Full Report

EPAM Systems, Inc.'s management explains the business in its own materials. The slides below do the most of that work, pulled from the documents preserved in Sources. Each source link opens the complete presentation at that slide in a new tab.

Investor Presentation — May 2026 — May 2026

EPAM's current company-overview deck: the fastest tour of what it does, its scale and segments, the AI strategy, and FY26 guidance. · Open the full document →

Investor Day 2026 — Investor Day 2026

Management's fullest statement of strategy — the AI-native thesis, the engineering-moat argument, the delivery model, and 2028 targets. · Open the full document →

EPAM Systems, Inc.'s annual reports contain management's most considered account of the business. These are the sections, passages and visual pages worth opening in the originals preserved in Sources.

EPAM Systems, Inc. — FY2025 Annual Report (Form 10-K) — FY2025

Latest 10-K: the fullest picture of EPAM's AI pivot, Ukraine-centered delivery model, and 2025 margin compression. · Open the full document →

Item 1. Business — Overview and Services — p. 5 · Read the full section →

How EPAM frames itself: 30+ years of software engineering now sold as AI-native transformation and consulting.

EPAM's self-description — engineering heritage repositioned around AI-enabled transformation.

EPAM has used its software engineering expertise to become a leading global provider of digital engineering, cloud and artificial intelligence-enabled transformation services, and a leading business and experience consulting partner for global enterprises and ambitious start-ups. […] We leverage AI to deliver transformative solutions that accelerate our clients' digital innovation and enhance their competitive edge. Through platforms like EPAM AI/RUN™ and initiatives like DIALX Lab™, we integrate advanced AI technologies into tailored business strategies, driving significant industry impact and fostering continuous innovation.

p. 5 · Read in context →

Item 1. Business — Global Delivery Model — p. 9 · Read the full section →

The delivery footprint is EPAM's edge and its concentration risk in one place — India now largest, Ukraine still ~8,750.

Delivery headcount by country at Dec 31, 2025: India ~12,200, Ukraine ~8,750, Poland/Belarus/Mexico following.

In 2025, India remained our largest delivery location, measured by the number of delivery professionals, and as of December 31, 2025, we had approximately 12,200 delivery professionals in this location. We continued to focus on growing India as a key delivery location and added approximately 2,150 delivery professionals since December 31, 2024.

Ukraine continues to be a significant delivery location for us and we had approximately 8,750 delivery professionals there as of December 31, 2025, compared with 8,764 delivery professionals as of December 31, 2024. Since the Russian forces' attack on Ukraine and its people began on February 24, 2022, our teams remain highly focused on maintaining uninterrupted production. Our highest priority remains the safety and security of our employees and their families in Ukraine as well as in the broader region, and we have continued to support relocating our employees to lower risk locations, both inside Ukraine and to other countries where we operate. The vast majority of our Ukraine employees are in safe locations and we continuously monitor the situation.

p. 9 · Read in context →

Item 1. Business — Human Capital — p. 11 · Read the full section →

A headcount business — total employees (62,850) and delivery utilization (~76.8%) are the real operating levers.

Employees and delivery utilization rates, three years shown.

As of December 31, 2025, 2024 and 2023, we had approximately 62,850, 61,200, and 53,150 employees, respectively, of which approximately 56,600, 55,100, and 47,350 were delivery professionals, respectively. […] For the years ended December 31, 2025, 2024 and 2023, the utilization rates of our delivery professionals were approximately 76.8%, 76.7%, and 74.3%, respectively.

p. 11 · Read in context →

Item 1A. Risk Factors — Risks Related to Geopolitical Events — p. 15 · Read the full section →

~14,100 delivery and support staff sit in Ukraine and Belarus; the war remains a genuine, company-specific delivery threat.

Roughly 14,100 personnel based in Ukraine and Belarus as of year-end 2025.

We have significant operations and personnel in Ukraine and Belarus. Ongoing conflict and disruption in the region following Russia’s invasion of Ukraine in February 2022 has had and could continue to have a material adverse effect on our operations, personnel, business, clients, service delivery, and financial results. […] In particular, as of December 31, 2025, approximately 14,100 of our global delivery, administrative and support personnel were based in Ukraine and Belarus, both of which are involved in or affected by Russia’s invasion of Ukraine.

p. 15 · Read in context →

Item 1A. Risk Factors — Risks Related to Artificial Intelligence — p. 16 · Read the full section →

Management concedes AI-based tools may replace its services and have already weighed on the share price — the bear case in its own words.

EPAM states AI competition has 'negatively impacted the price of our stock.'

Increased competition, or the perception of increased competition, from new and non-traditional market participants like AI-based task-specific tools, has negatively impacted the price of our stock. If a significant number of our existing or future clients employ AI-driven tools as a replacement for our services or the software we build, our revenues, anticipated growth and prospects, our financial condition, and our results of operations could be materially adversely affected.

p. 16 · Read in context →

Item 7. MD&A — Business Update Regarding the War in Ukraine — p. 42 · Read the full section →

Management's current-state read: Ukraine production back to pre-war productivity, $100M humanitarian pledge nearly spent.

Ukraine delivery at pre-war productivity; $10.1M of the $100M humanitarian commitment remains.

Russia’s attack on Ukraine has had, and could continue to have a material adverse effect on our operations. As of December 31, 2025, Ukraine continues to be a significant delivery location with a large number of delivery professionals operating from safe locations at levels of productivity consistent with those achieved prior to the attack. We have maintained our $100 million humanitarian aid commitment to our people in Ukraine, and as of December 31, 2025, we have $10.1 million remaining to be expensed under this humanitarian commitment.

p. 42 · Read in context →

Item 7. MD&A — Results of Operations — p. 44 · Read the full section →

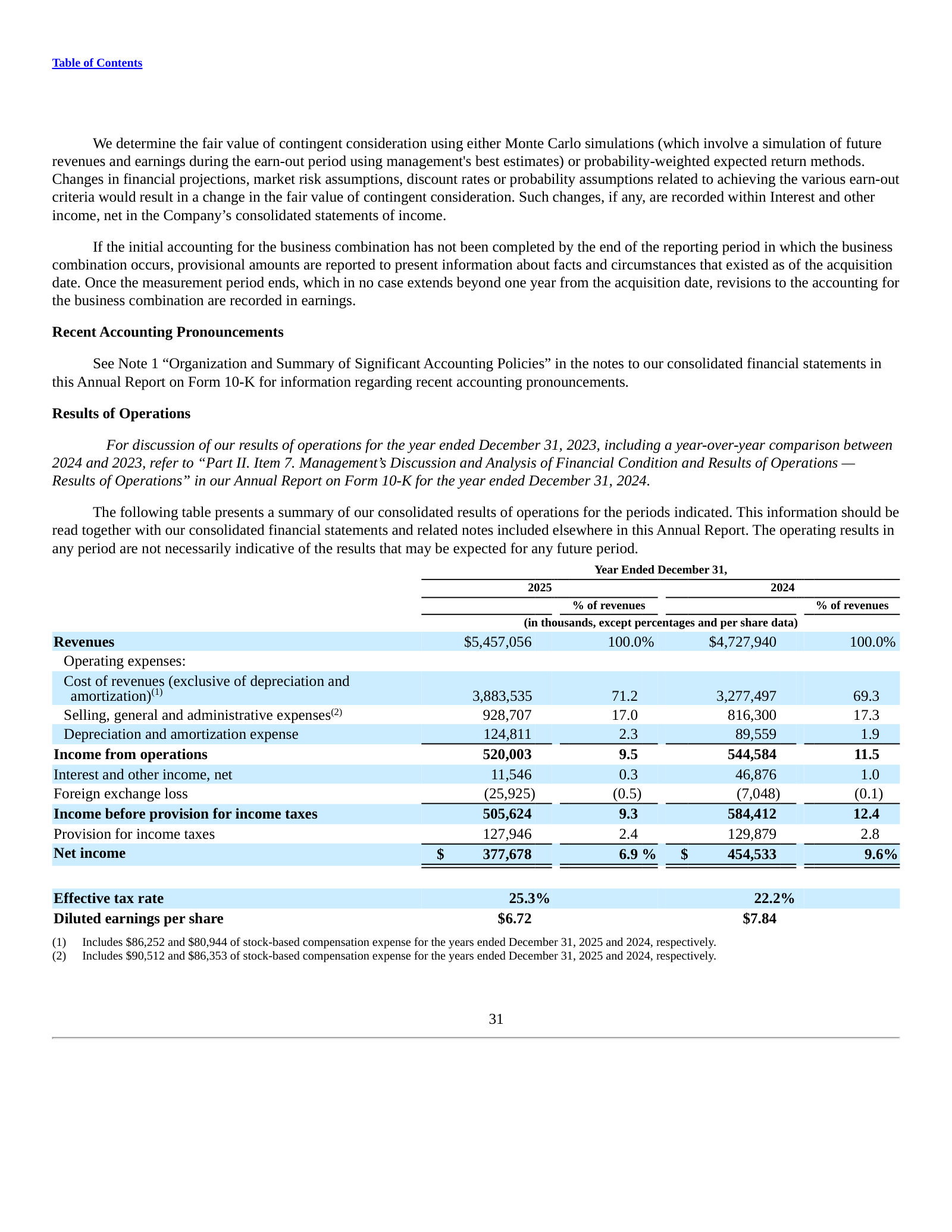

The margin story: revenue up 15.4% to $5.46B, yet net income and diluted EPS fell as costs outran growth.

Revenue bridge for 2025: acquisitions added 9.2 points and FX 1.3 points of the 15.4% growth.

During the year ended December 31, 2025, our total revenues increased 15.4% from the previous year to $5.457 billion. Revenues from the first twelve months following each acquisition that was made in the fourth quarter of 2024, increased our revenues by 9.2% and fluctuations in foreign currency increased our revenues by 1.3% during the year ended December 31, 2025 as compared to the previous year.

p. 45 · Read in context →

Item 7. MD&A — Results by Business Segment — p. 49 · Read the full section →

Two segments (Americas, Europe) after the 2025 rename from North America; both saw operating margins compress.

2025 rename of the North America segment to Americas, reflecting Latin America growth (no restatement).

Starting in 2025, we renamed our North America segment to Americas. The new name reflects the evolving geographic footprint and growth of operations within the segment, particularly in Latin America. This constitutes a naming change only and no changes were made to amounts reported.

p. 49 · Read in context →

EPAM Systems, Inc. — FY2022 Annual Report (Form 10-K) — FY2022

The war's first full year — features a Russia segment and an evacuation narrative both absent from later reports. · Open the full document →

Item 7. MD&A — Business Update Regarding the War in Ukraine — p. 32 · Read the full section →

The crisis-year snapshot: phased exit from Russia and employee relocation, versus FY2025's stabilization.

April 2022 phased exit from Russia and September 2022 agreement to sell remaining Russian holdings.

Prior to the attack in February 2022, Belarus and Russia were our second and third largest delivery locations by the number of delivery professionals, respectively. On April 7, 2022, the Company announced the beginning of a phased exit of our operations in Russia in close collaboration with our employees, contractors, and customers. We have discontinued services to certain customers located in Russia and on September 7, 2022, we executed an agreement to sell substantially all of our remaining holdings in Russia to a third party.

p. 32 · Read in context →

Item 7. MD&A — Results by Business Segment: Russia Segment — p. 43 · Read the full section →

EPAM still reported a Russia segment in 2022 — since eliminated entirely — swinging to an operating loss.

The since-eliminated Russia segment: a $13.5M operating loss in 2022 versus $32.5M profit in 2021.

During 2022, revenues from our Russia segment decreased $92.3 million relative to 2021 and represent 1.5% of total segment revenues during 2022 compared with 4.4% in 2021. The decrease in revenues was primarily attributable to decreased operations in Russia as we proceed with the phased exit from Russia while discontinuing services to customers there. Operating loss of our Russia segment was $13.5 million in 2022 compared to operating profit of $32.5 million in 2021. This decrease was largely driven by discontinuance of services to certain customers in Russia which led to reduced revenues, increased bad debt expense, and expenses incurred for services provided to those customers for which revenue was not recognized as collectability was not considered probable after announcing the discontinuance of services to customers in Russia.

p. 43 · Read in context →

More annual reports

EPAM Systems, Inc. — FY2024 Annual Report (Form 10-K) — FY2024 · 113 pages · Prior-year 10-K covering the NEORIS and First Derivative acquisitions and EPAM's return to growth. · Open →

EPAM Systems, Inc. — FY2023 Annual Report (Form 10-K) — FY2023 · 114 pages · The demand-slowdown year — revenue growth stalled after the post-invasion rebalancing. · Open →

EPAM Systems, Inc. — FY2021 Annual Report (Form 10-K) — FY2021 · 116 pages · Pre-invasion baseline: Belarus and Russia still ranked among the largest delivery locations. · Open →

Competitors describe EPAM Systems, Inc.'s market in their own filings and calls. These verified passages and visual pages show where their strategies meet, using source documents preserved in Sources.

Globant (GLOB)

The closest listed analog to EPAM: a next-generation digital-engineering pure-play that names EPAM directly and competes for the same AI-transformation and platform-build budgets.

Globant sizes the shared opportunity using Gartner's projection for the cloud IT-services market — the pool EPAM competes for.

