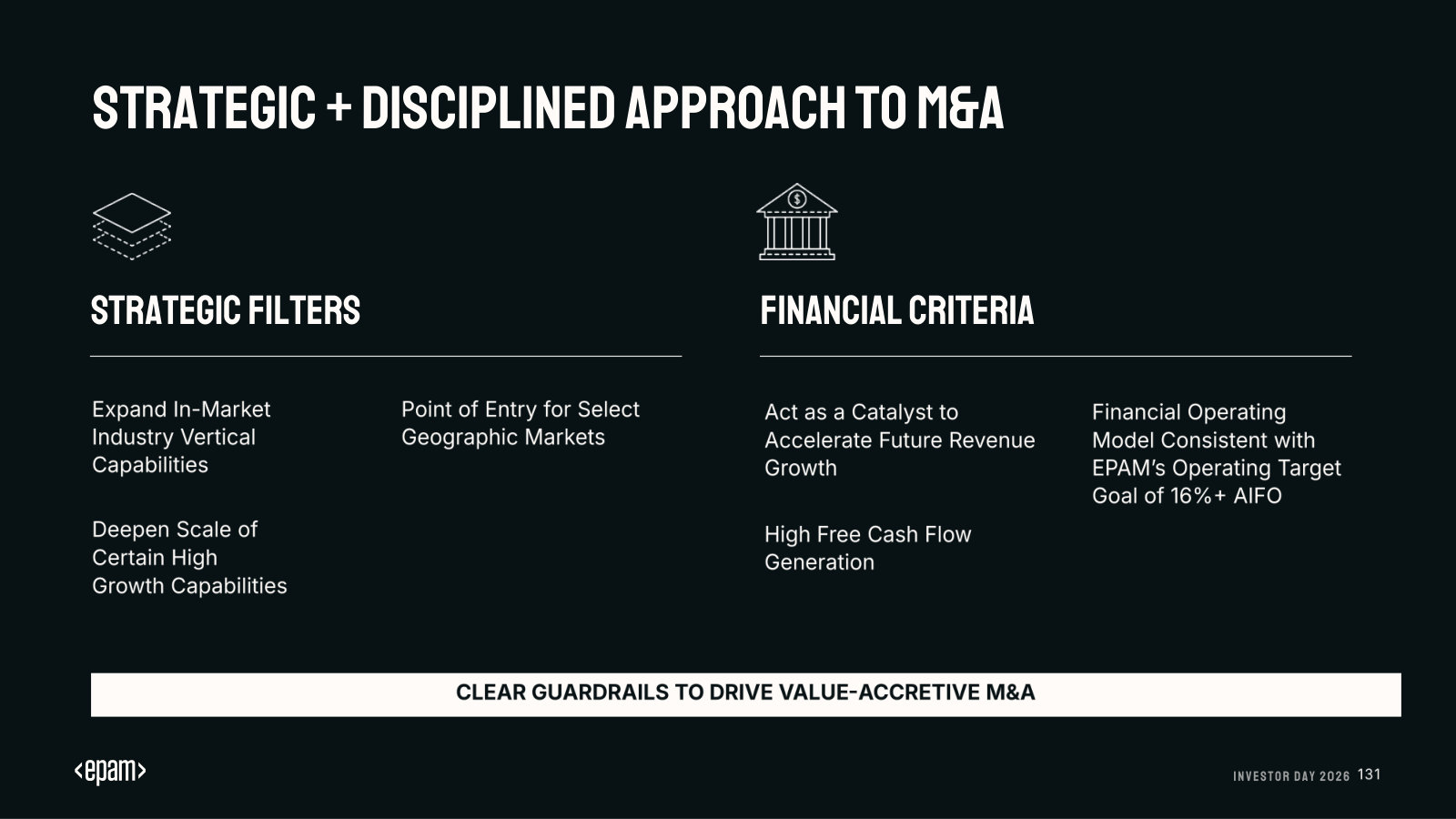

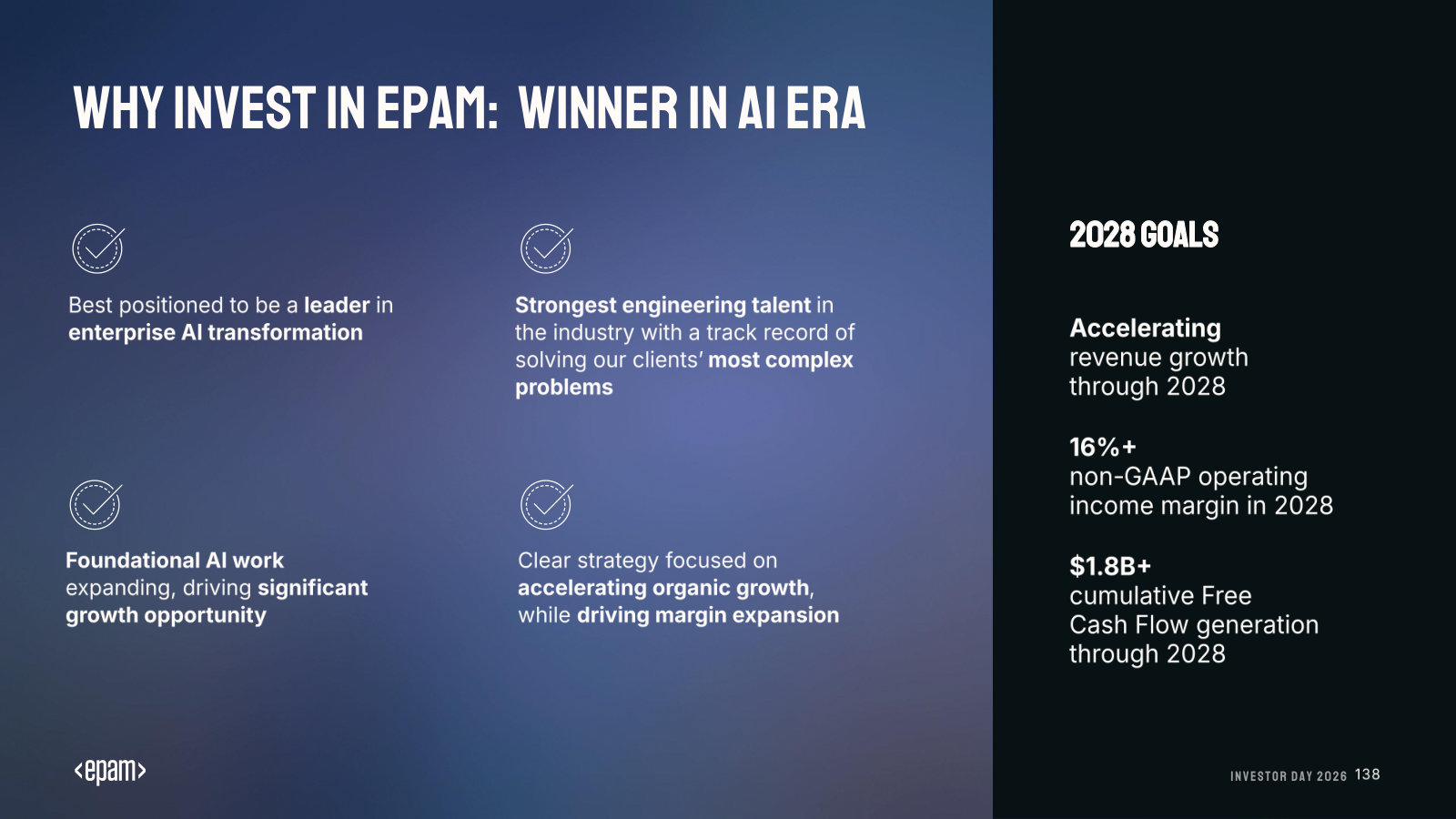

p. 5 — Winning in the AI Era — the four-point thesis and the 2028 targets (accelerating growth, 16%+ margin, $1.8B+ FCF) on one page. · Open the full presentation →p. 7 — Fast Facts, Q1 2026: reported revenue, GAAP/non-GAAP operating income and EPS, plus the revenue split by vertical and geography. · Open the full presentation →p. 9 — We Are Builders — how EPAM frames what it does for clients: solve complexity, cut cost, drive revenue, move to AI-native. · Open the full presentation →p. 10 — Thirty-year timeline through the internet, cloud/mobile and now AI eras — the 'cycle-tested, engineering remains' framing. · Open the full presentation →p. 11 — At a glance: founded 1993, $5.457B revenue (+15.4%), 62,750+ staff, 56,600+ delivery professionals, 55+ countries. · Open the full presentation →p. 12 — 2025 revenue by industry vertical and by geography, with growth rates — where the money comes from. · Open the full presentation →p. 13 — The global delivery engine: 56,600+ delivery professionals spread across regions on one map. · Open the full presentation →p. 14 — Who EPAM serves — 11 industries, 345+ of the Forbes Global 2000, and a wall of