The cloud IT services market is anticipated to reach $439 billion by 2028, according to Gartner. As organizations increasingly adopt complex hybrid environments, the need for external public cloud IT transformation services is set to rise dramatically, from 60% in 2023 to approximately 80% by 2028. This shift underscores the critical importance of cloud consulting services, driven by the need for technology assessment and readiness.

p. 31 · Read in context →

Globant's 20-F names EPAM Systems among the technology-services providers it competes against.

We face competition from various technology services providers such as Accenture, Atos, Capgemini, Cognizant Technology Solutions, Deloitte Digital, DXC Technology, Endava, EPAM Systems, Inc., Genpact, GlobalLogic, Grid Dynamics, HCL Technologies, Infosys, Tata Consultancy Services, and Wipro, among others.

p. 44 · Read in context →

Globant's stated AI-delivery model — an 'AI Pods' subscription platform routing across many LLMs — the offering it is pitching against rivals like EPAM.

Martín Migoya, CEO: The delivery engine powering both is Globant Enterprise AI, our proprietary platform with four interconnected hubs. The Enterprise Hub connecting securely to all corporate systems, the AI Hub routing intelligently across 140+ LLMs while preserving full data sovereignty, the Agent Hub where we build and publish industry-specific agents encoding twenty years of domain expertise, and the AI Pods Hub where clients subscribe and scale.

p. 9 · Read in context →

Endava (DAVA)

A next-generation digital-engineering competitor that places EPAM at the head of its named peer set; overlaps heavily with EPAM in build-side software services for enterprises.

Endava's annual report names EPAM Systems first among the 'next-generation' digital IT-service providers it counts as primary competitors.

Our primary competitors include next-generation digital IT service providers, such as Globant S.A., EPAM Systems, Grid Dynamics and Thoughtworks, digital agencies and consulting companies, such as Ideo, McKinsey & Company and Publicis Sapient, global consulting and traditional IT services companies, such as Accenture PLC, Capgemini SE, Cognizant Technology Solutions Corporation and Tata Consultancy Services Limited, and in-house development by our clients of their technology and IT capabilities.

p. 23 · Read in context →

Endava's CEO argues AI-driven demand — legacy modernization and complex AI implementation — will outweigh productivity headwinds over the next 5-10 years.

John Cotterell, CEO: So we actually see a lot of opportunity as enterprises start to address all of these complex issues around the implementation of AI and a growth in demand because there are many things that enterprises have not been able to do in the last 20 or 30 years like address their legacy systems. The AI actually enables a cost-effective route to addressing as well as then delivering business benefits that weren't possible without AI. So actually, we see the uplift in the market opportunity certainly for the next 5 to 10 years, outweighing as enterprise started to adopt at scale, outweighing the productivity headwinds that people are concerned about.

p. 18 · Read in context →

Endava's CEO on the market moving from AI experimentation to operationalization and outcome-based engagements — the same demand shift EPAM is chasing.

John Cotterell, CEO: Clients are increasingly looking for partners who can help them operationalize AI securely, integrate it into complex enterprise environments and connect investment directly to measurable business outcomes. […] Robust enterprise-grade IT services are essential for enabling AI leaders to scale their products safely and quickly.

p. 7 · Read in context →

Grid Dynamics (GDYN)

A digital-engineering competitor that lists EPAM as a primary competitor and benchmarks itself against EPAM in its stock-performance peer group; competes directly for AI-native build work.

Grid Dynamics' 10-K lists EPAM Systems among its primary competitors.

Our primary competitors include global consulting and traditional IT service providers such as Accenture plc, EPAM Systems, Inc., Capgemini SE, Cognizant Technology Solutions Corporation, Infosys Technologies, Tata Consultancy Services Limited

p. 33 · Read in context →

Grid Dynamics' CEO argues AI-native development and legacy modernization are expanding the addressable market for engineering services.

Leonard Livschitz, CEO: AI is meaningfully expanding Grid Dynamics' addressable market. For example, AI-native SDLC and agentic coding fundamentally changed the economics of delivering services. With delivery time and cost compressing, we can take on larger client initiatives that were previously out of our reach. Also, AI is unlocking a wave of legacy modernization that was not previously economically viable.

p. 1 · Read in context →

Grid Dynamics' CEO positions nimble AI-focused engineering against incumbent system integrators, arguing headcount leverage is no longer a moat — a framing that cuts at scaled players like EPAM.

Leonard Livschitz, CEO: Large enterprises are increasingly seeking highly capable, nimble partners like Grid Dynamics, who can move quickly and deliver meaningful AI outcomes rather than relying on incumbent global system integrators burdened by legacy delivery models. In many ways, headcount leverage is no longer a competitive moat and differentiation comes from domain knowledge, AI capabilities and ability to rapidly scale relevant expertise.

p. 1 · Read in context →

Cognizant (CTSH)

A far larger IT-services firm that names EPAM as a direct competitor; overlaps with EPAM across digital engineering, modernization, and AI-led transformation for enterprise clients.

Cognizant's 10-K names EPAM Systems among its direct competitors.

Our direct competitors include, among others, Accenture, Atos, Capgemini, CGI, Deloitte Digital, DXC Technology, EPAM Systems, Genpact, HCL Technologies, IBM Consulting, Infosys Technologies, Tata Consultancy Services and Wipro.

p. 18 · Read in context →

Cognizant's CEO frames the AI opportunity as reaching trillions in 'labor spend' beyond the software market — his case for an expanding services TAM.

Ravi Kumar, CEO: While the global software market is in the hundreds of billions of dollars, the surrounding labor spend represents many trillions more. Classical software has barely penetrated that space. We believe AI's winners will be those who diffuse into this labor spend, reshape how work gets done.

p. 3 · Read in context →

Cognizant's CEO describes an 'AI builder stack' spanning compute, cloud, models and services — its strategy for capturing agentic-AI demand.

Ravi Kumar, CEO: We believe the invention and reimagination of businesses will be driven by value at the intersection of AI-led agentic capital and classical software. To capture this demand, our AI builder stack acts as the connective tissue that addresses four layers of the ecosystem: AI compute, cloud, model access, and human capital services.

p. 2 · Read in context →

Accenture (ACN)

The largest and broadest competitor in EPAM's market; its scale, GenAI investment and bookings set the pace for AI-led services that EPAM must contend with.

Accenture points to its stated $3 billion multi-year generative-AI investment as a bid for early leadership in AI-related client spend.

We also use our investment capacity to drive early leadership in areas of growth. For example, our early and decisive decision in fiscal 2023 to invest significantly to become a leader in generative AI with a $3 billion multi-year investment has positioned us to capture this new area of spend for our clients.

p. 6 · Read in context →

Accenture's stated quarterly Advanced-AI bookings and revenue — a gauge of the scaled AI demand EPAM competes against.

Angie Park, CFO: Our Advanced AI bookings this quarter were $2.2 billion, nearly doubling from Q1 last year and also up from Q4. Revenue reached another milestone this quarter at approximately $1.1 billion.

p. 8 · Read in context →

Infosys (INFY)

A large global IT-services incumbent competing with EPAM on enterprise AI, modernization and large-deal transformation programs, with a very different offshore-led cost model.

Infosys sizes the AI-services opportunity it is targeting to 2030 — its framing of the enterprise-AI market EPAM also pursues.

Salil Parekh, CEO: the 6 areas with an external analysis, we understand that the opportunity is between $300 bn and $400 bn in the year getting to 2030, so over that time frame at that time in 2030. […] today, we have a clear view that the opportunity is massive and large and that will become the driving force of what we will grow and drive through in the next coming years.

p. 11 · Read in context →

Infosys reports its full-year large-deal signings and points to a broad AI-services market — the scaled deal pipeline EPAM competes against.

Salil Parekh, CEO: Large deals were strong. For the full year, we had $14.9 bn of large deals. This is a growth of 28% over the prior year. And for Q4, we were at $3.2 bn, a strong showing for the quarter. […] We see a large addressable market for AI services across six areas; AI strategy and engineering, data, process, legacy modernization, physical AI and trust.

p. 26 · Read in context →

More peer documents

Grid Dynamics FY2024 10-K — competitor list and stock peer group — 158 pages · Names EPAM as a competitor (p29) and benchmarks its stock-performance chart explicitly against EPAM, Accenture, Cognizant, Endava and Globant (p70). · Open →

Endava FY2024 20-F — prior-year competitor and comp peer group — 214 pages · Earlier framing naming EPAM as a primary competitor plus a compensation peer group listing EPAM, Globant and Grid Dynamics (around p95). · Open →

Cognizant FY2024 10-K — competitor list — 148 pages · Prior-year 10-K also names EPAM Systems among direct competitors (around p17), showing the framing is persistent, not a one-off. · Open →

Accenture FY2024 10-K — competition and positioning — 106 pages · Prior-year competitive positioning and GenAI strategy for cross-checking how the largest competitor's framing evolved into FY2025. · Open →

Globant FY2025 20-F — updated competitor list and demand drivers — 221 pages · Refreshed competitor list still naming EPAM (around p38) plus updated market-driver commentary for cross-checking the FY2024 TAM figures. · Open →

Infosys FY2026 annual report — Topaz / enterprise-AI strategy — 384 pages · Lays out Infosys's Topaz AI platform and 'enterprise AI partner of choice' positioning at length — the strategic backdrop to its market-size claims. · Open →

Cognizant Q1 FY2026 earnings call — 11 pages · Fuller management commentary on AI-led demand, agentic-AI delivery and pricing beyond the two quarters featured above. · Open →

Globant Q3 FY2025 earnings call — 32 pages · Earlier detail on the Globant Enterprise AI platform as a 'multipurpose hub' and AI-Pods traction, predating the Q4 model featured above. · Open →

EPAM Systems: the business and its drawdown

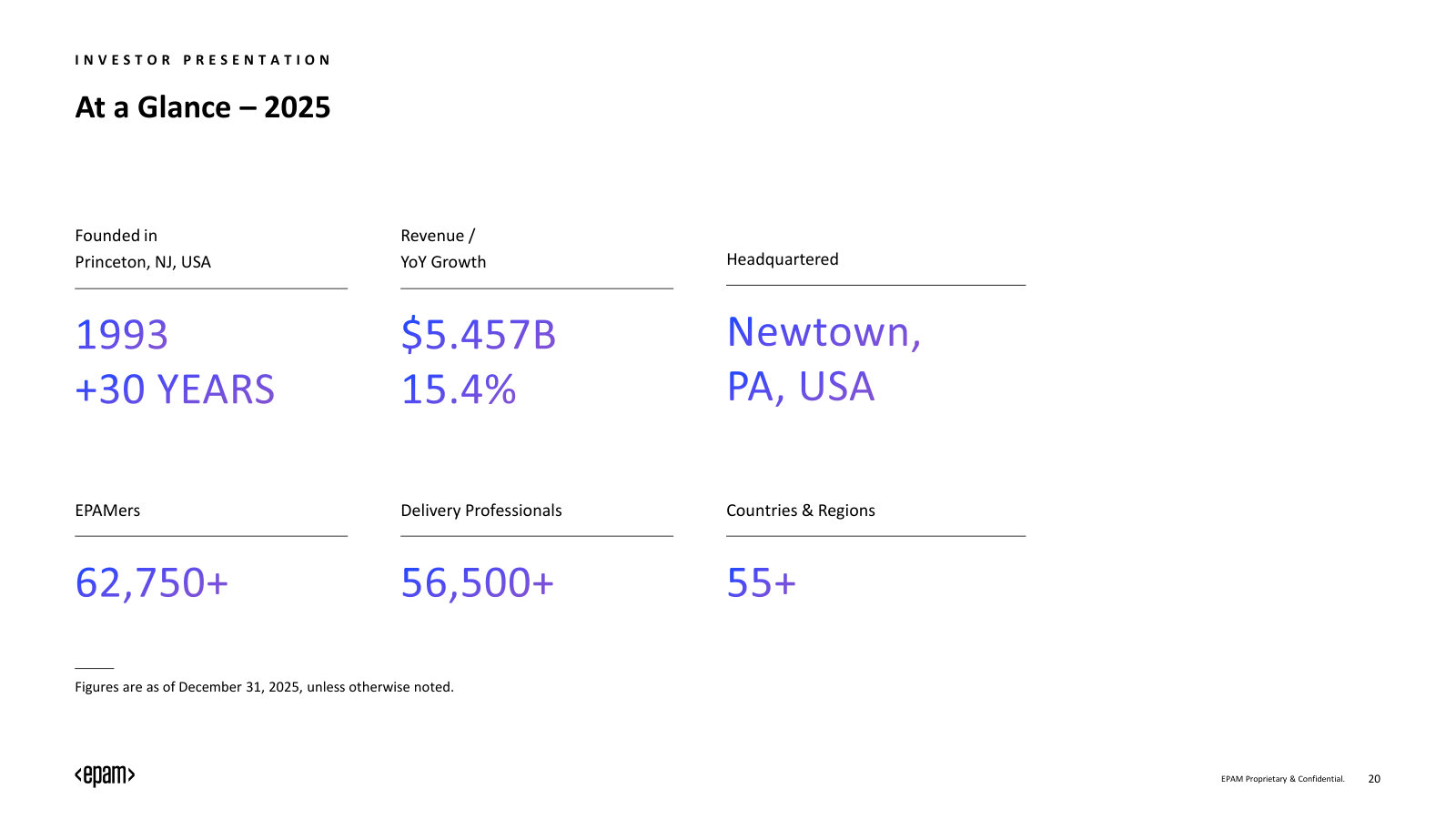

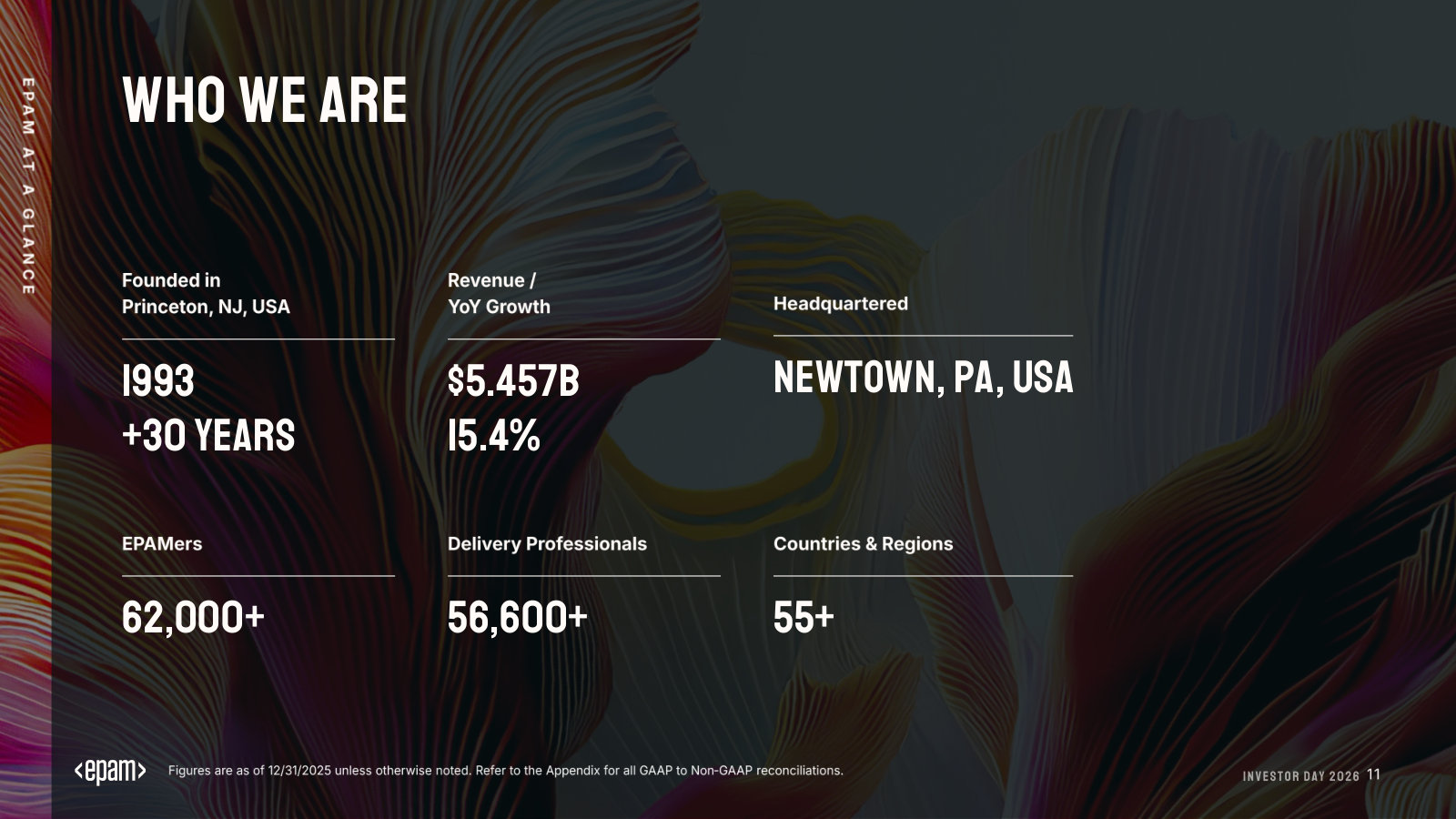

EPAM Systems builds software for large enterprises — digital engineering, cloud and AI work delivered by roughly 56,600 engineers, mostly in lower-cost geographies [1]. The business still grows and still converts profit to cash. The stock does not reflect that: at $86, EPAM trades about 87% below its late-2021 peak, near $13 of trailing earnings and under 8x free cash flow, with net cash worth a quarter of its market value. This chapter establishes what the company is, how it earns, and what the collapse has left on the table.

What EPAM does

EPAM describes itself as a global provider of digital engineering, cloud, and AI-enabled transformation services, pairing consulting with more than three decades of software-delivery execution [2]. In plain terms, when a bank, retailer, or drug company needs custom software built, modernized, or run, EPAM supplies the multidisciplinary engineering teams to do it, billing largely for the time of those engineers.

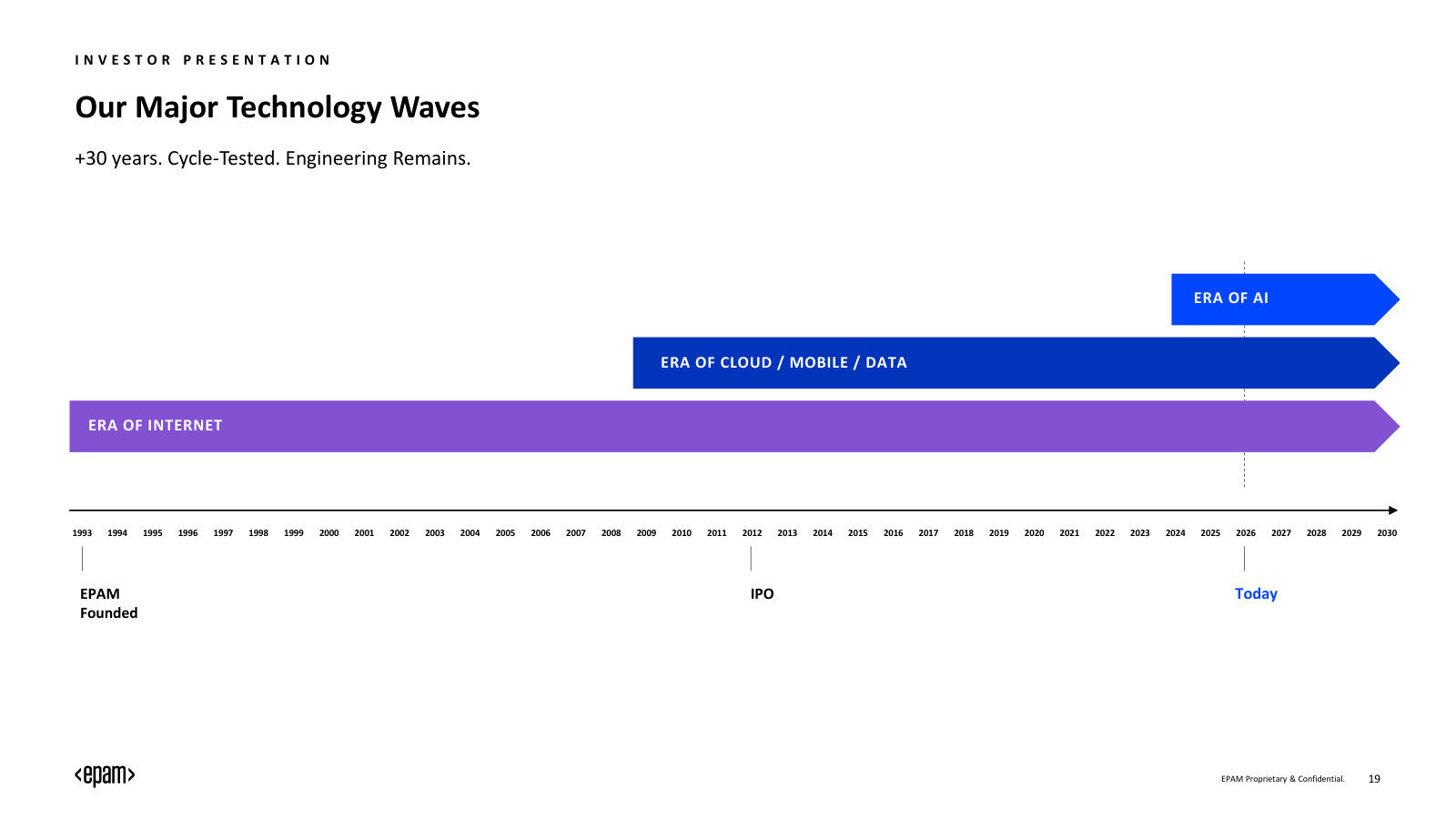

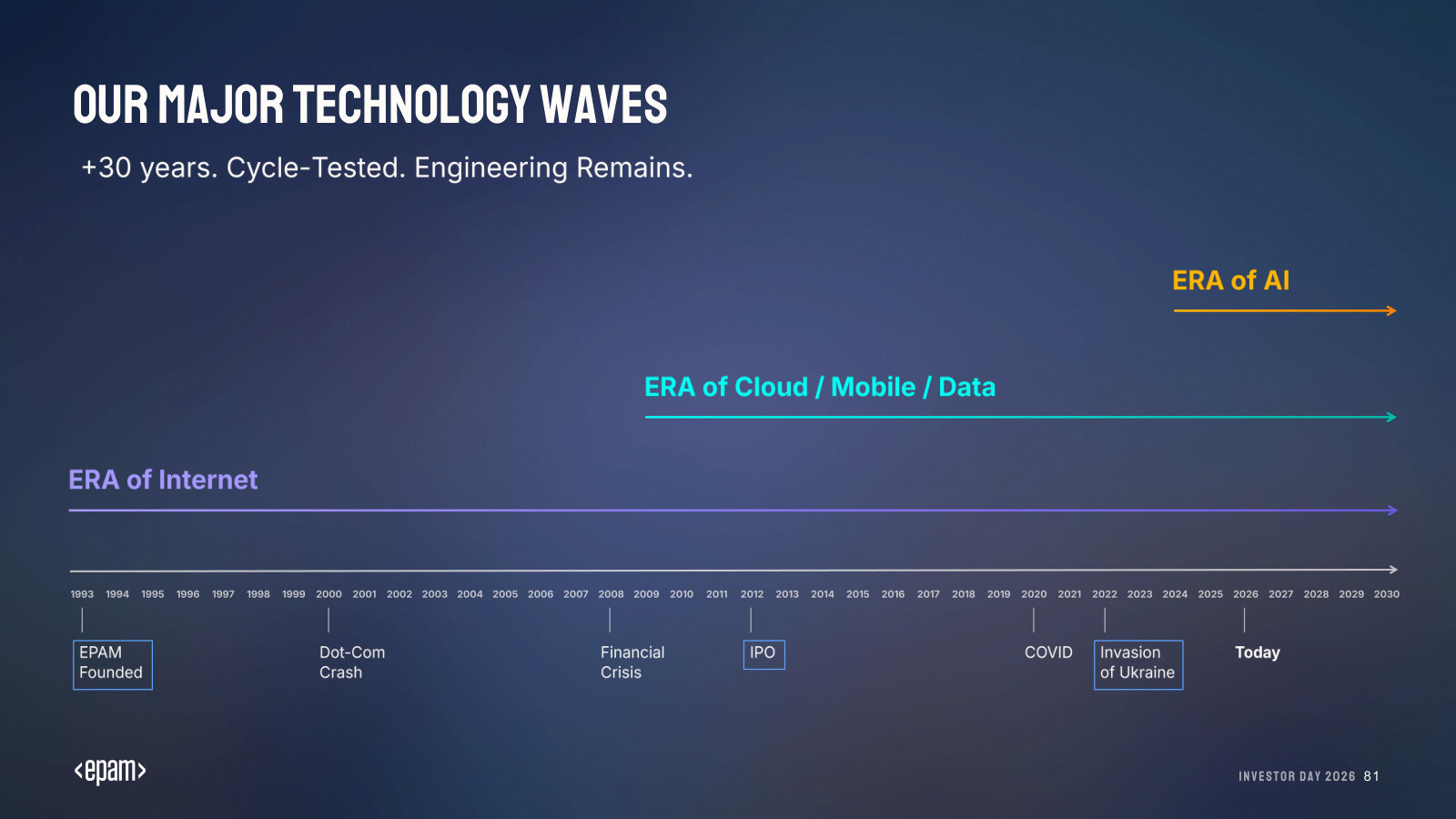

The predecessor business was founded in 1993 and incorporated in Delaware in 2002; it is headquartered in Newtown, Pennsylvania [3]. Founder Arkadiy Dobkin ran it as CEO from the start until September 1, 2025, when Balazs Fejes became President and CEO and Dobkin moved to Executive Chairman [4]. Dobkin remains the largest individual holder, with about 1.5 million shares, close to 2.9% of the company — meaningful founder alignment, though far from control.