named clients. · Open the full presentation →p. 16 — The five cycle-tested strengths EPAM says position it to win: Client Zero, engineering, talent, domain depth, client ties. · Open the full presentation →p. 17 — The multi-year aspiration to be the go-to enterprise-AI partner: Establish, Transform, Capitalize, with key enablers. · Open the full presentation →p. 18 — How demand is shifting — traditional services (BPO, agency, consulting) giving way to AI-driven, agentic equivalents. · Open the full presentation →p. 19 — EPAM's AI maturity ladder: moving clients from ad-hoc copilots up to codified AI-native delivery, the claimed moat. · Open the full presentation →p. 20 — The four growth drivers — talent, domain/verticalization, internal IP, partnerships — with the partner roster. · Open the full presentation →p. 21 — The 'full-stack agentic engineer' — the new talent profile, and which skills are retiring, retained and rising. · Open the full presentation →p. 22 — Three go-to-market 'brand doors' (EPAM, Empathy Lab, EPAM Continuum) aimed at CTO, CMO and business-strategy buyers. · Open the full presentation →p. 23 — The AI/Run offering suite — Transform, Blueprints, Talent and Tools — that packages the AI-native services. · Open the full presentation →p. 34 — The long-term financial algorithm: growth, profitability, free cash flow and capital allocation as one flywheel. · Open the full presentation →p. 35 — Revenue, non-GAAP operating income and EPS, 2022–2026E — the 'returning to growth' picture in three bar charts. · Open the full presentation →p. 36 — Free cash flow history and the 80–90% conversion target — the case for a cash-generative model. · Open the full presentation →p. 37 — Capital allocation: how cash was deployed in 2024–25 (buybacks, M&A, reinvestment) and the go-forward priorities. · Open the full presentation →p. 38 — FY26 and Q2 2026 guidance: revenue, margin and EPS ranges — the near-term numbers management is committing to. · Open the full presentation →

Management's fullest statement of strategy — the AI-native thesis, the engineering-moat argument, the delivery model, and 2028 targets. · Open the full document →

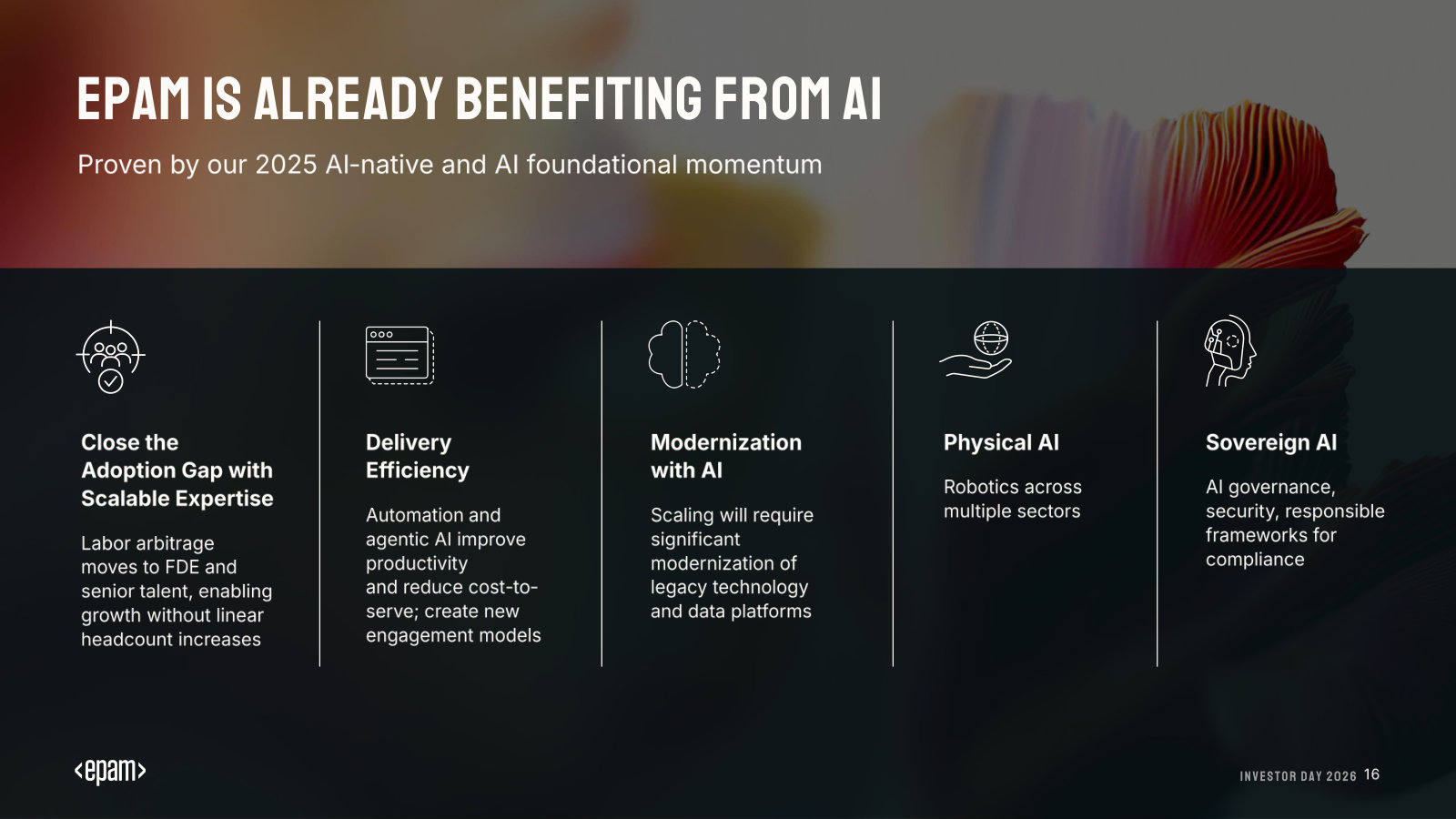

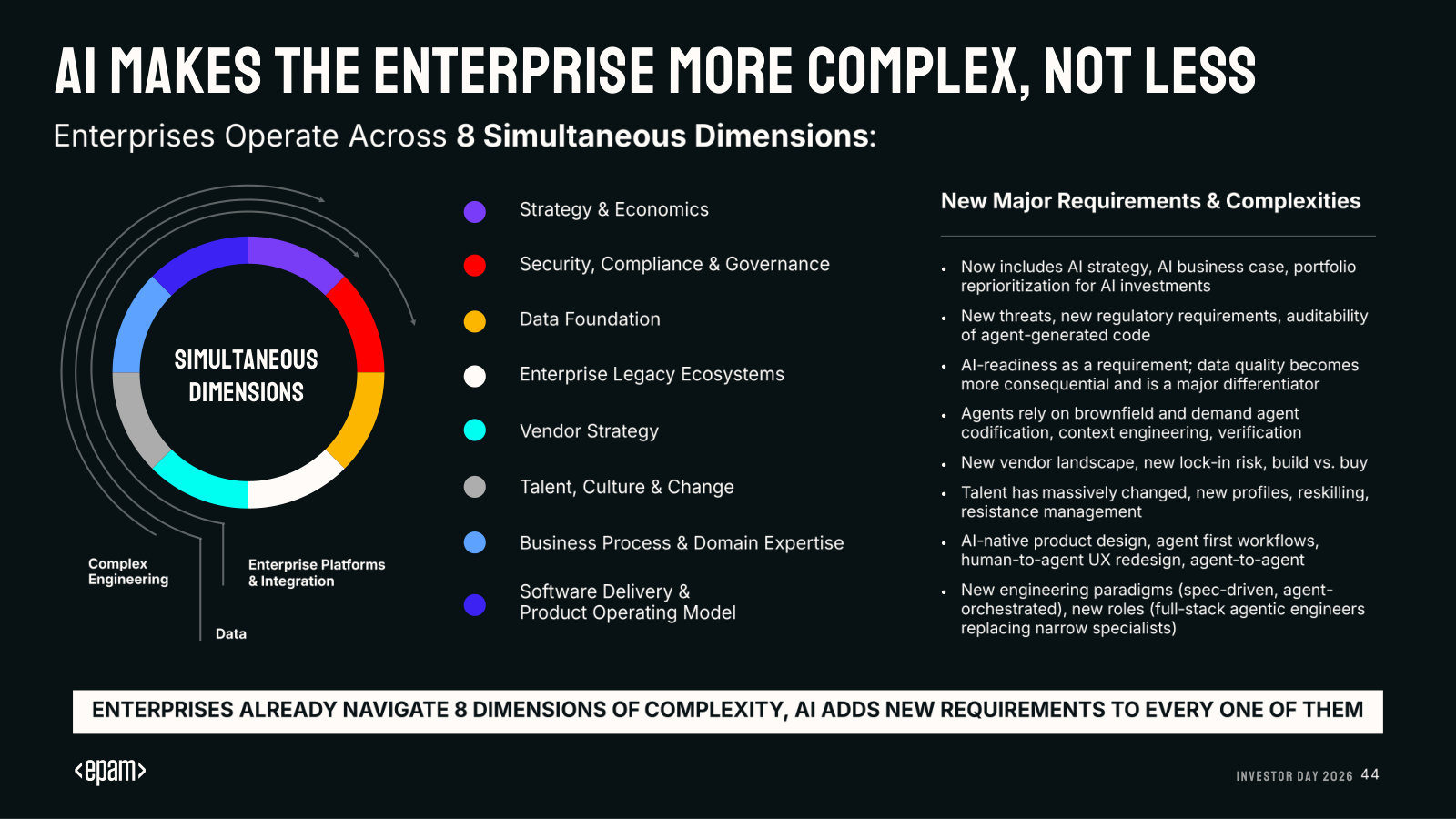

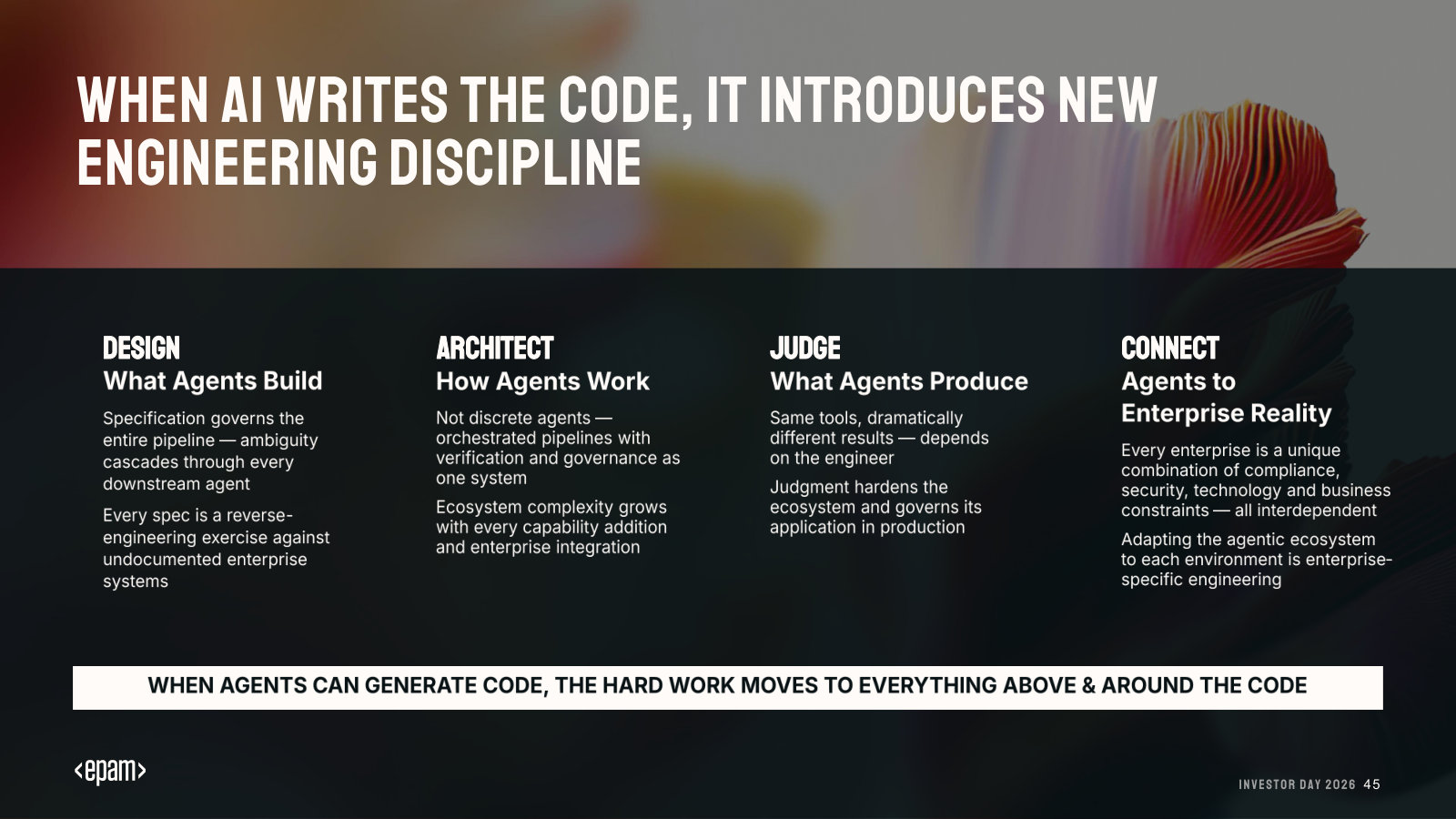