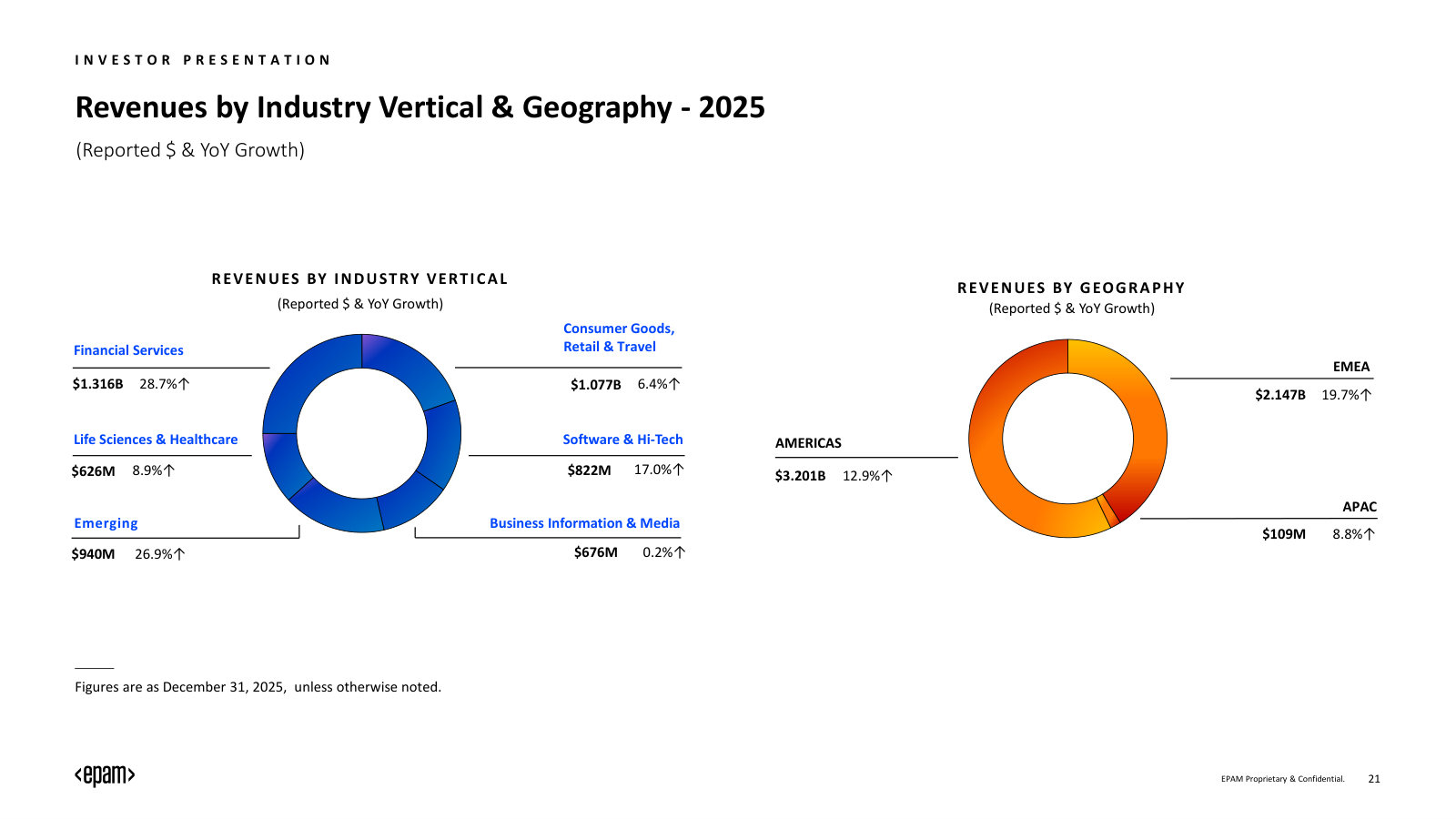

Its clients are concentrated in five verticals — financial services; software and hi-tech; consumer goods, retail and travel; life sciences and healthcare; and business information and media — and they tend to stay: 64.4% of 2025 revenue came from clients of five years or more, and no single client is more than a low-double-digit share of the total, with the top five at 13.7% [1]. It competes with the large IT-services names — Accenture, Cognizant, Infosys, TCS, Capgemini — and with closer digital-engineering peers such as Globant, Endava, and Grid Dynamics [5].

How the money is made

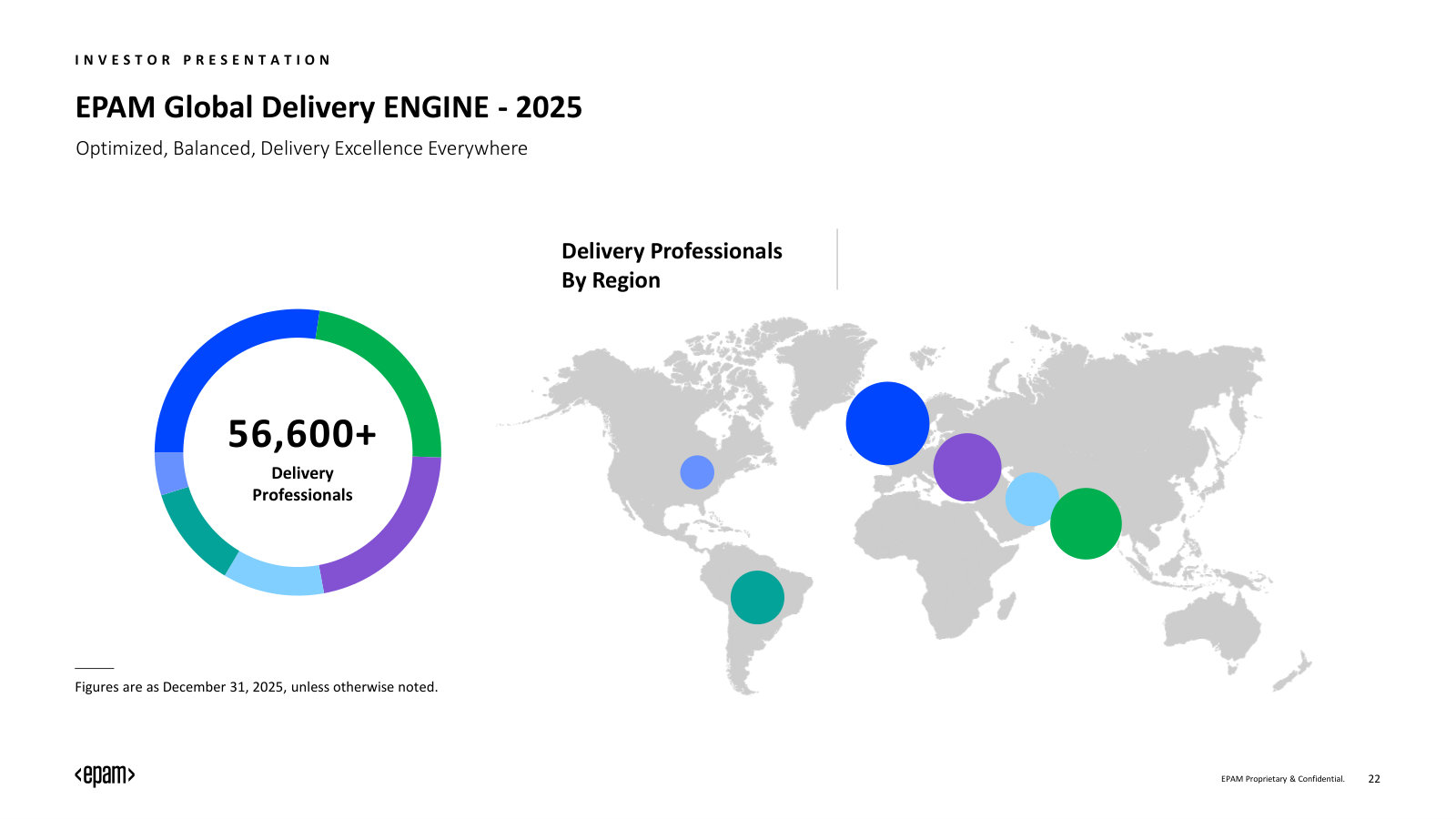

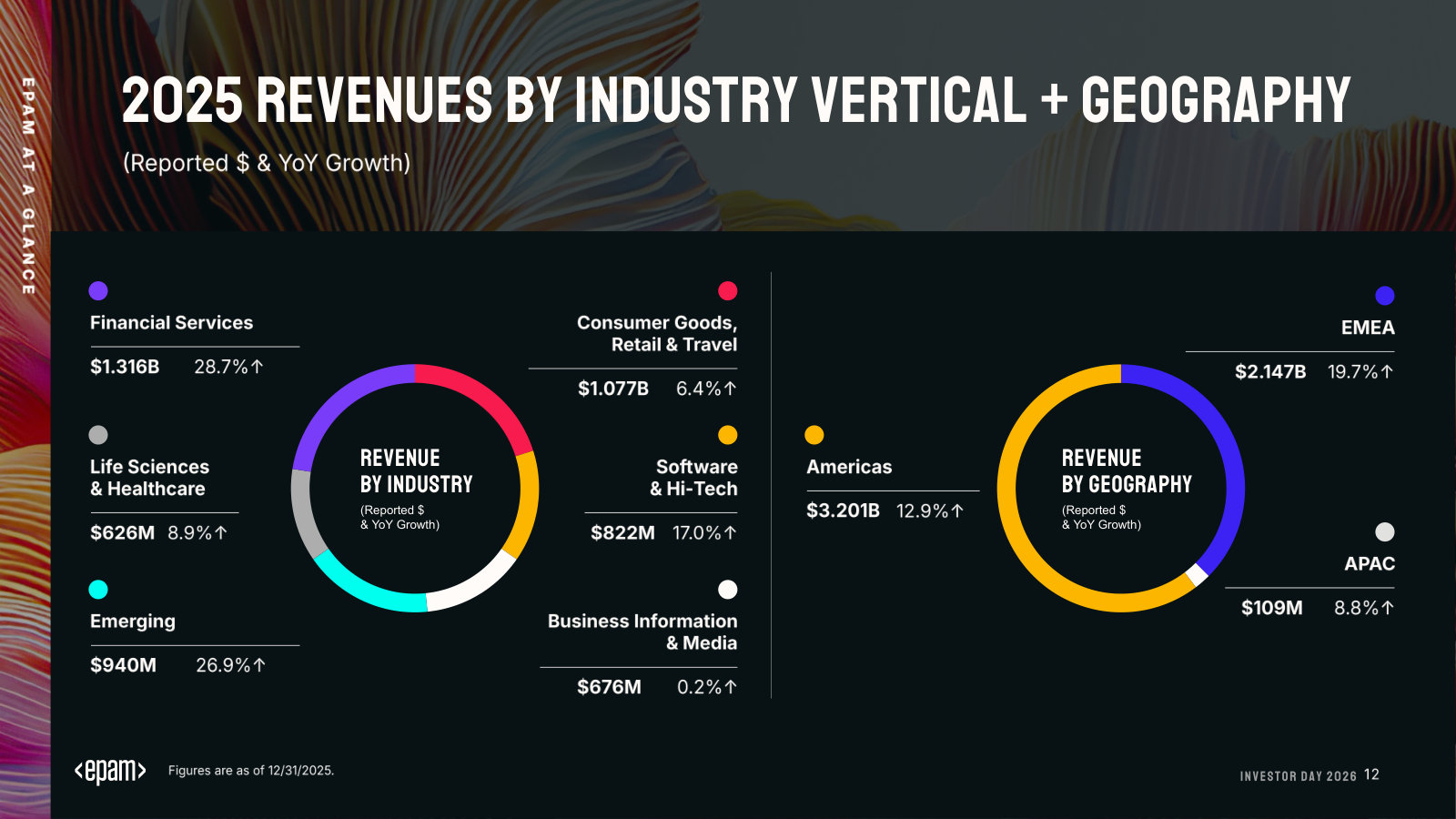

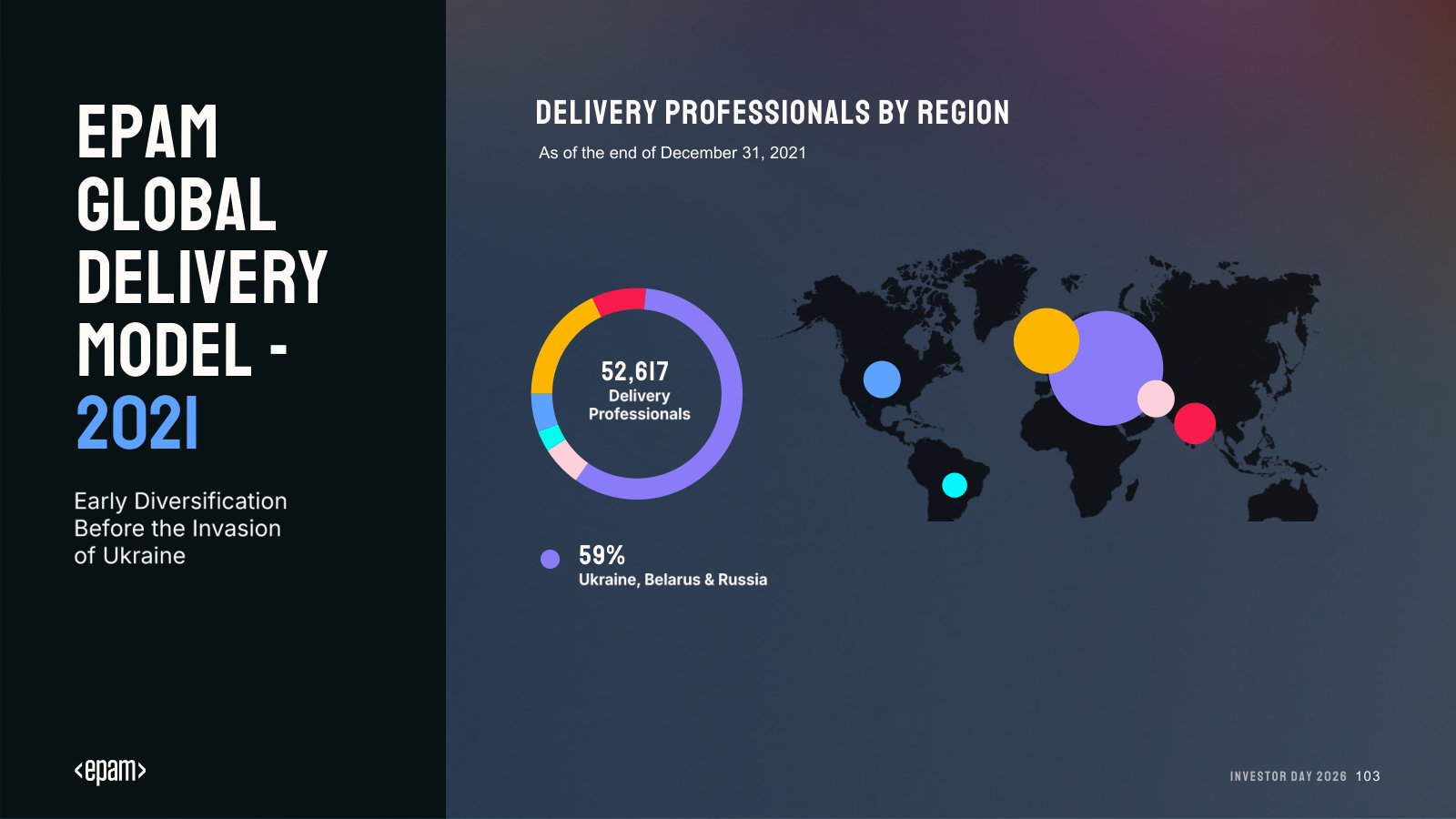

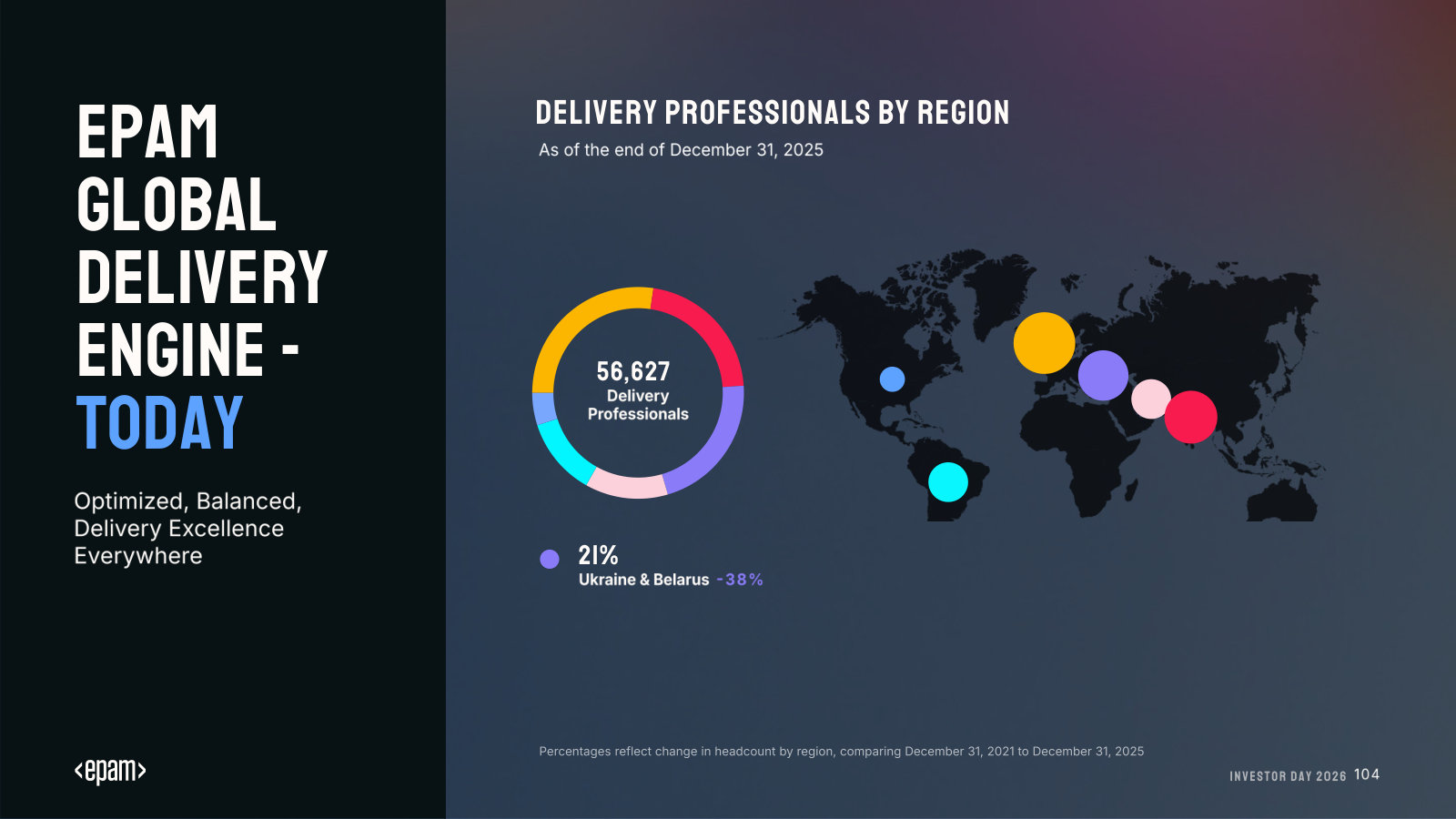

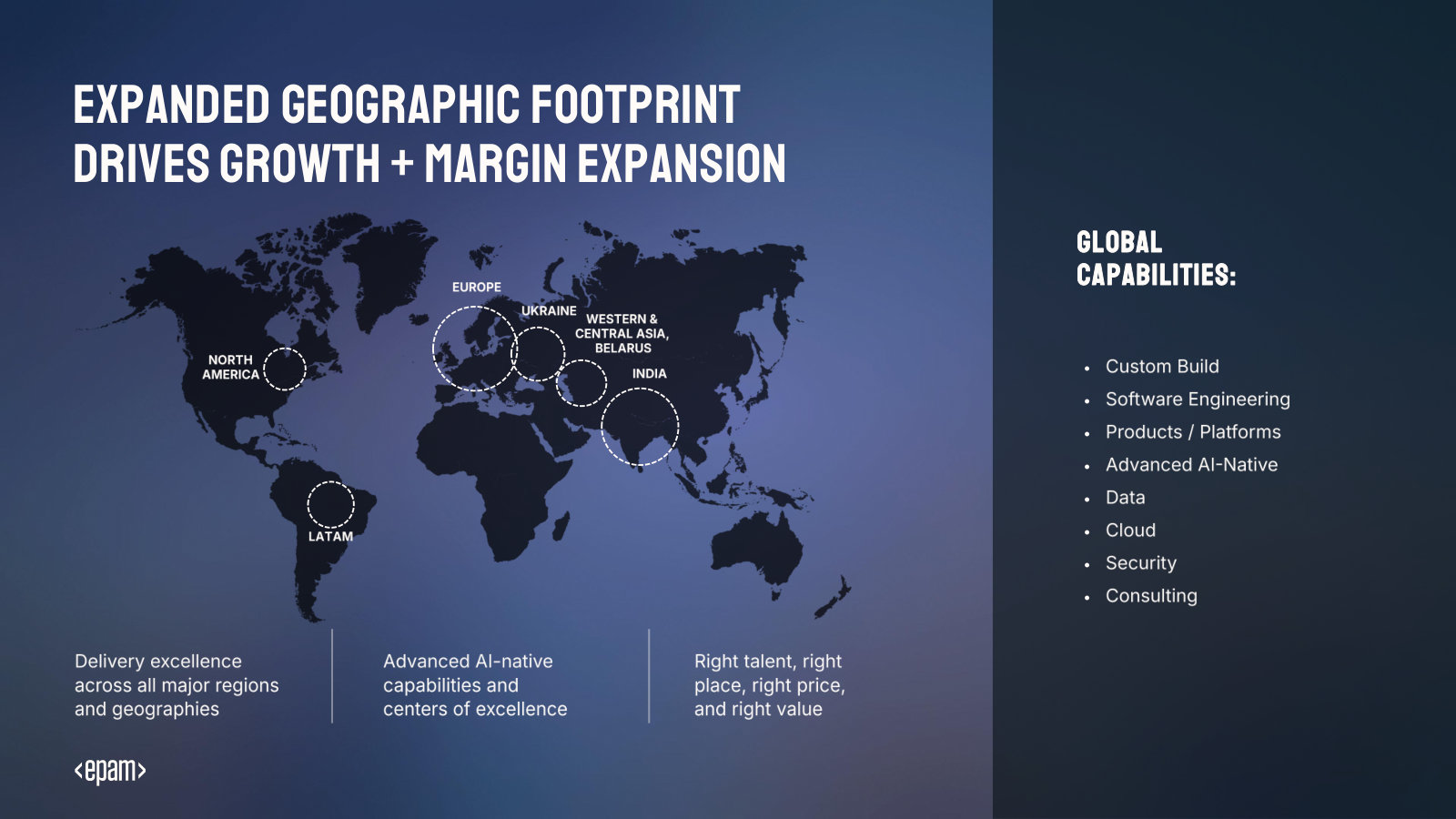

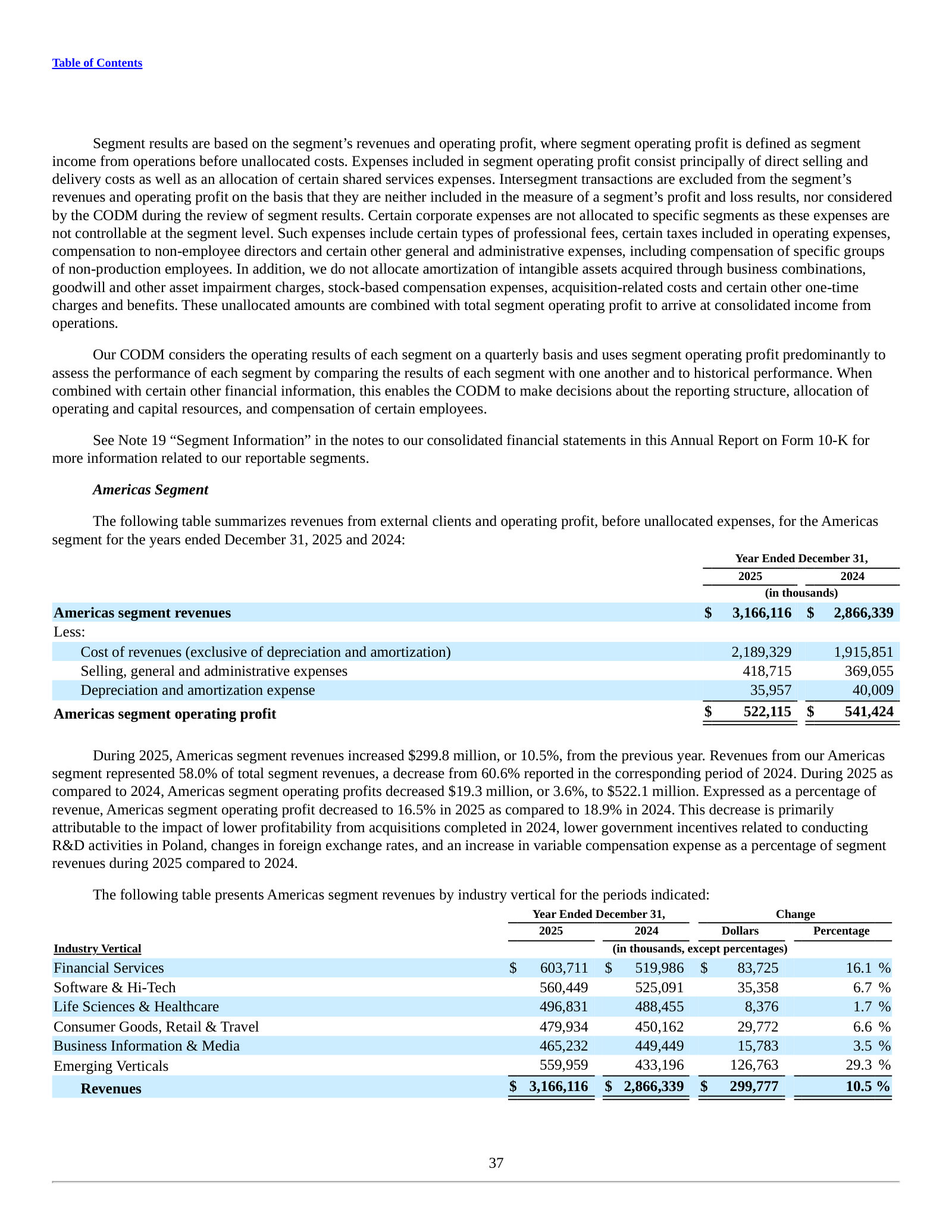

The revenue sits in developed markets while the cost of delivering it sits in emerging ones — the labor-arbitrage core of the model. In 2025, the Americas produced 58.7% of revenue and EMEA most of the rest [6], but the engineers are largely elsewhere: India is now the largest delivery location at about 12,200 professionals, and Ukraine remains significant at roughly 8,750 despite the war [1]. The spread between what clients pay in New York or London and what engineers cost in Hyderabad or Kraków is where the margin lives.