p. 11 — At a glance: 1993 founding, $5.457B revenue (+15.4%), 62,000+ staff, 56,600+ delivery professionals, 55+ countries. · Open the full presentation →p. 12 — 2025 revenue by industry vertical and geography, with growth rates — the shape of the business. · Open the full presentation →p. 13 — We Are Builders — the client-value framing: solve complexity, cut cost, drive revenue, accelerate AI-native change. · Open the full presentation →p. 14 — Who EPAM serves — 11 industries, 345+ of the Forbes Global 2000, and the named-client roster. · Open the full presentation →p. 16 — Where EPAM says it already benefits from AI: closing the adoption gap, delivery efficiency, modernization, physical/sovereign AI. · Open the full presentation →p. 17 — Gartner's IT-services market map: a $1.8T market, and the faster-growing consulting/implementation segments EPAM targets. · Open the full presentation →p. 18 — The AI-spending TAM: $4.7T total, EPAM's addressable $1.3T in AI services and cybersecurity, growing ~30% a year. · Open the full presentation →p. 19 — The five cycle-tested strengths behind the thesis: Client Zero, engineering, talent, domain depth, client relationships. · Open the full presentation →p. 20 — The aspiration to be the go-to enterprise-AI partner — Establish, Transform, Capitalize — and the key enablers. · Open the full presentation →p. 22 — The AI/Run suite — Transform, Blueprints, Talent, Tools — packaging the shift from software delivery to full transformation. · Open the full presentation →p. 23 — How demand is shifting: traditional BPO, agency and consulting work giving way to agentic, AI-native services. · Open the full presentation →p. 44 — The demand thesis: AI adds new requirements to all eight dimensions of enterprise complexity, not fewer. · Open the full presentation →p. 45 — When agents write the code, the hard work moves to Design, Architect, Judge and Connect — a new engineering discipline. · Open the full presentation →p. 46 — Delivery-as-Code: the agentic software lifecycle as a swimlane, showing where agents execute and where humans still gate. · Open the full presentation →p. 47 — The competitive argument: engineering culture plus Fortune-2000 delivery volume is what rivals can't assemble. · Open the full presentation →p. 48 — The AI maturity ladder and EPAM's claimed differentiation at Level 3, illustrated with the PostNL rollout. · Open the full presentation →p. 50 — AI/Run.Blueprints in depth — the adoption barriers it addresses, plus a client citing a 20% engineering-efficiency gain. · Open the full presentation →p. 51 — AI/Run.Tools in depth — integrating hyperscalers and industry tools, with a case showing 60% faster migration and $250K+ saved. · Open the full presentation →p. 52 — The talent evolution from narrow specialist to full-stack agentic engineer that turns AI tools into delivery systems. · Open the full presentation →p. 53 — Why demand won't dry up: an 'infinite backlog' of deferred work, with Edward Jones, Baker Hughes and Nelnet examples. · Open the full presentation →p. 81 — The 30-year timeline across internet, cloud and AI eras, marked with the dot-com crash, IPO, COVID and the Ukraine invasion. · Open the full presentation →p. 82 — The historical pattern: every productivity wave lowered build cost but underestimated the resulting demand and complexity. · Open the full presentation →p. 103 — Delivery model in 2021: 59% of delivery staff in Ukraine, Belarus and Russia before the invasion — the starting risk. · Open the full presentation →p. 104 — Delivery model today: that concentration cut to 21%, showing the post-invasion geographic de-risking. · Open the full presentation →p. 123 — Revenue, non-GAAP operating income and EPS, 2022–2026E — the return-to-growth picture with the drivers behind it. · Open the full presentation →p. 124 — The expanded delivery footprint — hubs across the Americas, Europe, India and Central Asia — and the capabilities offered. · Open the full presentation →p. 125 — Reiterated FY26 and Q1 2026 guidance: revenue, margin and EPS ranges in one table. · Open the full presentation →p. 126 — The long-term financial algorithm: growth, profitability, free cash flow and capital allocation as a flywheel. · Open the full presentation →p. 127 — The three-year growth target — from $5.5B toward double-digit growth by 2028 — and the drivers management is banking on. · Open the full presentation →p. 128 — The margin target: non-GAAP operating margin back to 16%+ by 2028, bridged by gross-margin and SG&A gains. · Open the full presentation →p. 129 — Free cash flow history and the 80–90% conversion target, pointing to ~$1.8B+ cumulative FCF through 2028. · Open the full presentation →p. 130 — Balance sheet: ~$1.3B cash against just $25M debt and a $675M untapped facility — the base for capital allocation. · Open the full presentation →p. 131 — The M&A framework — the strategic filters and financial criteria EPAM says it applies to acquisitions. · Open the full presentation →p. 138 — The CEO's closing 'why invest' case and the 2028 goals — the one slide that sums up the thesis. · Open the full presentation →