Source: FY2025 Annual Report (Form 10-K), MD&A revenues by location [6].

That structure carries two exposures worth stating up front, because both are central to why the stock fell. The first is geographic: after Russia's February 2022 invasion, EPAM had to relocate large parts of a delivery base then concentrated in Ukraine, Belarus, and Russia, and it has since rebuilt around India and elsewhere [7]. The second is structural, and EPAM names it directly: increased adoption of AI-based software tools "may reduce demand for our services," because clients can use large-language-model and agentic tools to build and maintain software themselves rather than buy engineering hours [7]. A business that sells engineering time faces an obvious question when the tool it sells begins to write code.

The drawdown

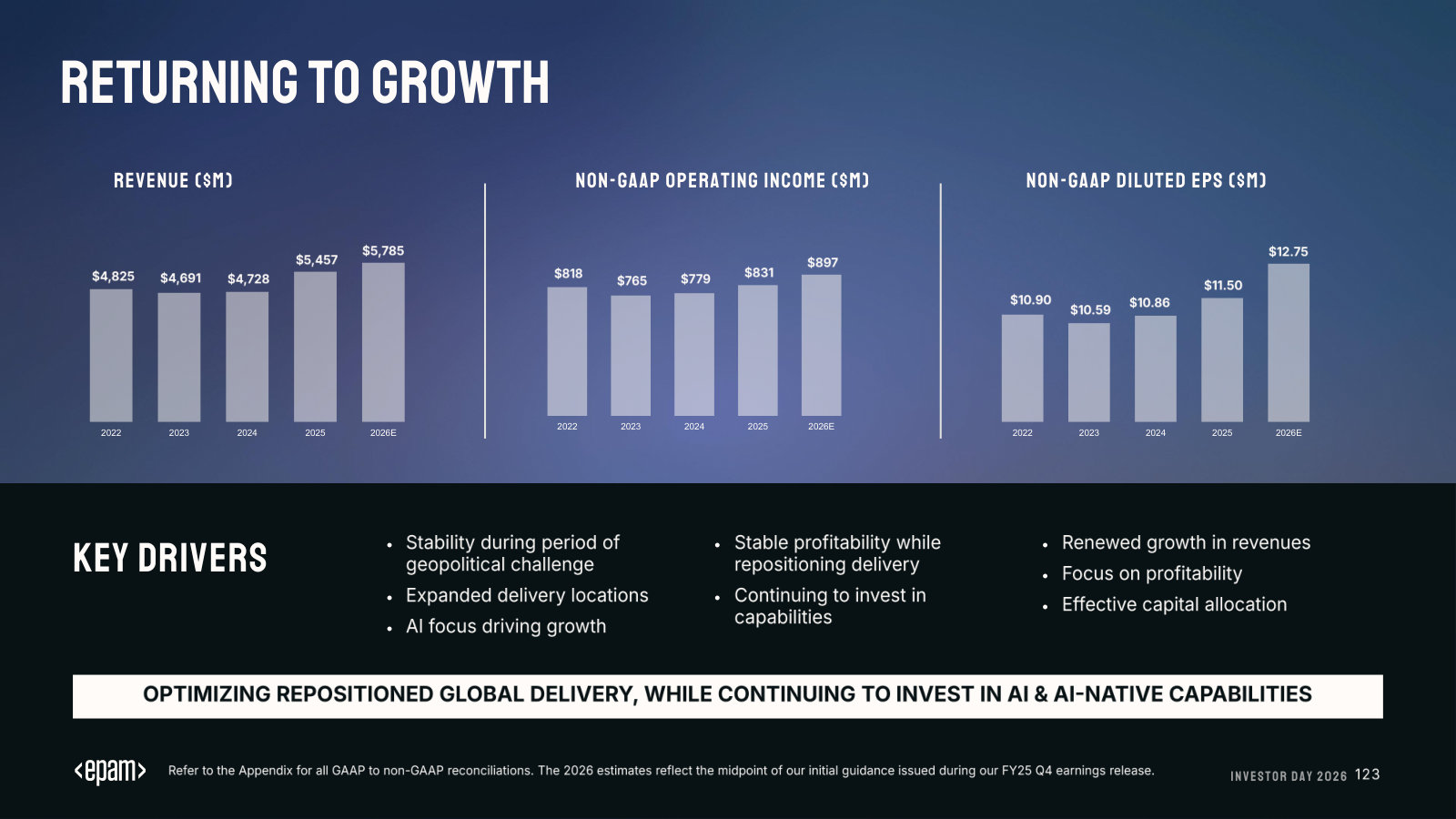

EPAM was one of the market's fastest-growing IT names on the way up: revenue compounded from about $1.2 billion in 2016 to $3.8 billion in 2021, and the shares closed 2021 near $668, up more than thirtyfold from the 2016 year-end. The re-rating then reversed in stages — the 2022 delivery shock, a demand slowdown through 2023 and the first half of 2024, and, most recently, an accelerating AI-disruption fear that took the stock from roughly $205 at the end of 2025 to $86 by mid-2026.

Source: NYSE daily price history (2026 point is the July 13, 2026 close of $86.38); company filings, as reported.

The distinction that matters for a value investor is whether the earnings collapsed with the price. They did not, at least not to the same degree.

The financials behind the fall

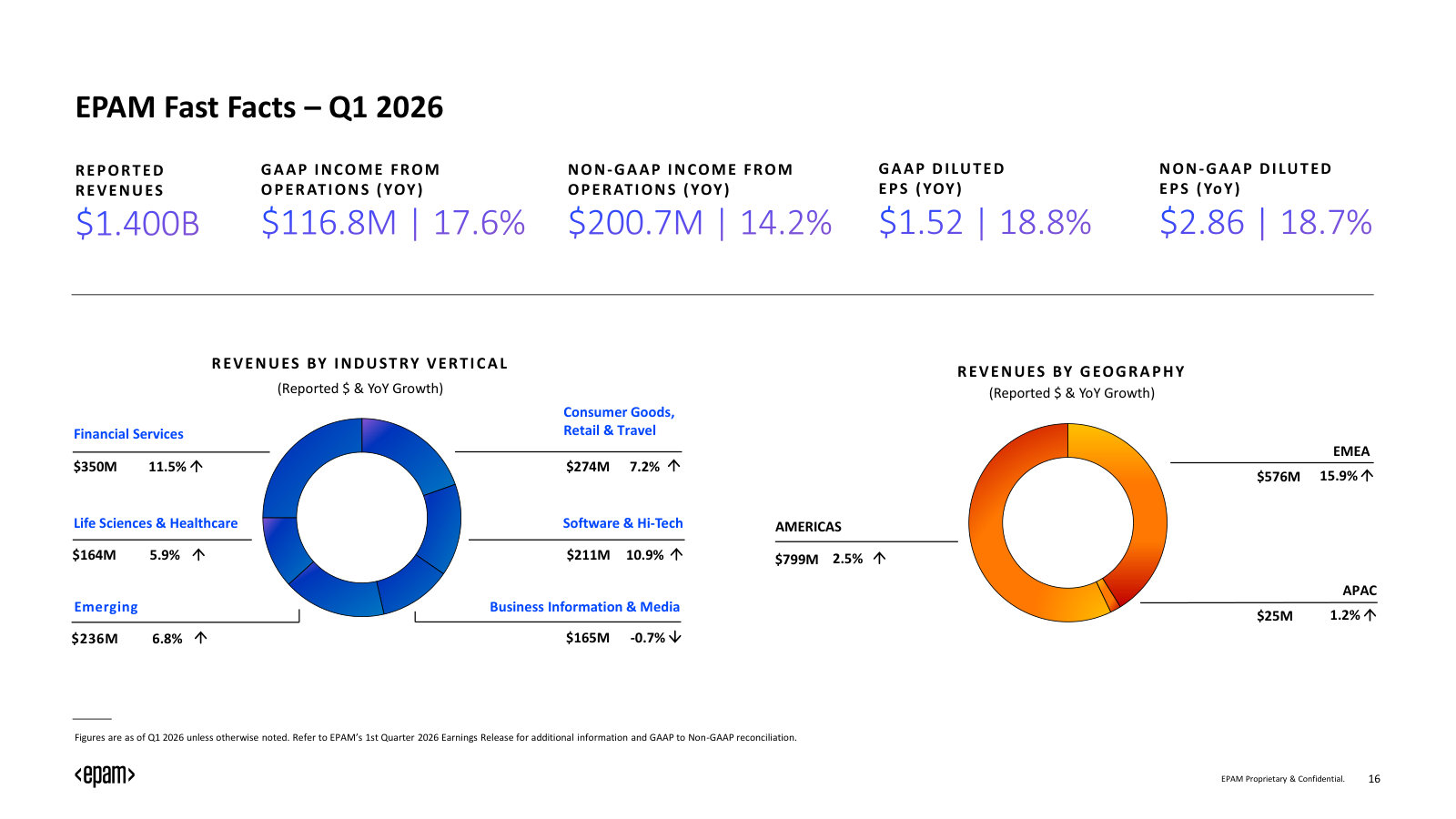

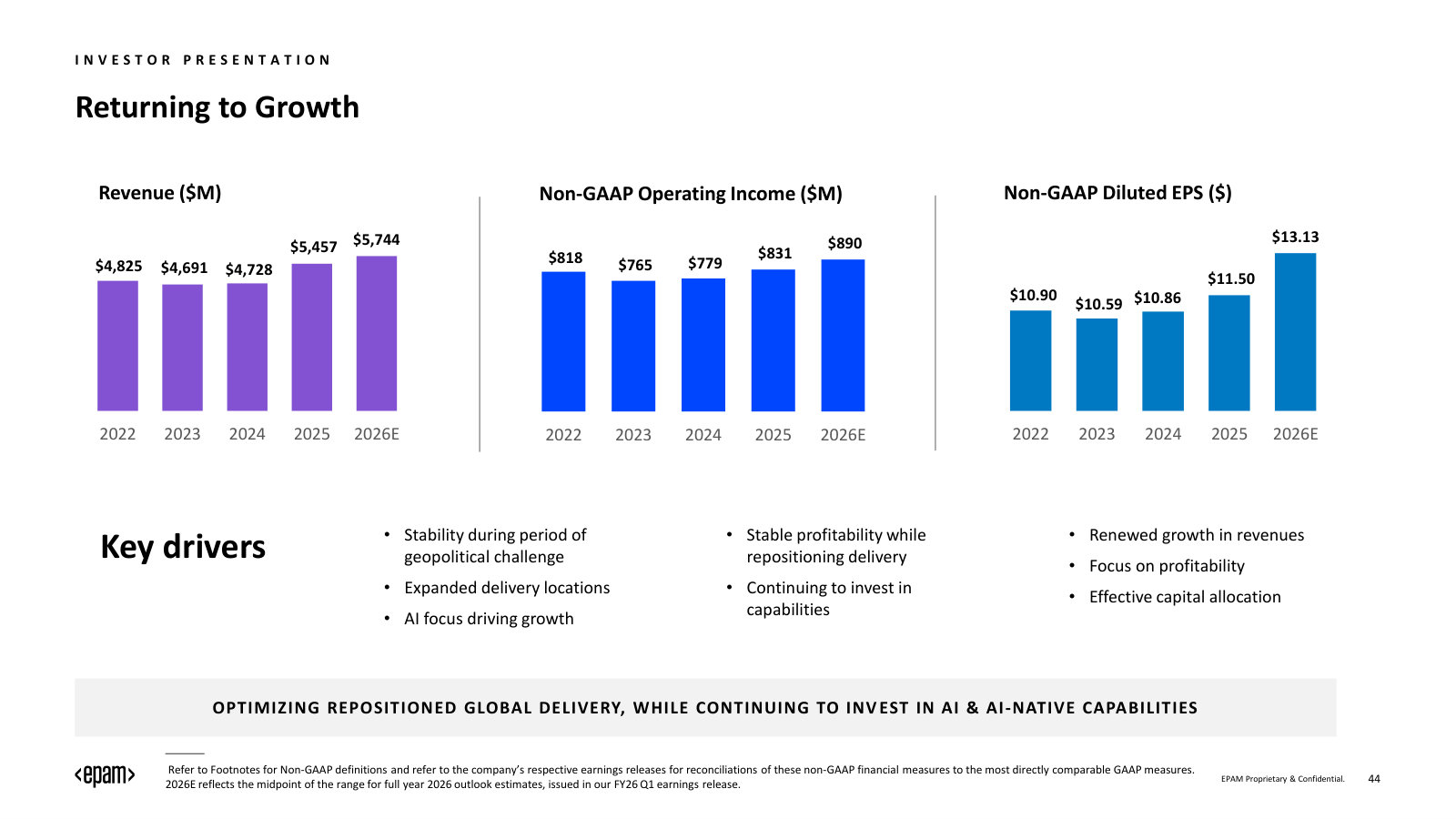

Revenue did stall. After growing 28% in 2022, it fell in 2023 and was roughly flat in 2024 as clients deferred spending, before reaccelerating to $5.46 billion in 2025 — up about 15%, helped by acquisitions [8]. Management attributes the 2023–early-2024 weakness primarily to macroeconomic uncertainty rather than a structural loss of demand [7]. Operating margin, however, has compressed — from around 14% in 2021 to about 9.5% in 2025 — as the company absorbed relocation, hiring in higher-cost geographies, and reinvestment [8].

Source: FY2025 Annual Report (Form 10-K), Consolidated Statements of Income; earlier years from prior 10-Ks, as reported [8].

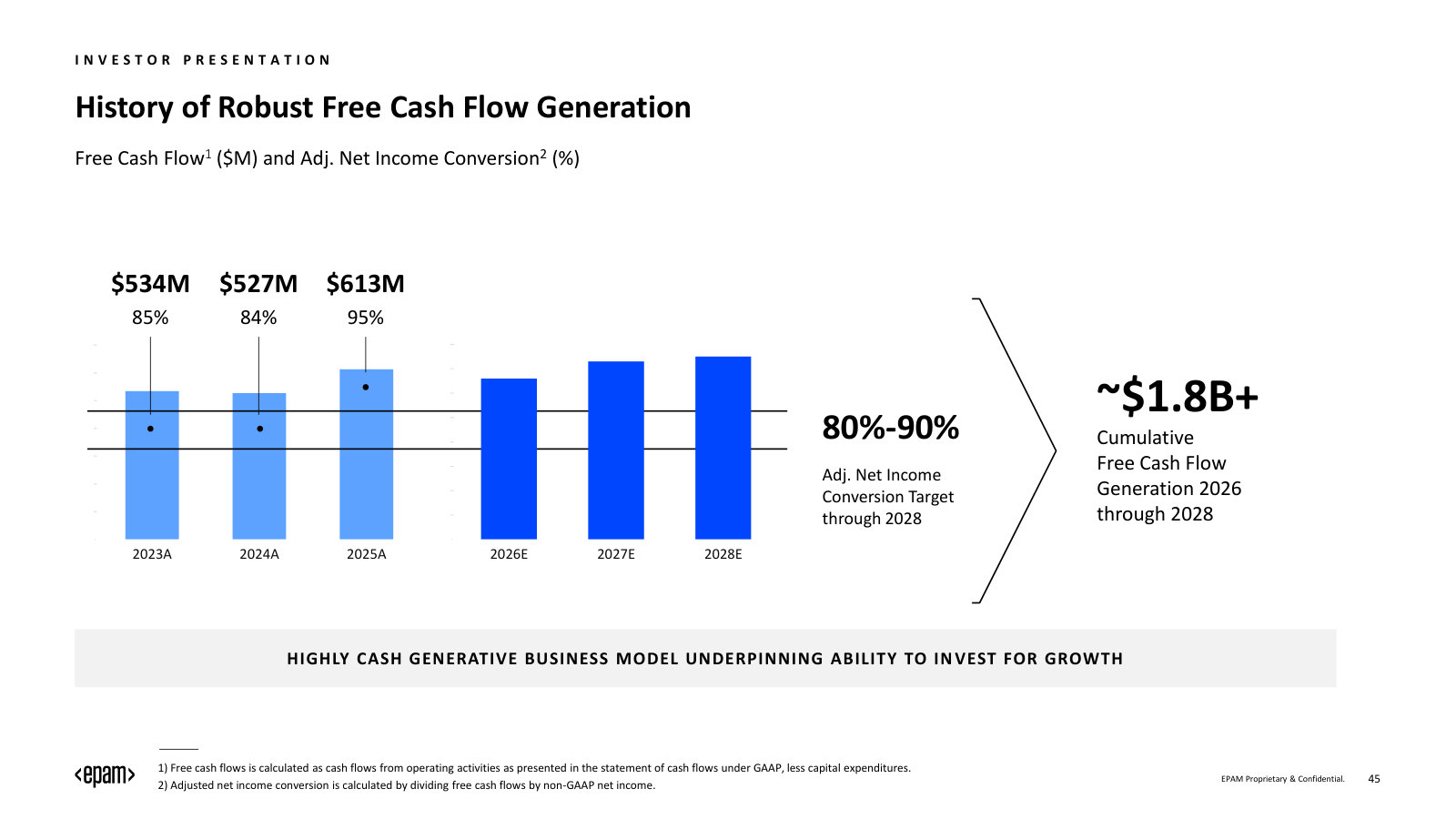

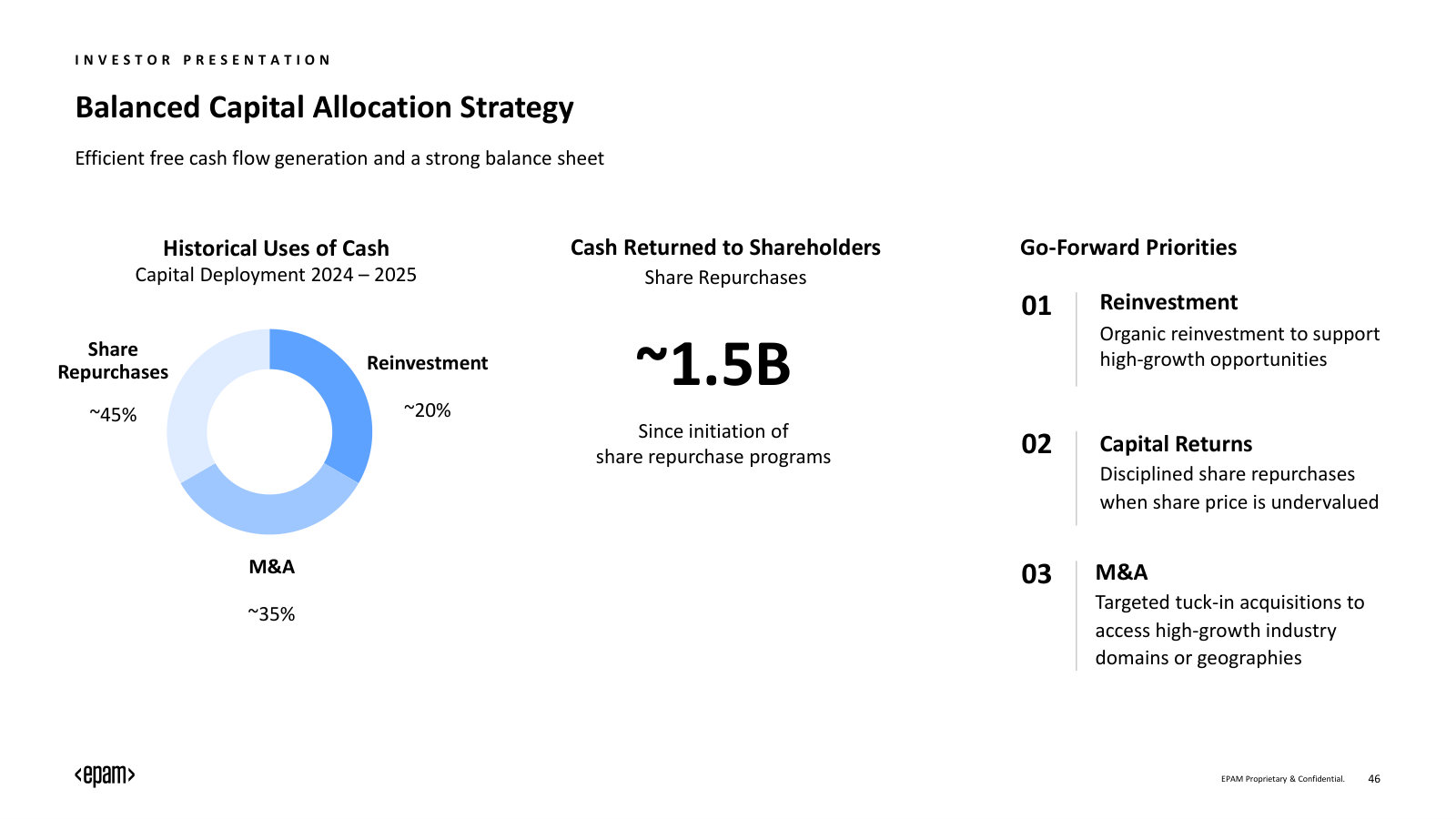

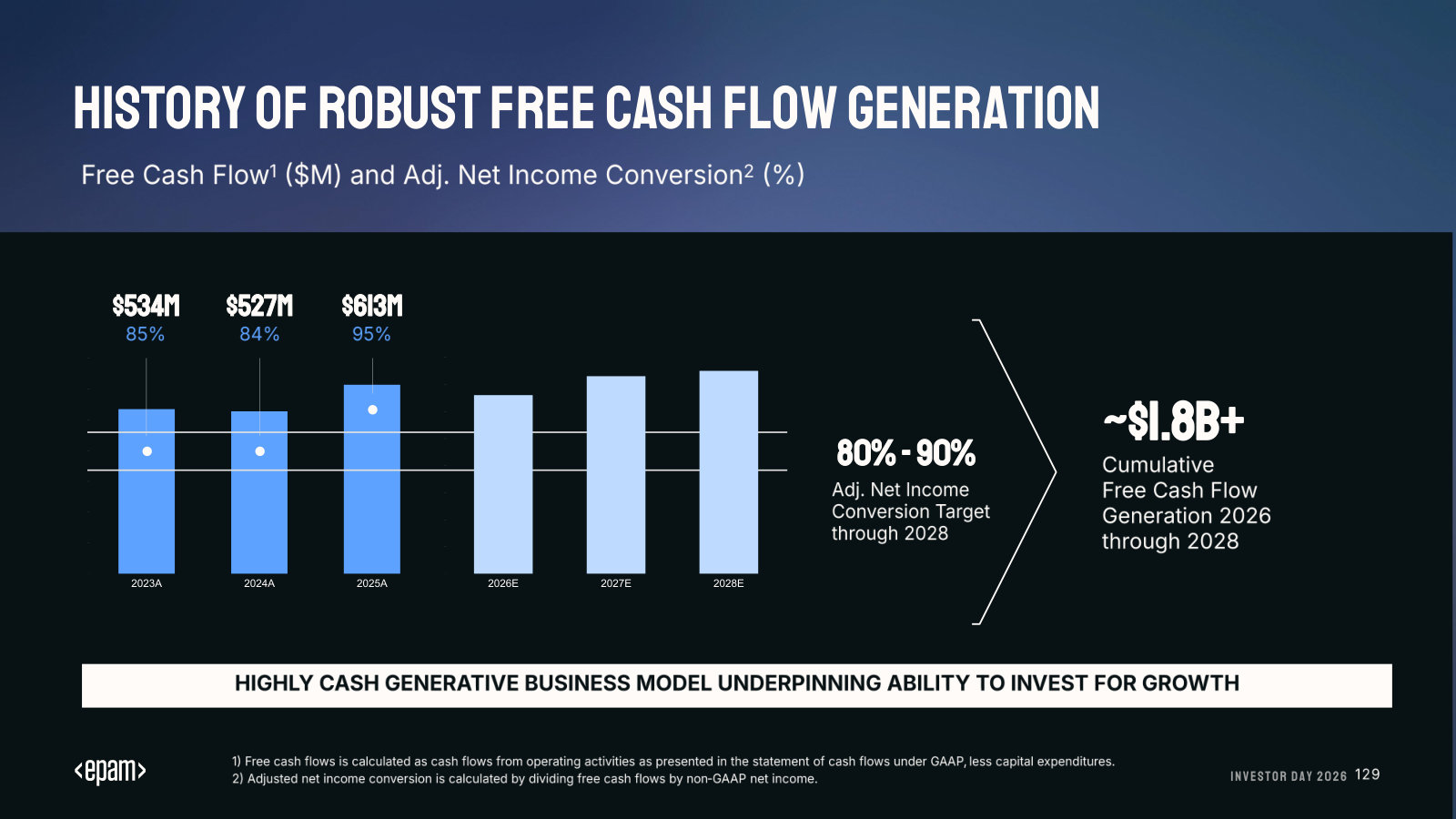

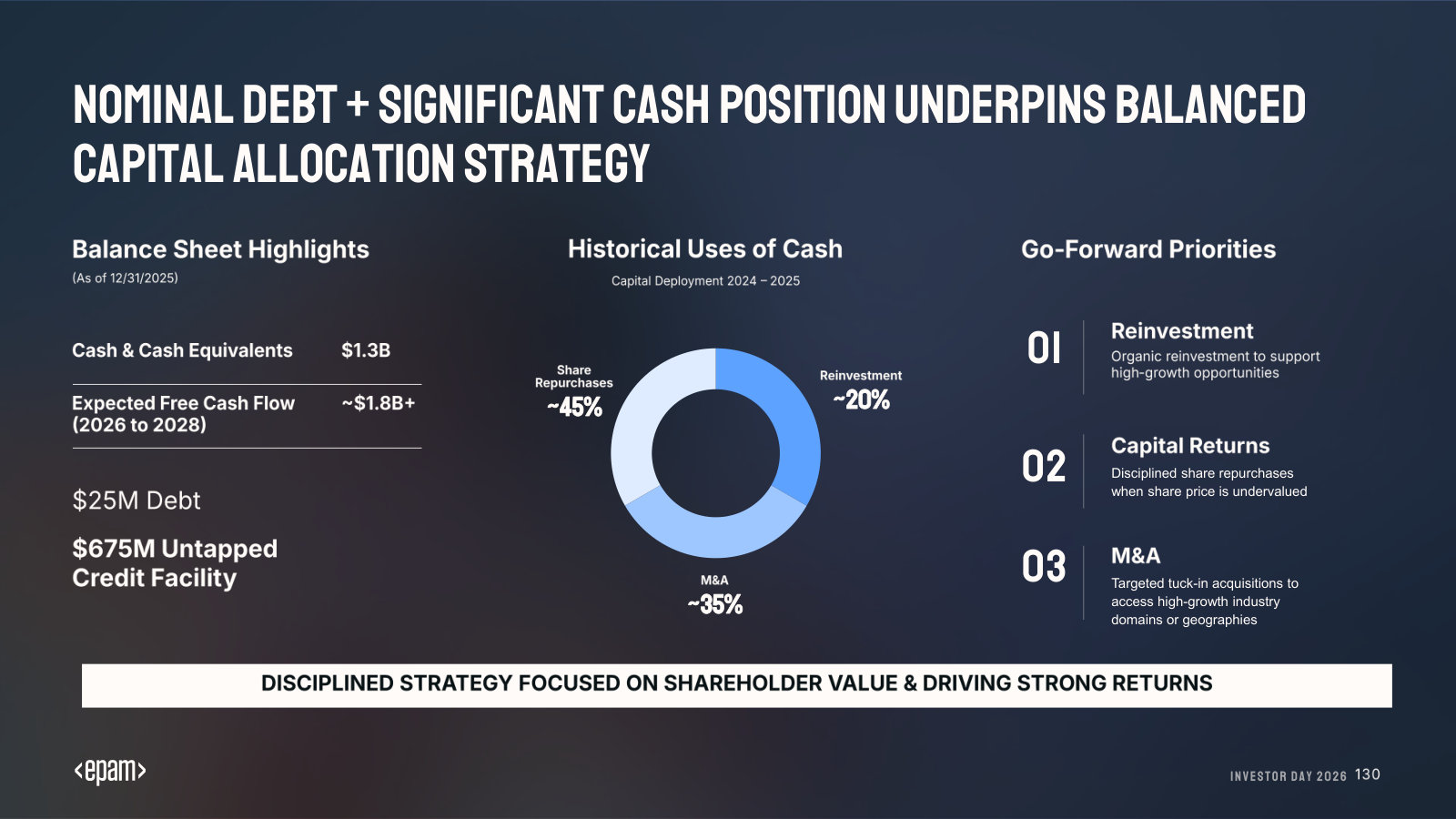

Net income of $378 million in 2025 is below the $482 million EPAM earned in 2021 on 45% less revenue — a real deterioration in profitability, and the honest counter-point to any "nothing changed" reading. What did not deteriorate is cash generation. Operating cash flow reached $655 million in 2025 and free cash flow was about $613 million, both records, because this is an asset-light business with minimal capital spending [9]. The balance sheet carries $1.30 billion of cash against about $25 million of debt [10]. For a reader whose first fear is bankruptcy, EPAM is close to the opposite case: net cash, no meaningful borrowings, and positive free cash flow every year through the downturn.

Source: FY2025 Annual Report (Form 10-K), Consolidated Statements of Cash Flows [9].

What the price implies

At $86.38, EPAM's equity is worth about $4.9 billion. Strip out the $1.27 billion of net cash — 26% of the market value — and the operating business is priced at roughly $3.6 billion, against $613 million of trailing free cash flow: an enterprise value near 6x that cash flow. On reported (GAAP) earnings the trailing multiple is about 13x; on the consensus non-GAAP earnings analysts actually model, the forward multiple is roughly 7x.

Share Price

Market Cap ($M)

Net Cash ($M)

From 2021 Peak

EV / Free Cash Flow

Trailing P/E (GAAP)

Source: valuation derived from the July 13, 2026 close and FY2025 reported financials [8]; net cash per the FY2025 balance sheet [10]; price per NYSE history.

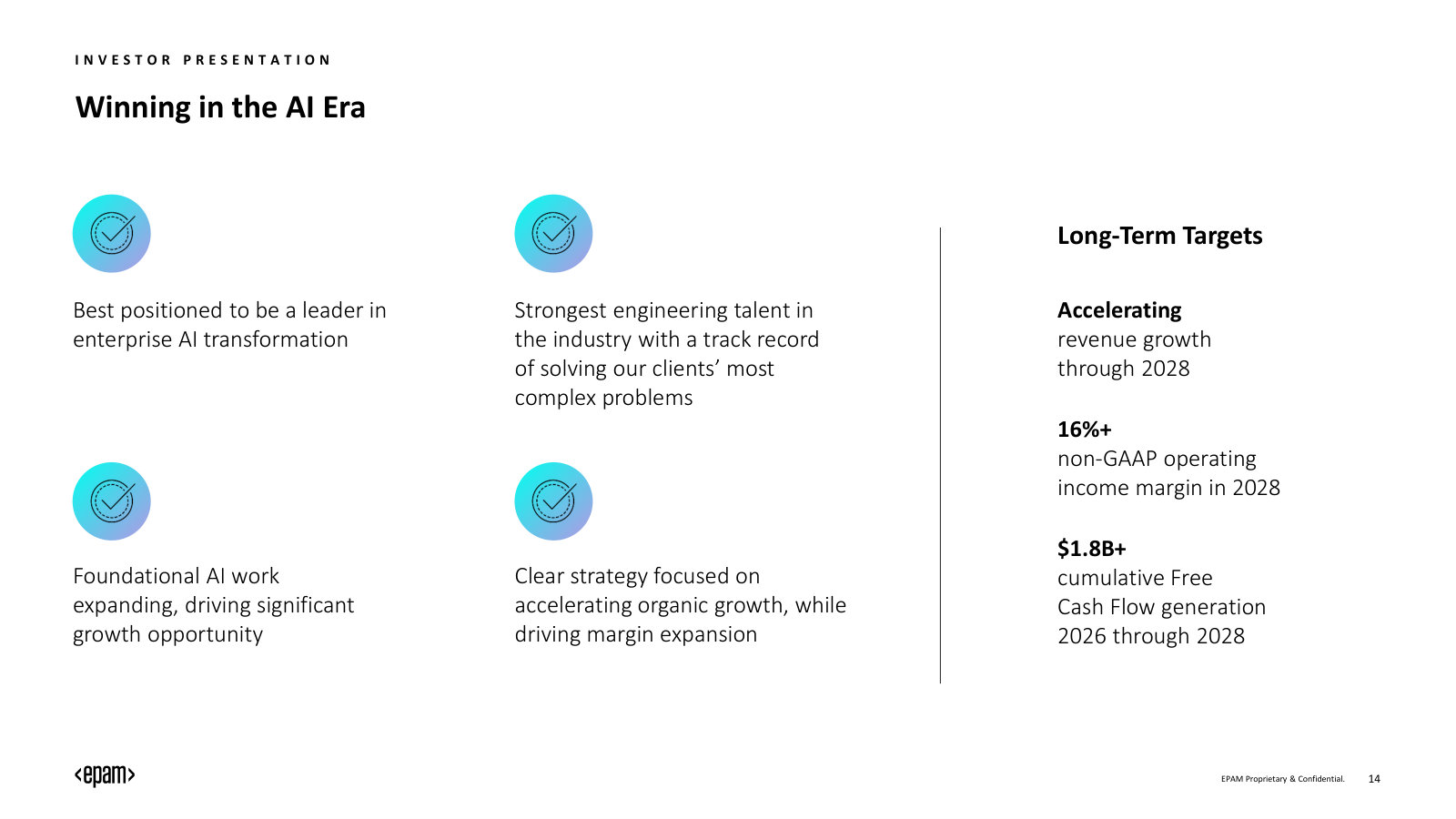

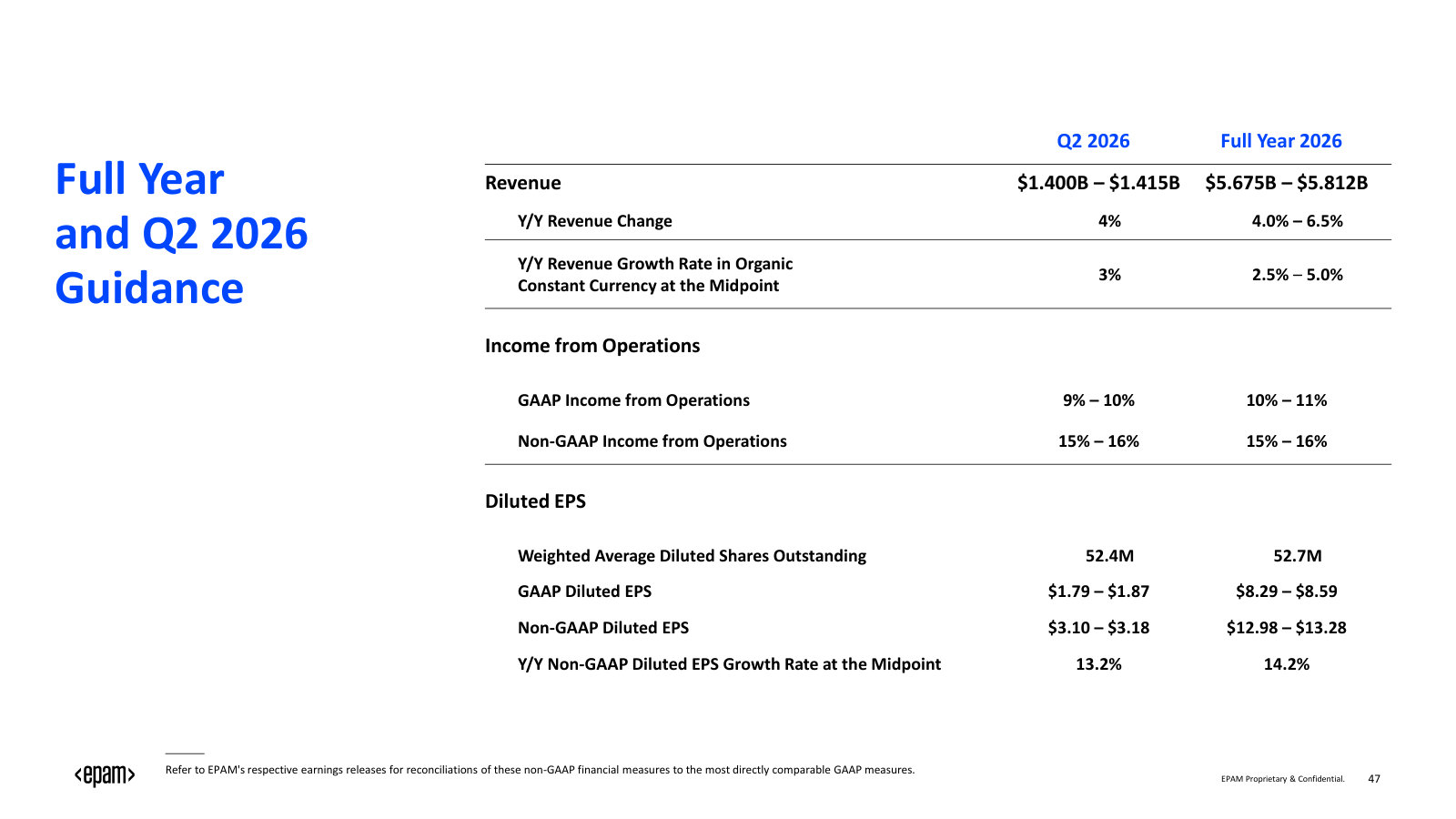

The sell-side is not modeling collapse. Consensus expects revenue to keep growing modestly — around 5% in 2026 and 6% in 2027 — and non-GAAP earnings to rise to roughly $13 and $14 a share. The mean analyst price target is about $139, some 60% above the current quote; notably, the lowest target in the range, $85, sits essentially at today's price. That configuration — a stock trading at the floor of the analyst range, on a mid-single-digit forward multiple, while estimates still show growth — is the "pessimism already priced in" setup, and it is what makes EPAM worth a careful look rather than a glance.

Source: FY2025 actual per the 10-K [8]; FY2026–FY2027 figures are consensus estimates, as reported.

The question this report answers

EPAM is a fallen star with a clean balance sheet, a still-loyal client base, a founder who built it over thirty years, and a valuation that already assumes the story is broken. The central question this report exists to answer is this: does EPAM's roughly 87% fall from its 2021 peak mark a durable, cash-generative, founder-anchored engineering franchise that the market has overshot to the downside — or the early, rational repricing of a labor-based software-services model that AI and geographic dislocation are structurally impairing? Everything that follows tests one side of that question against the other — the economics of the delivery model, what AI does to billable hours, how management is spending the cash, and how much margin of safety the price genuinely provides.